You open a dashboard, see a stablecoin vault flashing a high APR, and your first thought is usually the right one: what am I getting paid for, and what am I taking on to get it?

That question matters more in DeFi than the headline number. APR is useful, but it's only a signal. It tells you where to look, not where to park capital blindly. If you treat APR as the answer, you'll chase noisy incentives, miss fee drag, and confuse temporary emissions with durable yield.

The practical move is simpler. Read APR as the first layer of a strategy. Then separate sustainable income from marketing, compounding from simple return, and real risk from polished UI.

What Is APR and Why It Matters in DeFi

In traditional finance, APR means annual percentage rate. It's a standardized measure of the annual cost of borrowing that includes interest and certain lender fees, which is why it's more useful than a plain stated interest rate when comparing products like mortgages, auto loans, and credit cards, as explained in Capital One's overview of how APR includes interest plus certain loan fees.

In DeFi, people use the term differently in day-to-day conversation. Most of the time, when a protocol shows an APR on your deposit, it's presenting a simple annualized return without compounding. Same letters, different practical use. Instead of asking what it costs to borrow, you're asking what you might earn by supplying capital.

The DeFi translation

If a stablecoin pool shows an APR, read it as a rough annualized earning rate based on current conditions. That's the clean version.

The messy version is what experienced users already know:

APR is a snapshot: It often reflects current utilization, current incentives, and current trading activity.

APR is usually pre-friction: Gas, slippage, bridge costs, and withdrawal timing can change what lands in your wallet.

APR may mix yield sources: Lending interest, trading fees, and token incentives can all be bundled into one number.

Practical rule: APR is a sorting metric. It helps you rank opportunities fast, but it doesn't tell you whether the yield is durable.

That's why APR still matters. It gives you a common language for comparison. When you're scanning lending markets, vaults, or LP positions, APR is the first number that lets you compare unlike interfaces on roughly similar terms.

Why seasoned users still start with APR

Smart DeFi users don't ignore APR. They just don't stop there. A posted APR tells you where the protocol wants your attention. Your job is to ask what's underneath it.

If you're evaluating infrastructure or venue exposure as part of that process, it can help to review Uniswap for AI stacks and similar tooling pages that summarize how a protocol fits into broader onchain workflows. That kind of context matters when yield depends on actual usage, not just incentives.

A good mental model is this: APR is the label on the box. You still need to inspect the contents.

APR vs APY The Power of Compounding

APR and APY get mixed up constantly, and in DeFi that confusion gets expensive.

APR is the simple annualized rate. APY is the effective annual return after compounding. If the protocol auto-compounds rewards, or if you manually harvest and redeploy them, APY is the number that better reflects what your position can earn over time.

Why APR can understate the real result

A useful clue comes from outside DeFi. Khan Academy notes that APR is a standardized measure that can “understate a little bit” the cost in some cases because compounding changes what people pay over time. Their lesson on APR and the gap between standardized rates and actual paid amounts captures the same core idea DeFi users run into on the earning side.

In DeFi, flip that logic around. If rewards are reinvested, your actual effective return can be higher than the simple APR suggests. But only if compounding is real, affordable, and frequent enough to matter.

The snowball analogy works because it's accurate. A snowball gets bigger as it rolls because the fresh layer adds more surface area for the next layer. Reinvested yield does the same thing.

Here's the simple comparison.

Feature | APR (Annual Percentage Rate) | APY (Annual Percentage Yield) |

|---|---|---|

What it measures | Simple annualized rate | Effective annual return |

Compounding included | No | Yes |

Best use | Quick comparison of base rate | Estimating real growth if rewards are reinvested |

Common in DeFi | Displayed on lending markets, LP dashboards, vaults | Displayed by auto-compounding vaults or calculators |

Main risk of misuse | Overestimating what you'll earn if fees are high | Assuming compounding is frictionless |

What actually changes your result

Compounding only helps when the mechanics support it.

Reward frequency matters. If rewards accrue continuously but you claim rarely, your realized return may sit closer to APR than APY.

Transaction costs matter. Onchain actions can eat the benefit of frequent compounding.

Reward asset quality matters. Reinvesting a weak incentive token into the same position can raise displayed APY while weakening your actual portfolio quality.

A calculator helps if you want to model those trade-offs before touching a vault. This guide on how to calculate APY is useful for turning an advertised APR into a more realistic earning estimate.

Later in the decision process, I care less about the theoretical APY and more about whether compounding is net positive after all friction.

For a quick visual explainer, this video does a solid job of separating the two concepts:

A high APY built on constant manual harvesting isn't passive. It's a part-time job with execution risk.

Reading Between the Lines DeFi APR Pitfalls

The APR you see on a DeFi screen is often accurate in a narrow technical sense. It still may not describe the return you end up with.

That gap is where most mistakes happen. Users anchor on the number, skip the mechanics, and deposit into a position whose yield profile changes the moment capital flows in or incentives rotate out.

Variable rates are the norm

Outside crypto, APR isn't always stable either. Citizens Bank notes that credit cards often have variable APRs tied to market conditions and that promotional APRs can rise after the intro period. That matters because borrowing costs remain high. The average APR charged for credit card accounts that incurred interest was 21.52% as of February 2026, according to NerdWallet citing the Federal Reserve in Citizens Bank's explainer on variable APRs and promotional rate changes.

DeFi behaves the same way in principle, just faster. Supply changes. Borrow demand moves. Incentive programs start and stop. Trading volume dries up. A vault that looked attractive this morning can look ordinary by tonight.

The common traps behind headline APR

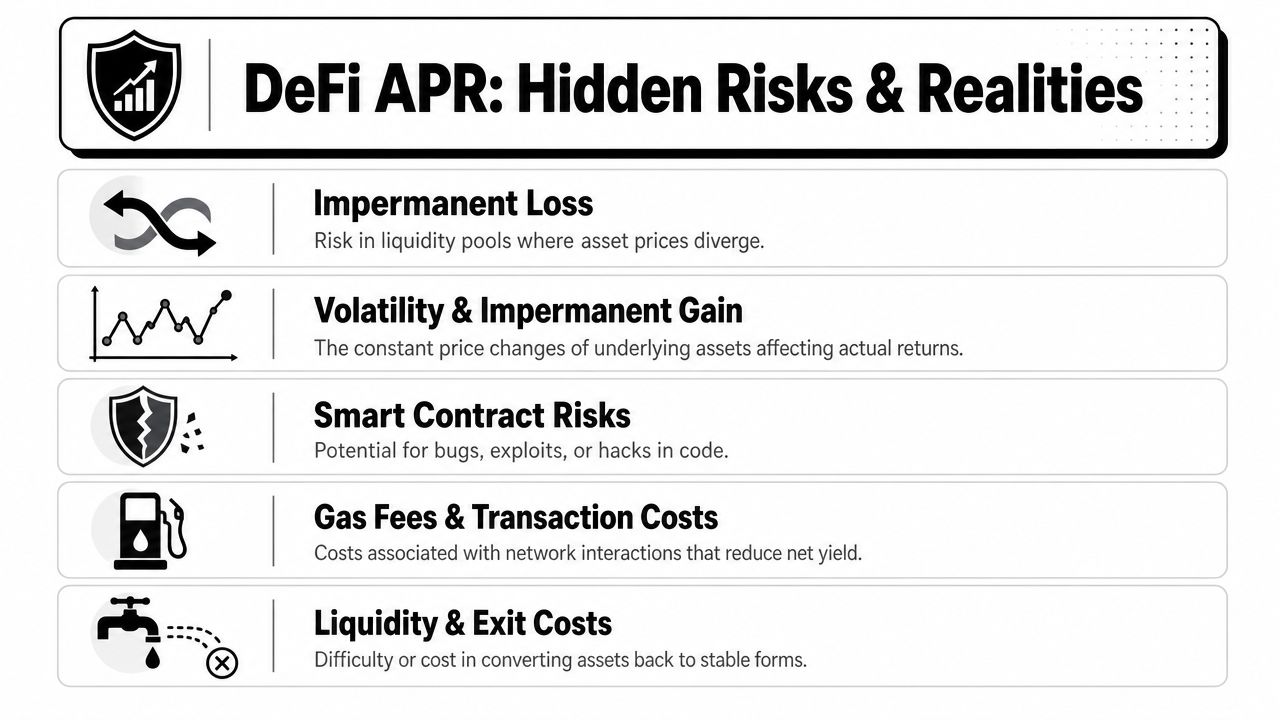

Some APRs come from healthy activity. Others come from conditions you shouldn't want to own.

Token emissions can distort the picture: If most of the yield comes from a reward token, you need conviction in that token, not just the percentage.

Fees reduce net return: Gas, bridge costs, performance fees, and withdrawal friction can shrink what looked like a clean spread.

Smart contract risk is real: A stablecoin strategy with elegant math still depends on code, admin controls, oracle design, and emergency procedures.

Liquidity matters on the way out: If a protocol is easy to enter but awkward to exit, your realized yield can be much worse than the dashboard suggested.

Risk filter: When APR spikes suddenly, assume there's a reason. Sometimes it's healthy demand. Sometimes it's mercenary capital farming an incentive before leaving.

Questions worth asking before you deposit

I've found that a short skepticism checklist beats a deep spreadsheet at the start.

Check | What to look for |

|---|---|

Yield source | Organic borrowing demand, trading fees, or token subsidies |

Rate stability | Whether the displayed APR is drifting, spiking, or decaying |

Exit path | How easily you can unwind back to stablecoins |

Operational overhead | Whether the position needs active claims, rebalancing, or monitoring |

The big takeaway is simple. High APR often means high sensitivity. Sensitivity to flows, incentives, volatility, or platform assumptions. If you don't know which one is driving the number, you don't know what you own.

How to Evaluate Stablecoin Yield Opportunities

A stablecoin opportunity gets easier to judge once you stop asking, “Is this APR good?” and start asking, “What machinery produces this yield?”

That one shift cuts out a lot of noise.

A usable checklist

When I screen a new vault, lending market, or pool, I run through four checks.

Find the source of yield.

Lending revenue is different from swap fees. Both are different from pure token emissions. If the protocol can't explain the source clearly, skip it.Separate base APR from bonus APR.

A position backed by actual usage is usually more durable than one propped up by incentives. If rewards stopped tomorrow, would the strategy still make sense?Inspect the operating burden.

Some opportunities only look attractive because they assume active management. If you need to claim, swap, bridge, and redeploy constantly, treat the posted number as gross, not practical.Model your exit before entry.

Stablecoin yield isn't just about earning. It's about getting back to stablecoins cleanly when conditions change.

What works better in practice

The strongest setups usually share a few traits:

Simple mechanics: Straightforward lending or conservative vault logic is easier to monitor.

Clear reward composition: You can tell what comes from usage and what comes from incentives.

Low maintenance: Fewer moving parts means fewer chances to leak return.

Reliable unwind path: You can reduce or close exposure without drama.

For broader context on where rates come from across the market, this overview of stablecoin interest rates is a practical reference.

What usually doesn't work

Chasing the top number on an aggregator tends to fail for the same reasons every time.

You arrive late: The advertised APR compresses after deposits flood in.

You underestimate friction: Fees and rebalancing eat the edge.

You own weak incentives: The quoted return depends on selling a reward asset under pressure.

If you can't explain a stablecoin yield strategy in plain English, you probably shouldn't scale it.

The goal isn't to find the flashiest APR. It's to find a return stream you can understand, monitor, and exit without surprises.

Automating Your Strategy with Yield Seeker

Manual yield hunting works if you enjoy watching dashboards, checking incentives, and re-evaluating venues whenever rates move. Many lack the time for such activities, especially if they're managing idle stablecoins alongside actual work.

That's where automation starts to make sense. Not because research stops mattering, but because the repetitive parts can be systematized.

Where automation helps

A tool can't remove market risk, contract risk, or strategy risk. It can reduce the burden of tracking fragmented opportunities and constantly re-checking whether an APR still deserves your capital.

That's the practical case for Yield Seeker. It's an AI-powered platform that lets users deposit stablecoins on Base and have an AI agent monitor and allocate capital across DeFi protocols in real time, with funds remaining accessible and no lockups or withdrawal fees. For users who want the mechanics behind that workflow, the write-up on automated APY discovery shows how this type of system approaches yield monitoring.

How to read APR inside an automated setup

Automation doesn't make APR magic. You still want to interpret the dashboard correctly.

Displayed APR is still a signal: It shows what the strategy is earning under current market conditions.

Movement matters more than the headline: A stable rate can be more useful than a flashy one that collapses after inflows.

Net behavior is what counts: If the system can reduce idle cash, redeploy efficiently, and avoid unnecessary churn, it can make the strategy easier to live with.

There's a practical difference between seeing ten opportunities and managing one coherent flow of capital. The first feels informed. The second is usually what busy users need.

Good automation doesn't promise perfect yield. It reduces missed opportunities, repetitive checking, and sloppy execution.

For experienced DeFi users, the appeal is less about convenience than consistency. For newer users, it's often the opposite. They want guided access without learning every dashboard from scratch. Both groups are solving the same problem: turning APR from a noisy feed into a usable earning process.

From APR Signal to Smarter Stablecoin Earnings

APR matters because it gives you a fast way to scan the market. That's why it's on every lending page, vault card, and pool interface. But the useful part of APR isn't the number alone. It's what the number prompts you to investigate.

In DeFi, that means asking a few sharp questions. Is the yield organic or subsidized? Is the rate stable or jumpy? Can you compound efficiently? Can you exit without giving back weeks of return through friction or poor timing?

The right way to use APR

The strongest stablecoin operators I know don't chase APR mechanically. They use it as a filter, then they pressure-test the source of yield.

That approach usually leads to better decisions:

Prefer understandable yield over flashy yield

Treat variable APR as normal, not exceptional

Estimate net return, not dashboard return

Value low-maintenance strategies if your time is limited

What smarter earning actually looks like

Smarter earning isn't finding the highest number on the screen. It's building a repeatable process for selecting yields you can live with.

Sometimes that means taking a lower posted rate because the source is cleaner. Sometimes it means skipping a reward-heavy vault because the incentive won't hold. Sometimes it means automating part of the workflow so your capital stays productive without demanding constant attention.

APR is the signal. Judgment is the edge.

If you read APR that way, stablecoin yield gets simpler. Not easy, because DeFi still has real risk. But simpler, because you stop treating a single metric as the whole story and start using it as intended: an entry point to a better decision.

If you want a lower-friction way to put that process into practice, Yield Seeker gives you an AI-assisted way to monitor and allocate stablecoin capital across DeFi opportunities without manually checking every protocol yourself.