You're probably in a familiar spot. You hold USDC or another stablecoin, you see DeFi yields that look materially better than a bank account, and your first question isn't “how do I get the highest APY?” It's “what's the catch?”

That question usually leads to a pile of protocol docs, dashboards, and acronyms. LTV. Health factor. Liquidation threshold. Utilization. Reserve factor. Most of it is useful, but the core idea is simpler than the interfaces make it look.

If you understand collateral, you understand the basic safety model behind onchain lending. And if you care about yield, treasury management, or using stablecoins without getting surprised by hidden risk, collateral isn't background knowledge. It's the operating system.

Why Collateral Is the Bedrock of DeFi

Collateral is often introduced when one considers a practical question: why would anyone lend onchain to a wallet they don't know?

The answer is that they usually don't lend on trust. They lend against assets already locked in a smart contract. If a borrower wants to access liquidity, the borrower posts something of value first. That posted asset is the lender's protection and the protocol's enforcement mechanism.

This isn't a crypto novelty. In traditional credit markets, collateral sits at the center of how lending works. European Central Bank research finds that about 70% of credit amounts are collateralized, and pledged collateral is associated with 33% to 48% higher committed loan amounts in secured lending markets across countries, which shows how directly collateral shapes credit access and pricing (European Central Bank working paper on collateralized credit).

That matters because DeFi didn't invent the logic. It automated it.

Why this matters for your money

If you deposit stablecoins into a lending market, your yield usually depends on borrowers posting enough collateral to support the loan. If you borrow against crypto, your safety depends on how that collateral is valued, monitored, and liquidated when needed.

A simple way to explain it is:

Without collateral: lending depends on identity, underwriting, legal contracts, and collections.

With collateral: lending depends on asset quality, pricing feeds, liquidation rules, and smart contract execution.

In DeFi: those rules are public, mechanical, and fast.

Practical rule: Before chasing yield, identify what collateral is backing the activity that produces it.

For newer users, this is also where overcollateralized lending in DeFi starts to make sense. The extra cushion isn't there to make protocols look conservative. It's there because crypto assets can move quickly, and the protocol needs room to stay solvent while prices change and liquidators act.

Understanding Crypto Collateral

Collateral in crypto works like collateral anywhere else. You lock up an asset so you can borrow against it. If the loan becomes unsafe and you don't fix it, the system can sell some or all of that asset to repay what you borrowed.

The closest everyday analogy is a mortgage, but with one important difference. In DeFi, the system usually wants a larger safety cushion because collateral can trade around the clock and can reprice fast.

Why overcollateralization exists

If you pledge a volatile crypto asset, the protocol has to assume the value may drop before anyone can react. That's why you often need to post more value than you borrow.

Think of it less as a penalty and more as a buffer against three things:

Price volatility: ETH, WBTC, and other major assets can move sharply.

Execution delay: even automated systems need time for oracles to update and liquidators to transact.

Market stress: liquidity gets thinner exactly when everyone wants out.

That's why a protocol may treat two assets with the same dollar value very differently. A stablecoin and a volatile token aren't equally useful collateral just because both are worth the same amount at deposit time.

Volatile collateral versus stable collateral

Using volatile assets like ETH or WBTC as collateral gives you one kind of flexibility. You keep market exposure while borrowing stablecoins for spending, trading, or deploying elsewhere. The trade-off is liquidation risk. If the collateral falls, your loan gets riskier even if you haven't touched the borrowed funds.

Using stablecoins as collateral changes the profile. Price swings are usually smaller, so the loan is easier to manage. But stablecoin collateral has a different limitation. Since the asset itself is already cash-like, borrowing power may be less strategically interesting than with a volatile asset you want to keep.

Here's the practical split:

Collateral type | What it's good for | What usually goes wrong |

|---|---|---|

Volatile assets | Borrowing without selling long-term holdings | Borrowers get liquidated after fast market moves |

Stablecoins | Lower-volatility borrowing base, simpler treasury use | Users underestimate protocol, issuer, or liquidity risk |

Good collateral isn't just valuable. It has to remain usable when markets are messy.

That distinction becomes important later when you move from basic lending to yield strategies. In simple borrowing, the question is “how much can I borrow?” In advanced treasury work, the better question is “how efficiently can this collateral support multiple actions without forcing me into fragile positions?”

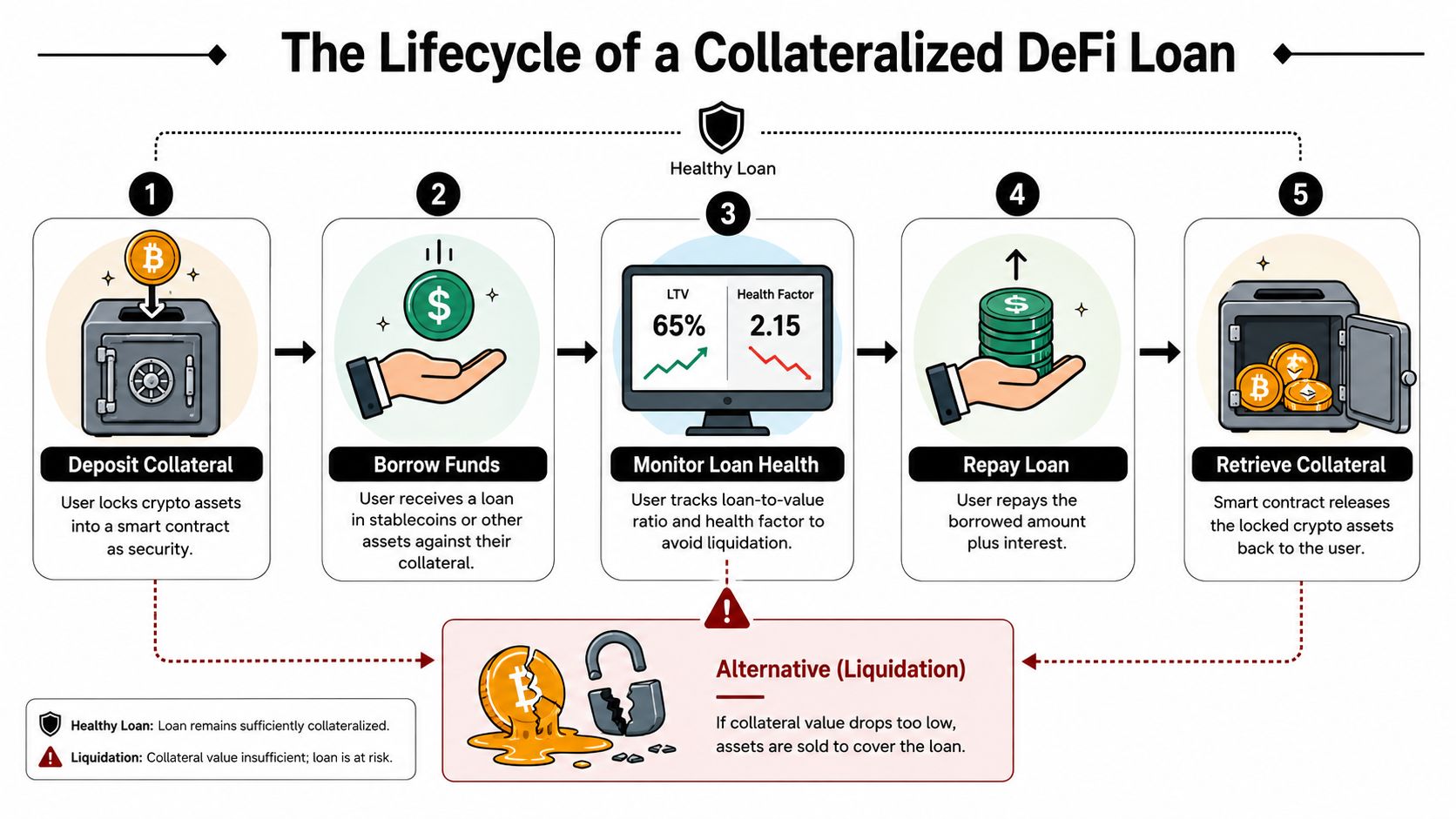

The Lifecycle of a Collateralized DeFi Loan

A collateralized loan onchain looks simple on the front end. Deposit asset. Borrow asset. But the lifecycle matters because the risk doesn't stop after the first click.

Start with a common case. A user deposits ETH into a lending protocol because they want stablecoin liquidity without selling their ETH. The protocol locks the ETH in a smart contract and lets the user borrow USDC against it.

Deposit and borrow

At the start, the loan looks healthy. The collateral is worth more than the borrowed amount, so the position has room. This is the part many people focus on because it feels like the decision point.

It isn't. The actual job starts after the loan opens.

Borrowing creates a live position that changes as market prices, interest accrual, and protocol parameters move. If you want a more detailed walkthrough of the mechanics, this guide to DeFi borrowing is useful background before opening your first position.

A short visual helps make the sequence concrete:

Monitor and defend the position

Once the loan is live, the borrower has to monitor the gap between collateral value and debt. That's where many preventable mistakes happen.

The common failure mode isn't that the original idea was wrong. It's that the borrower assumed the position could be left unattended.

A workable operating routine looks like this:

Track the collateral price: if your pledged asset falls, your safety buffer shrinks.

Watch accrued debt: interest can push a borderline position into danger.

Know your action plan: add collateral, repay part of the loan, or reduce exposure before the protocol does it for you.

A DeFi loan is closer to a margin position than a bank loan. The protocol doesn't care about your intentions. It cares about collateral sufficiency.

Liquidation and closure

If the position becomes too risky, liquidators step in. These are market participants or bots that repay part of the borrower's debt and receive collateral in return according to protocol rules. That process protects the protocol and, indirectly, depositors who supplied the lent funds.

Liquidation feels punitive when it happens to you, but from a system perspective it's necessary. Without it, lenders would be exposed to undercollateralized losses and the protocol's solvency would break down.

The loan ends in one of two ways:

Healthy closure: the borrower repays principal plus interest, then withdraws collateral.

Forced closure path: the protocol liquidates enough collateral to restore safety or fully close the debt.

The key practical lesson is simple. Opening the loan is easy. Managing the collateral through changing conditions is the true skill.

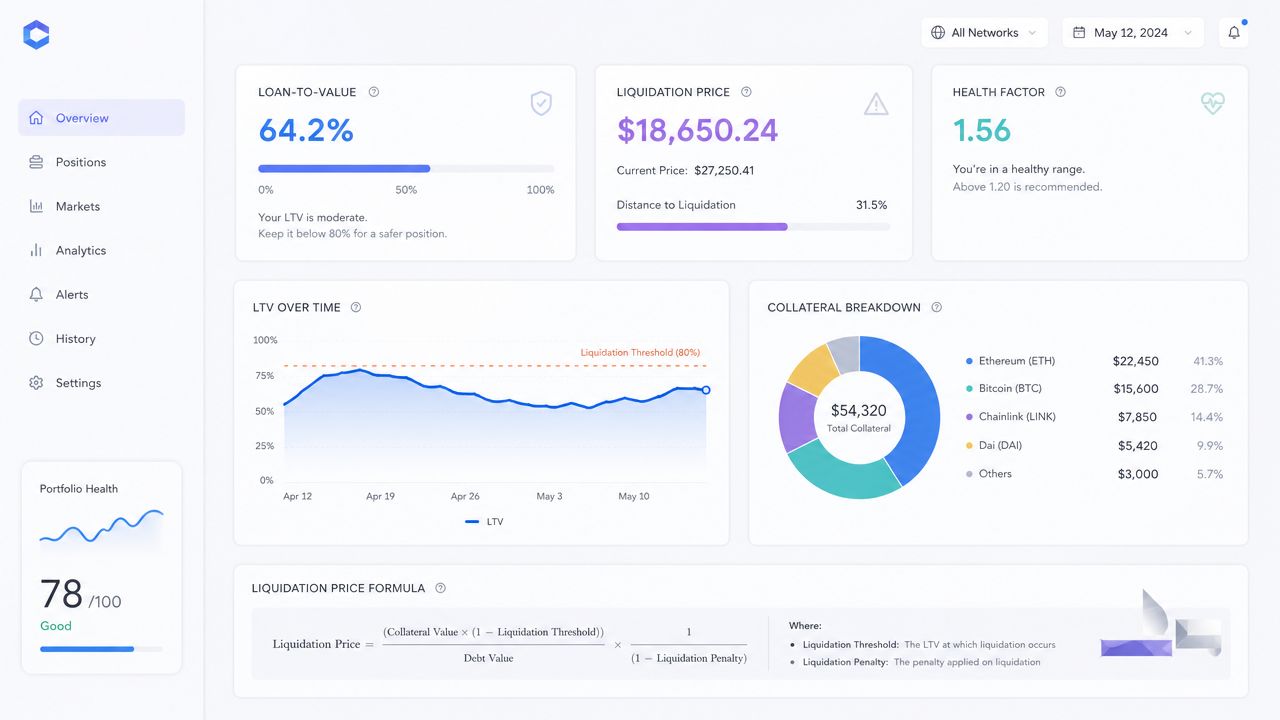

Key Risk Metrics You Must Understand

The fastest way to misuse collateral is to borrow based on the maximum number shown in a protocol UI. Safe borrowing starts with understanding the three metrics that control your room for error.

Loan-to-value

Loan-to-value, or LTV, is the ratio of borrowed value to collateral value.

Formula:

LTV = Loan value / Collateral value

If you deposit collateral worth $1,000 and borrow $500, your LTV is 50%.

LTV is the number that tells you how aggressive the position is. Higher LTV means more capital efficiency, but less room for price moves. Lower LTV means lower immediate borrowing power, but more resilience.

What works in practice is rarely borrowing at the maximum allowed. Experienced users usually treat the max as a ceiling, not a target.

Liquidation threshold and health factor

The liquidation threshold is the line where the protocol can begin liquidating your collateral. It is not the same as your current LTV. It's the danger boundary.

The health factor packages your distance from that boundary into a simpler score. Different protocols present it slightly differently, but the idea is consistent: the higher the health factor, the safer the position.

A practical interpretation:

Lower LTV than threshold: position is alive and relatively safer.

Near threshold: small price moves can trigger liquidation.

Past threshold: liquidators can act.

How the metrics interact

You don't manage these numbers separately. They move together.

Here's the useful mental model:

Metric | What it tells you | Why it matters |

|---|---|---|

LTV | How much you've borrowed against collateral | Measures aggressiveness |

Liquidation threshold | The protocol's risk boundary | Defines forced-sale risk |

Health factor | Distance from danger | Helps with ongoing monitoring |

Watch this, not that: Don't obsess over the borrow max. Watch how fast your health factor deteriorates when the collateral asset sells off.

There's also a broader reason to respect these mechanics. Collateral doesn't just affect one borrower's account. Research presented to the AEA finds collateral effects may account for as much as 37% of employment growth in certain economic cycles, which highlights how collateral can act as a macroeconomic transmission channel rather than a simple loan backstop (AEA conference paper on collateral and growth).

That same amplification logic matters in DeFi. Rising collateral values can make users feel safer and borrow more aggressively. Falling values can force deleveraging across many accounts at once. If you want to think clearly about yield, risk-adjusted APY matters more than headline APY, because collateral stress can erase attractive yield surprisingly fast.

Collateral in Action on Major DeFi Protocols

The theory is straightforward. The implementation varies a lot.

Aave, Compound, and MakerDAO all use collateralized lending logic, but they don't express risk in identical ways. Asset selection, oracle design, governance decisions, liquidation mechanics, and parameter updates all change the borrowing experience.

What to compare first

When evaluating a protocol, focus on four practical questions:

Which assets qualify as collateral

How much borrowing power each asset gets

Where liquidation begins

How easily you can monitor and unwind the position

The protocol brand matters less than the parameter discipline around the specific asset you plan to use.

Example comparison framework

The table below is intentionally a framework, not a live parameter sheet. Protocol settings change, and using stale numbers is a good way to get liquidated.

Collateral Factor & LTV Comparison on Major Protocols (Example)

Asset | Protocol | Max LTV | Liquidation Threshold |

|---|---|---|---|

ETH | Aave | Varies by market and governance settings | Varies by market and governance settings |

WBTC | Aave | Varies by market and governance settings | Varies by market and governance settings |

USDC | Aave | Varies by market and governance settings | Varies by market and governance settings |

ETH | Compound | Varies by market and governance settings | Varies by market and governance settings |

WBTC | Compound | Varies by market and governance settings | Varies by market and governance settings |

USDC | Compound | Varies by market and governance settings | Varies by market and governance settings |

ETH-backed vaults | MakerDAO | Borrowing constraints depend on vault type | Liquidation parameters depend on vault type |

What tends to work and what doesn't

A few patterns hold up across protocols.

Using blue-chip collateral for simple borrowing: This is usually easier to reason about than using thinly traded assets.

Matching strategy complexity to monitoring capacity: If you can't watch it, don't run a fragile structure.

Reading asset-level rules, not just protocol summaries: One protocol can be conservative on one asset and aggressive on another.

What usually fails is assuming “major protocol” automatically means “safe position.” A strong protocol can still host a weak user setup if the collateral is volatile, the LTV is too high, or the borrower ignores governance changes and market conditions.

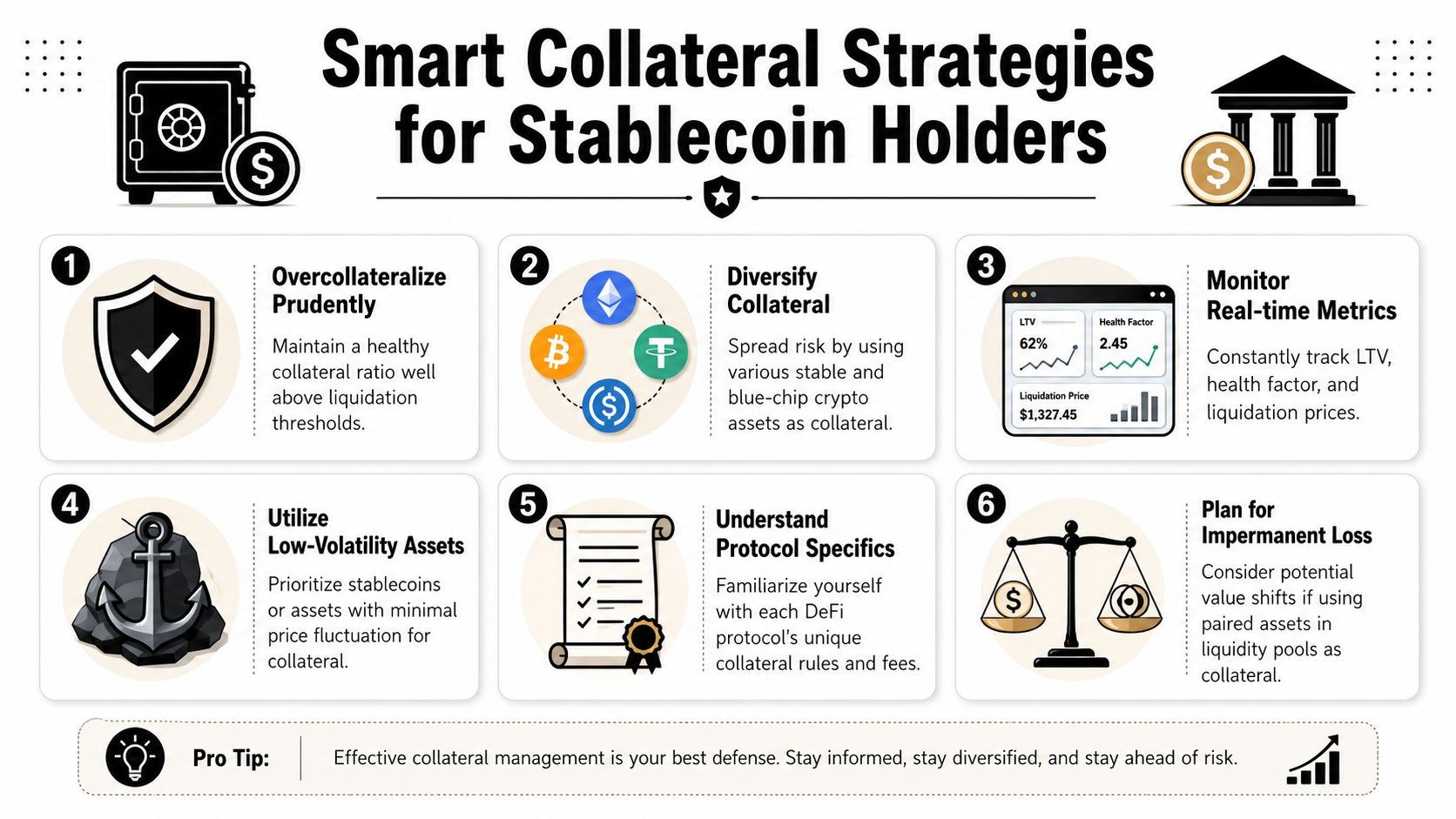

Smart Collateral Strategies for Stablecoin Holders

Stablecoin holders often think collateral is mainly a borrower concern. It isn't. Even if your primary goal is passive income, collateral quality shapes where your yield comes from and how resilient that yield is when conditions change.

The safest habit is to treat collateral management as portfolio construction, not as a one-time settings choice.

Practical habits that reduce bad outcomes

If you manage stablecoin capital, these habits matter more than squeezing out a slightly better rate on a single venue.

Keep a larger cushion than the protocol requires: The protocol minimum is a liquidation line, not a comfort zone.

Prefer simple structures you can explain in one sentence: If the strategy depends on several linked assumptions, it can fail in several ways.

Use collateral with deep liquidity when possible: In stressed markets, ease of exit matters as much as nominal value.

Separate treasury capital from speculative collateral: Don't make operating liquidity depend on a token you'd be unwilling to hold through a sharp drawdown.

Borrowing against volatile assets versus posting stablecoins

For many users, borrowing stablecoins against volatile assets is cleaner than trying to use stablecoins as the starting point for recursive borrowing strategies. You keep your crypto exposure and access liquidity, but you must actively manage downside risk.

For treasury-style users, stablecoin collateral can make sense when the goal is low-volatility positioning or operational liquidity. The mistake is assuming “stable” means “risk-free.” Stablecoins still carry issuer, liquidity, smart contract, and venue-specific risks.

Conservative collateral policy usually looks boring while markets are calm. That's exactly the point.

A checklist before deploying capital

Ask these questions before opening or funding any yield strategy:

What exact asset is the collateral?

How quickly can its market quality deteriorate?

Who liquidates unsafe positions, and how reliable is that process?

Can you add funds or reduce exposure fast if the position drifts?

Would you still like the strategy if the headline APY were lower?

If the answer to the last question is no, the setup may be yield-first and risk-blind. That usually ends badly.

Automating Collateral for Smarter Yield

Manual collateral management works when you run one position, watch markets closely, and don't mind moving funds yourself. It breaks down when capital is spread across venues, strategy rules differ by protocol, and the cost of staying attentive becomes its own operational burden.

That's where collateral efficiency matters more than raw collateral quantity.

A useful insight from outside crypto is that having collateral isn't the same thing as having effective collateral. Research on collateral channel success found that quality and usability characteristics can be more predictive than simple presence, which is a helpful analogy for market operations too. In practice, the important question is often not “do I have enough collateral?” but “is this collateral usable, liquid, and deployable where I need it?” (PubMed abstract on collateral quality and usability).

What collateral efficiency actually means

In DeFi operations, efficient collateral is collateral that can support borrowing or yield activity without creating unnecessary fragility.

That usually includes:

Liquidity: can the asset be sold or moved without ugly slippage?

Acceptance: is it eligible across the venues you use?

Stability under stress: does it remain useful when volatility rises?

Operational simplicity: can the position be monitored and adjusted without constant manual effort?

A portfolio can look well collateralized on paper and still perform poorly in reality if assets are fragmented, trapped in low-utility venues, or tied to strategies that require frequent intervention.

Why automation becomes practical, not optional

Busy professionals and treasury teams usually don't fail because they don't understand collateral. They fail because good collateral management is repetitive. You need to monitor positions, compare venue conditions, adjust allocations, and avoid drifting into bad risk-reward trades.

Automation helps when it does three things well:

Function | Why it matters |

|---|---|

Continuous monitoring | Reduces the chance that a healthy position quietly becomes a weak one |

Allocation logic | Helps move capital toward better risk-reward setups |

Rebalancing discipline | Prevents emotion and neglect from driving decisions |

The key is that automation should improve judgment, not hide risk. A strong system doesn't just chase the highest available yield. It evaluates whether the collateral behind that yield is secure enough to justify the return.

If you want to earn on stablecoins without manually checking fragmented DeFi markets every day, Yield Seeker is built for that job. It helps users deposit USDC, keep funds accessible, and let an AI-driven system monitor and allocate capital across DeFi protocols with a focus on competitive, risk-aware yield.