You do not get a warning shot with liquidation. A sharp move hits, you open your wallet, and the position you planned to fix after lunch has already been cut by the protocol.

That is the central risk in DeFi with debt. Borrow against ETH, run a looped yield trade, open margin, or post volatile collateral for stablecoin liquidity, and you are accepting a system that watches collateral value in real time and acts faster than you do. Conviction does not matter. Reaction time often does not matter either.

Liquidation matters outside crypto too. Traditional finance treats imminent liquidation as a different financial state because the rules change once survival is in doubt. DeFi strips that down to code and enforces it continuously. The result is harsher, more transparent, and less forgiving.

The practical point is simple. Liquidation is not a rare edge case. It is the operating constraint behind every amplified trading strategy. Anyone taking signals from social channels should treat that risk with the same seriousness they give entry timing. Tools that Analyze crypto trading Telegrams can help filter noise, but signal quality alone does not protect a position once collateral ratios start breaking.

Good risk management in DeFi means assuming you will be tested at the worst possible time, then setting alerts, buffers, and automation before that test arrives.

The Silent Risk That Can Erase Your Crypto

You post ETH as collateral before work, borrow against it, and leave the position alone because the buffer looks comfortable. By the time you check again, price has slipped, liquidators have stepped in, and part of your collateral is gone. That sequence is common in DeFi. It is also preventable more often than users admit.

Many users say they understand liquidation because they know the definition. That is not enough. In practice, liquidation is the mechanism that keeps a lending or margin system solvent by closing your risk before your losses become the protocol's problem.

That is why liquidation feels brutal. Your trade thesis can still make sense over the next week. Your collateral only needs to fail the protocol's test for a few minutes.

The danger gets worse when users treat borrowing as a side feature instead of the core risk. A position can look productive because it earns yield, funds another trade, or supports a stablecoin strategy. Underneath, it is still a race between collateral value, debt growth, and market speed. If you need a refresher on that setup, this guide to how DeFi lending works covers the borrowing structure that liquidation sits on top of.

Why liquidation feels unfair

Liquidation does not care whether the move is irrational, temporary, or driven by panic. Code checks the ratio. Bots execute. You absorb the loss, plus fees and any penalty the protocol applies.

Traditional finance also treats imminent liquidation as a different state because survival changes the rules. DeFi strips away committees, phone calls, and delay. What remains is a hard trigger and a market full of automated actors competing to hit it first.

Crowded positioning makes this worse. Traders copy the same ETH loop, the same carry trade, or the same “safe” stablecoin setup, then volatility hits and everyone reaches for the exit at once. If you trade off signals from chat groups or social channels, tools that Analyze crypto trading Telegrams can help separate useful flow from momentum chasing before a crowded trade turns into a liquidation wave.

Practical rule: If your plan depends on having time to react manually, the position is carrying more liquidation risk than it appears.

What actually protects you

Discipline protects you. Wide collateral buffers help. Clear exit levels help. Alerts matter, but alerts alone are not enough in fast markets or high gas conditions.

The durable approach is simple and not glamorous. Size smaller than your model says you can. Assume volatility will expand when liquidity gets worse. Check how close your position is to the liquidation line before you focus on APY. Then automate as much of the monitoring as possible, because liquidation is the one DeFi risk that punishes inattention with perfect consistency.

The users who last in capital-amplifying DeFi do not treat liquidation as a rare accident. They treat it as the main job. Modern monitoring and AI-driven risk tools make that job far more realistic by tracking thresholds, market stress, and position health continuously, instead of waiting for you to notice trouble after the protocol already has.

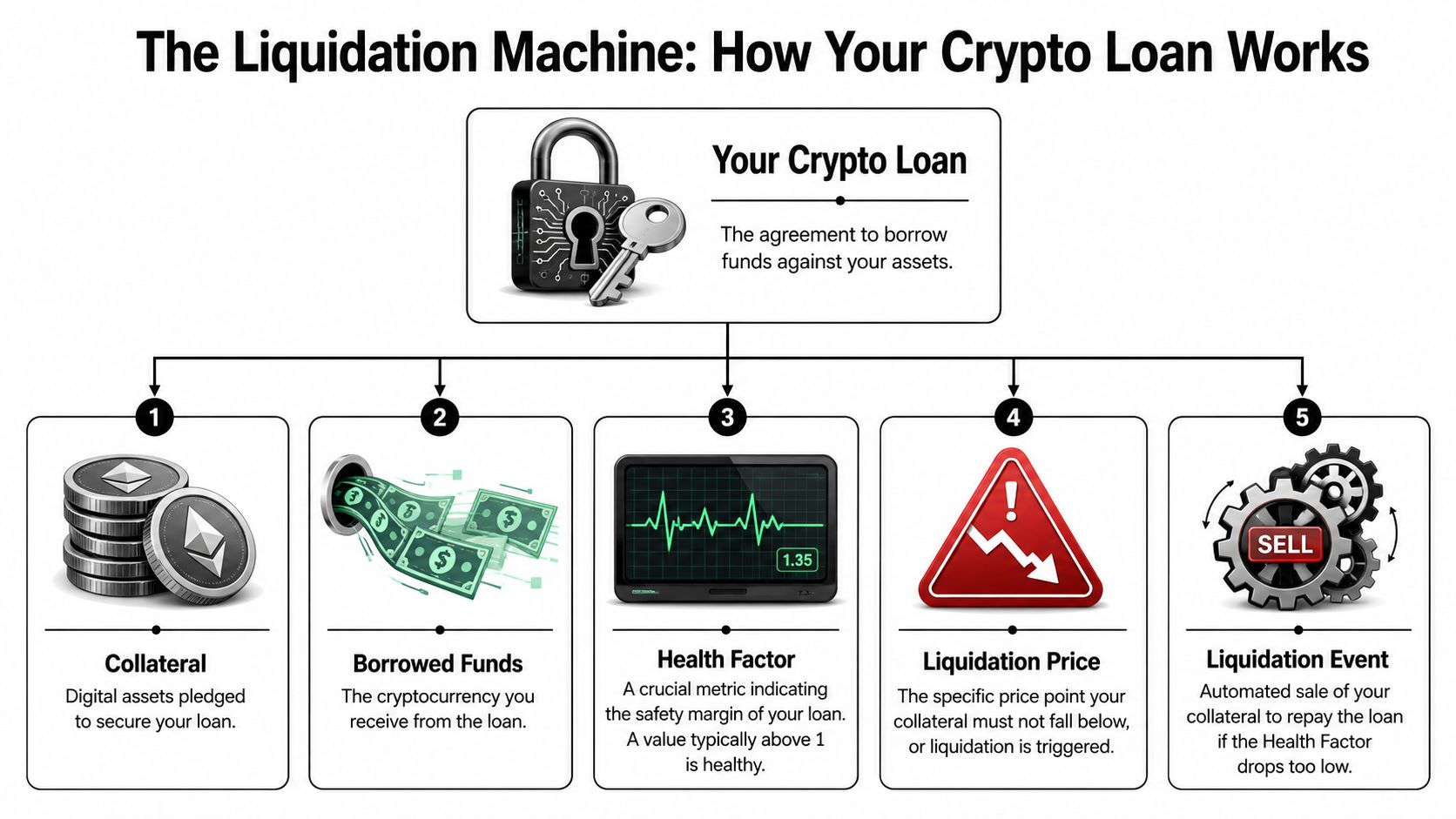

Understanding the Core Mechanics of Liquidation

The cleanest analogy is a pawn shop loan. You hand over an asset, receive cash, and the lender cares about one thing above all else: whether the asset still covers the loan with enough room for safety.

DeFi works the same way. Your collateral is the asset you deposit. Your debt is what you borrow. The protocol continuously checks whether the collateral still supports the debt. If not, liquidation starts.

The key numbers that matter

Most users look at APY first. Experienced users look at risk metrics first.

Collateral value: The market value of what you deposited.

Debt value: What you owe the protocol.

Loan-to-Value or LTV: The ratio between borrowed funds and collateral value.

Liquidation threshold or equivalent: The line where the protocol no longer considers the position safe.

Health factor: A shorthand safety score used by some interfaces. Higher means more buffer.

A simple mental model helps. If your collateral drops while your debt stays the same, your LTV rises. If your LTV rises too far, your health factor falls. When the platform's trigger is hit, someone else closes risk for you.

Protocols don't liquidate on time held

Many beginners are often confused by this. Liquidation usually isn't about how long you borrowed. It's about collateral health right now.

According to Drift's liquidation documentation, some platforms liquidate when totalCollateral falls below maintenanceMarginRequirement. Morpho-style lending uses a different lens, where liquidation activates when a borrower's LTV exceeds the market's Liquidation LTV or LLTV. Same idea, different implementation.

Here's a useful outside primer on preventing margin calls for traders if you want the traditional market parallel. The language differs, but the discipline is the same.

For a broader foundation on lending mechanics, see DeFi lending explained.

A short walkthrough can help if you prefer visual learning.

How to read your dashboard like a risk manager

Use this quick table when you open any margined position:

Metric | What it tells you | What usually worsens it |

|---|---|---|

Collateral value | How much support your loan has | A drop in asset price |

Debt value | What you owe | Borrowing more, accrued interest |

LTV | How stretched the position is | Falling collateral or rising debt |

Health factor | Your remaining safety buffer | Any move that pushes LTV toward the trigger |

Liquidation price | The level you can't afford to hit | Thin collateral buffer |

Don't ask whether your position is profitable. Ask whether it can survive a move against you before you get a chance to act.

How Liquidation Works in Different DeFi Arenas

A position can look safe on one dashboard and still be one bad candle away from forced closure on another. The rules change by venue. If you use the same risk habits everywhere, the protocol eventually corrects you.

Lending protocols

In lending markets, liquidation is usually partial and rule-based. You post collateral, borrow against it, and the protocol watches the relationship between the two. Once the account breaches its limit, a liquidator repays some or all of the debt and receives collateral plus a liquidation bonus, based on that market's formula.

The user-facing lesson is simple. Liquidation does not mean "my collateral gets sold" in some generic sense. It means your collateral gets taken according to that protocol's exact math, oracle inputs, close factor, and incentive structure. Those details decide how much of the position survives and how expensive the mistake becomes.

I have seen users treat all lending markets as interchangeable because the interface looks familiar. That is expensive thinking. Some protocols allow a liquidator to clear a large share of the debt quickly. Others limit how much can be repaid in one pass. Some rely on conservative oracle design. Others react faster, which can protect the system while giving borrowers less time to recover.

Margin and perpetual futures

Perpetuals are harsher because the collateral and the trade are tied together. In a lending position, collateral can drift down while the debt side changes more slowly. In a perp, unrealized losses hit account equity in real time. Your buffer can disappear fast.

Once equity falls below maintenance margin, the venue starts closing the position. On some platforms that means full liquidation. On others, the engine may reduce size first, then continue cutting if the move keeps going. The practical result is the same. A trader who treats a perpetual contract with magnified market exposure like a spot position often hands control to the liquidation engine.

Funding adds another layer. So does mark price design. So does slippage when markets get thin. The trade can be directionally right over a week and still get liquidated in an hour.

Recursive yield and stablecoin loops

Recursive strategies create a different kind of danger. You deposit an asset, borrow against it, deposit again, and repeat to increase yield or farm incentives. The position can look conservative because the collateral may be a stablecoin pair or a familiar blue-chip asset. The risk is still the amplified exposure. It is just stacked inside a loop.

That loop makes small changes matter more. Borrow costs rise. A stablecoin trades below peg. Collateral quality weakens. The health buffer across the whole structure shrinks faster than many users expect. By the time they check the dashboard, the position is already being unwound.

This catches careful users too, because the strategy feels passive after setup. It is not passive. It is an amplified carry strategy with liquidation risk attached.

Arena | Main trigger | User mistake that hurts most | What to monitor |

|---|---|---|---|

Lending | Collateral support falls below required level | Borrowing too close to the limit | LTV, health factor, oracle behavior |

Perpetuals | Margin falls below maintenance requirements | Treating a short-term trade like a long-term hold | Margin ratio, liquidation price, funding and volatility |

Recursive yield | Combined leverage across repeated borrow-deposit loops | Assuming stablecoins remove liquidation risk | Net exposure, depeg risk, borrow costs |

The common thread is discipline. Liquidation is the enforcement mechanism behind every design for magnified exposure in DeFi. Users who want to keep capital need venue-specific rules, clear buffers, and monitoring that does not depend on remembering to check manually. That is why automated risk tooling matters now. Markets move faster than human attention.

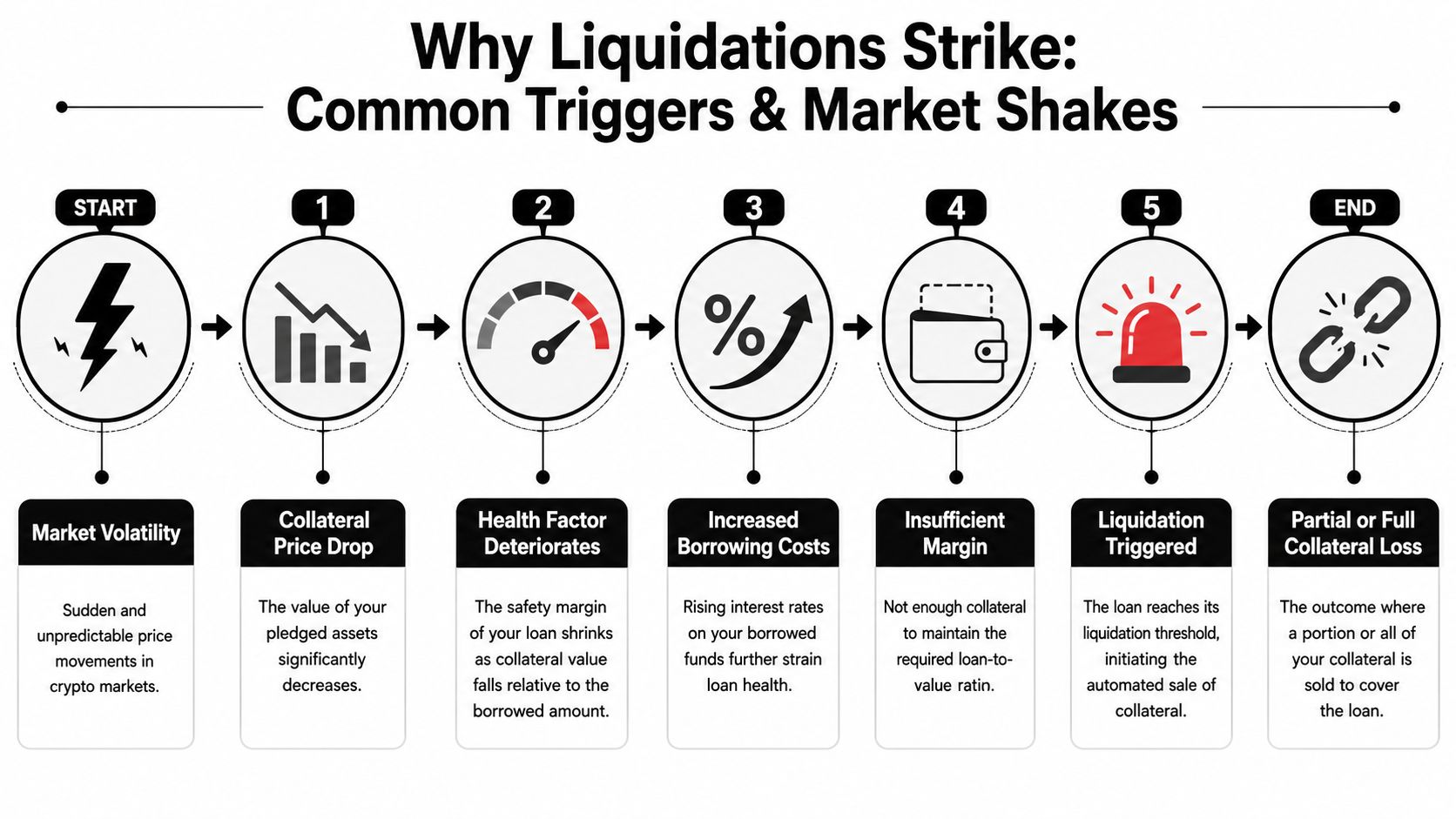

Common Triggers and Cautionary Tales

You go to sleep with a healthy buffer. You wake up to a smaller balance, a liquidation fee, and a transaction history that reads like a forced sale. That sequence is common in DeFi because liquidation risk builds imperceptibly, then gets enforced all at once.

A position usually breaks from several pressures hitting at the same time. Collateral drops. Debt grows. A price feed updates against you. Market depth gets worse right when you need to exit. The protocol does not care which part caused the damage. It only checks whether your position still meets the rules.

The triggers that hit most often

The repeat offenders are familiar.

Sharp collateral moves: A fast drawdown can erase a safety buffer before a user has time to top up or repay.

Debt growth: Interest accrual and variable borrow rates keep pushing the liability side higher, even if the collateral price does nothing.

Oracle timing and quality: Liquidation decisions depend on the protocol's chosen price source, update logic, and protections during volatile trading.

Thin exit liquidity: In stressed conditions, selling collateral or unwinding manually gets more expensive and less reliable.

Inattention: Users treat an active credit position like a spot holding and check it too late.

Oracle design deserves more respect than it gets. Liquidation is a rules engine tied to external price data. If the feed is slow, noisy, or easy to push around on a thin market, users feel that weakness directly. Good protocol design can reduce some of that risk. It cannot remove it.

I have seen the same mistake across lending books, perps, and looped yield trades. Users focus on entry conditions and ignore maintenance conditions. The trade looks safe at open. It becomes fragile a day later because funding changes, rates rise, or a collateral asset starts trading badly across venues. If you need a refresher on how that fragility shows up in supposedly defensive positions, review these stablecoin risk scenarios in DeFi strategies.

Cautionary tales usually start with confidence

The post-liquidation explanations are predictable. “It was a temporary dip.” “I had alerts set.” “The asset was liquid.” Those are not protections. They are assumptions that failed under stress.

The harsher lesson is that liquidation risk is rarely about one bad candle. It comes from running too close to the limit, with no clear plan for what to do if conditions worsen while you are offline. Crowded positioning makes it worse. When many wallets carry similar exposure, forced selling from one batch of liquidations can push the next batch closer to the line.

The practical response is dull by design. Keep more buffer than feels necessary. Size positions for bad conditions, not normal ones. Know which oracle your protocol uses and how liquidations are executed. Decide in advance whether you will add collateral, repay debt, or close the trade.

Discipline beats optimism here. Manual monitoring does not scale across fast markets, multiple protocols, and stacked positions. Modern risk tools help by tracking health metrics continuously, warning earlier, and automating parts of the response before a protocol turns your position into someone else's opportunity.

The Threat to Your Stablecoin Yield Strategy

A lot of stablecoin holders hear “yield” and think “cash-like income.” That's the wrong frame if borrowed capital is involved.

The danger usually enters through looping or recursive borrowing. You deposit a stablecoin, borrow against it, redeposit the borrowed funds, and repeat to amplify exposure to a spread. On paper, the strategy can look neat. In practice, you've built a tower where a small change in borrow conditions, collateral assumptions, or peg behavior can put the whole structure under pressure.

Stable doesn't mean liquidation-proof

Even if the asset is meant to be stable, the position can still be fragile. A stablecoin can wobble. Borrow costs can shift. Liquidity can dry up when everyone tries to unwind the same trade. You don't need a dramatic collapse to get hurt. You just need a strategy with too little margin for error.

That's why I like the retail liquidation analogy here. In surplus inventory markets, people who make money don't just chase cheap pallets. They calculate landed cost, freight, taxes, buyer's premium, and what happens if the manifest is wrong. The Closo guide on liquidation supply chains frames it as a supply-chain and pricing discipline problem, not a hunt for cheap goods. DeFi yield works the same way. Your real question isn't “what's the APY?” It's “what is my all-in cost of risk?”

For a deeper look at the non-obvious dangers inside supposedly defensive positions, read understanding stablecoin risks.

A better way to think about high APY

Use a checklist instead of excitement.

Where does the yield come from: Borrow demand, incentives, basis trade, protocol subsidy, or borrowed funds for increased returns?

What breaks the trade: Depeg, spread compression, rising debt cost, or thin exit liquidity?

How quickly can you unwind: One click, several steps, or not at all during volatility?

What happens if one assumption fails: Does yield shrink, or does the whole position become liquidation-prone?

High APY isn't automatically bad. But it often means the strategy has moving parts you must understand before you scale it.

The yield that survives stress is worth more than the yield that looks impressive only on calm days.

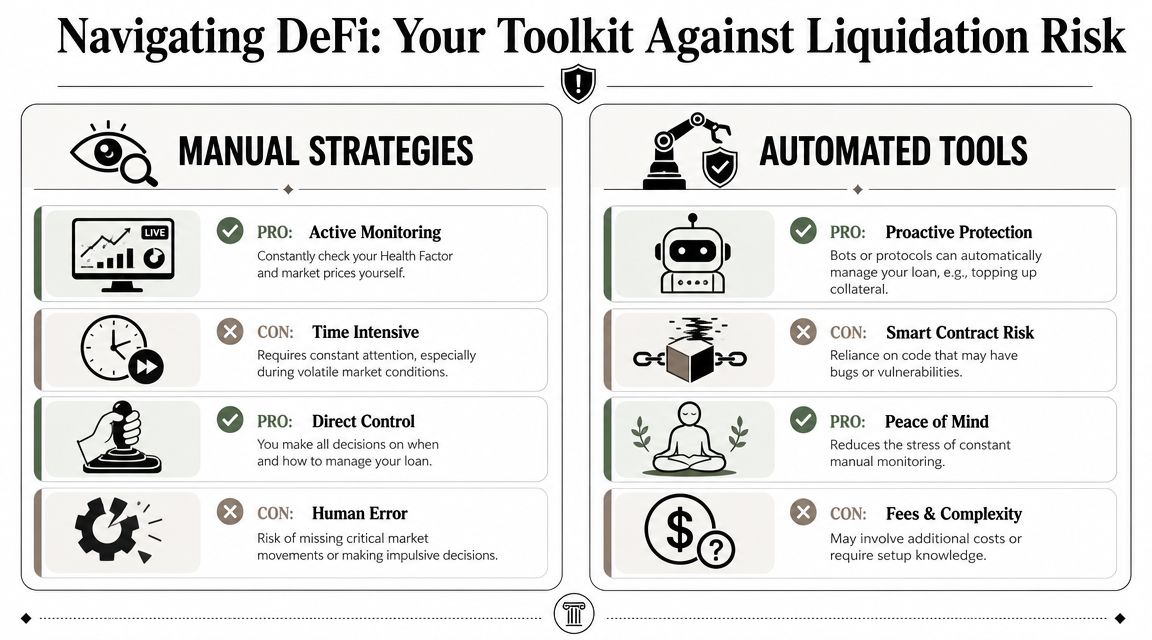

A Modern Toolkit for Managing Liquidation Risk

A borrowed position rarely fails because the dashboard looked confusing. It fails because the market moved fast, the response took too long, and the user needed a plan they had not prepared.

Manual oversight still has a place. Anyone using automation should understand what triggers a rebalance, what gets sold first, and where execution can fail. But manual control has a hard ceiling. Price shocks do not wait for office hours, and liquidation risk is most dangerous when attention is lowest.

What good manual defense looks like

Start with a response plan you can execute under stress.

Set a real buffer

Protocol limits are capacity numbers, not safety numbers. In practice, a position needs room for volatility, oracle lag, and bad fills.Choose your first action in advance

Decide whether stress means adding collateral, repaying debt, cutting size, or exiting. Making that call mid-panic is how small problems turn into forced sales.Watch both sides of the position

Traders often focus on collateral and ignore debt costs, borrow availability, or changing terms on the liability side.Prefer cleaner collateral

Thin liquidity and sharp volatility make recovery harder. Extra yield on paper can disappear the moment exit conditions get ugly.Treat alerts as inputs, not protection

An alert tells you to act. It does not act for you.

Where manual workflows break

The weak point is usually the operator.

Approach | Strength | Weakness |

|---|---|---|

Manual checks | Full user control | Missed moves during sleep, work, travel, or market chaos |

Simple alerts | Better awareness | Still requires fast action and clear judgment |

Rule-based bots | Faster responses | Can be rigid if market conditions change |

Managed automation | Continuous monitoring and execution | Requires trust in tooling and clear understanding of strategy limits |

The pattern is familiar in any risk-heavy system. Good control comes from thresholds, response rules, and clear ownership before conditions deteriorate. The Australian risk management framework guide is useful here because it reinforces a basic truth. Risk processes work when they are defined ahead of time, not improvised after the alarm goes off.

Why automation matters

DeFi now asks users to monitor too many variables at once. A position can look healthy, then weaken because liquidity thins, oracle inputs drift, debt terms change, or volatility spills over from another venue. None of that is exotic. It is normal operating reality for borrowed strategies.

That is why liquidation is not just a protocol mechanic. It is the test that exposes whether your process is real or cosmetic.

Manual tracking can work for small size and simple setups. It breaks down once positions span multiple protocols, chains, or dependencies. At that point, discipline has to be systematized.

What automation should actually do

Useful automation does more than chase headline returns. It should:

Monitor continuously: Track collateral health, debt conditions, liquidity quality, and protocol changes.

Filter bad setups: Reject opportunities with weak downside math, even if the top-line yield looks attractive.

React early: Reduce exposure or reallocate before a position drifts into a forced unwind zone.

Keep exits practical: Maintain enough liquidity and access that capital is not trapped when conditions change.

The right framework is on-chain risk management. The goal is not perfect prediction. The goal is faster, more consistent response while the problem is still manageable.

Yield Seeker fits that operating model. Its AI agent monitors and allocates stablecoin capital across DeFi opportunities in real time based on user settings, while keeping funds accessible without lockups or withdrawal fees according to the product information provided by the publisher. That does not remove risk. It changes how risk is handled. Instead of relying on scattered tabs, memory, and luck, the system keeps watching when the user cannot.

Better tools don't make borrowed positions safe. They make disciplined risk control more consistent.

That trade-off matters. Automation can reduce delay, enforce rules, and cut the odds of an avoidable liquidation. It also requires users to understand strategy limits, trust execution logic, and review how the system behaves in edge cases. For anyone serious about protecting capital, that is still a better operating model than hoping to be online at the exact wrong moment.

Surviving and Thriving in the World of DeFi

Liquidation is the central risk in DeFi involving borrowed capital. Not a side issue. Not an advanced topic for later. It's the mechanism that decides whether your strategy survives long enough to matter.

The users who last don't treat liquidation as bad luck. They treat it as a constant operating condition. They keep wider buffers, choose cleaner setups, and avoid strategies they can't explain under stress. They also accept that modern DeFi moves faster than manual oversight can reliably handle.

That's the shift. The goal isn't to eliminate risk. It's to manage it before the protocol manages it for you. Manual checks still matter. Alerts help. Structured playbooks help more. And increasingly, automated systems that monitor, filter, and reallocate in real time are the practical answer for anyone who wants yield without living inside dashboards all day.

If you want a hands-off way to pursue stablecoin yield with continuous monitoring and real-time allocation logic, Yield Seeker is built for that workflow. You can start with a small USDC deposit on Base, keep funds accessible, and let an AI agent handle the day-to-day protocol tracking that most users struggle to maintain consistently.