You’re probably in one of two camps right now.

Either you’ve ignored crypto for years because most of the conversation sounded like high-stakes gambling in a hoodie, or you already hold some USDC, USDT, or idle exchange cash and keep seeing people mention “yield” without ever explaining the work, the risks, or what to click.

That hesitation is rational. Crypto still asks too much of new users. Wallets, chains, bridges, gas, approvals, smart contracts, protocol names, changing rates. The industry often talks like everyone has time to become a part-time risk analyst. Most busy professionals don’t. They want to know one thing: can I put stable capital to work without turning this into another full-time dashboard problem?

That’s the part of crypto worth paying attention to. Not meme coin churn. Not heroic market timing. Stable yield.

The timing matters. In 2026, approximately 30% of American adults own cryptocurrency, and 61% of crypto owners plan to increase their investments, according to Security.org’s cryptocurrency consumer report. That tells you the market has moved beyond pure novelty. More people are looking for durable uses of crypto capital, not just lottery-ticket upside.

If you’re still getting your footing, a solid starting point is this beginner-friendly overview of crypto investing. It helps if the jargon still feels noisy.

The practical question isn’t whether crypto exists anymore. It clearly does. The practical question is which part of it deserves your attention, and which part deserves your skepticism.

Your Guide to Crypto Beyond the Hype

Most crypto explanations fail because they start in the wrong place. They start with ideology, token tickers, or market narratives. A better starting point is utility.

If you strip away branding and speculation, crypto is a way to move, store, and program digital value without depending entirely on one bank, one broker, or one payments company. Sometimes that matters a lot. Sometimes it doesn’t. The important part is understanding when it is useful.

A better mental model

Think of blockchain as a shared digital ledger. Not a magical one. Just a ledger that many computers keep in sync so participants can agree on who owns what.

That’s different from traditional finance, where a bank or brokerage updates the official record inside its own systems. In crypto, the record is shared across a network, and the rules for updating it are enforced by software.

A few core ideas matter more than the rest:

Wallets hold your access: A wallet doesn’t “store money” the way a leather wallet does. It stores the keys that let you control assets on-chain.

Smart contracts act like software-based financial rules: Instead of asking a bank employee or broker to process a product, users interact with code that executes predefined logic.

Networks are the rails: Ethereum, Base, Solana, and others are different environments where assets move and applications run.

Why this stopped being niche

Crypto is no longer a tiny side experiment. The global crypto market capitalization stands at $2.67 trillion as of early 2026, with milestones such as SEC approval of Bitcoin ETFs and Ethereum’s energy-efficient Merge helping cement crypto as a maturing asset class, according to CoinGecko market data.

That doesn’t mean every token deserves attention. It means the asset class itself now has enough depth that serious capital, infrastructure, and product design are showing up.

Crypto makes more sense when you stop asking, “Which coin will moon?” and start asking, “Which financial tasks can software do better, faster, or more transparently?”

For stable yield seekers, that shift is everything. You don’t need to care about every corner of crypto. You need a working model of how digital dollars move through programmable systems, because that’s where the practical opportunities start.

What Is Crypto Really A Practical Primer

You move cash into a savings account and expect two things. The balance should stay stable, and the process should not eat your week. People who come to crypto for yield usually want the same outcome. They are not looking for another speculative bet. They want a digital dollar they can put to work through software.

That is the practical starting point for stable yield. Learn the role of stablecoins, understand what DeFi does, and judge every opportunity by one question. Why does this payout exist?

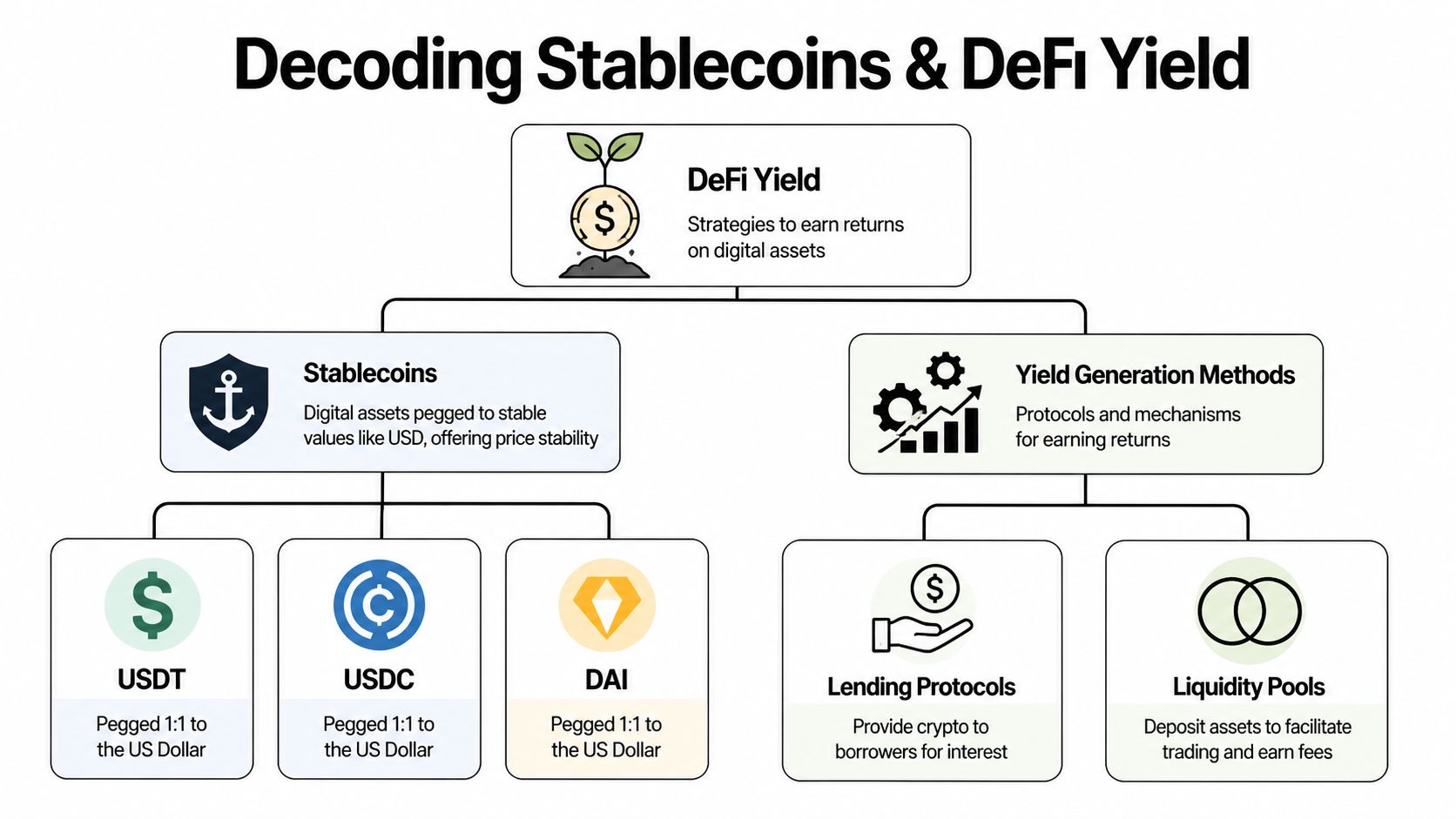

Stablecoins are the cash layer

Stablecoins are crypto assets built to hold a stable reference value, usually one U.S. dollar. In practice, they serve as the working cash of the on-chain economy. Funds move into stablecoins when traders want to reduce volatility, when operators need fast settlement, or when investors want yield without taking direct exposure to Bitcoin or smaller tokens.

Bitcoin behaves more like high-volatility macro exposure. Stablecoins function more like programmable cash.

That distinction matters. If the asset itself is swinging 10 percent while you are earning 5 percent, the yield barely matters. Stablecoin strategies are easier to evaluate because the base asset is designed to stay flat. The real question becomes whether the yield source is durable and whether the setup is worth the risk. If you want a more focused breakdown, this guide to earning stablecoin yield covers the mechanics in more detail.

DeFi is software-based finance

DeFi is a set of financial applications that run on blockchains. Instead of opening an account with a bank, users connect a wallet to software that handles lending, trading, collateral management, and yield distribution according to code.

That sounds abstract until you frame it in normal financial terms. A lending protocol is a money market run by smart contracts. A liquidity pool is a trading venue where users supply inventory and earn fees. A yield vault is a rules-based allocator that moves capital according to a defined strategy.

The key difference from traditional finance is operational. These systems are open, always on, and programmable. The trade-off is that the user takes more responsibility. There is no branch manager to call if you send funds to the wrong address or deposit into a weak protocol.

Where the yield comes from

“Earn yield” is too vague to be useful. The payout has to come from somewhere real.

Method | What you’re doing | Why yield exists |

|---|---|---|

Lending | Depositing stablecoins into a lending market | Borrowers pay to access liquidity |

Liquidity provision | Supplying assets to trading pools | Traders pay fees to swap |

Incentive programs | Participating in protocol growth programs | Protocols distribute rewards to attract capital |

This is the filter experienced users apply first. Capital earns a return because it performs a job. It funds loans, supports trading, or helps a protocol attract liquidity during a growth phase.

The safest habit is simple.

Practical rule: If you cannot explain the yield source in one plain sentence, do not deposit.

Why stablecoins matter so much

Stablecoins became central because they solve a basic operational problem. Crypto users need an asset that settles quickly, moves across platforms, and does not force a market view every time they hold cash for a few days.

That is why stable yield has become one of the few parts of crypto that busy professionals can evaluate rationally. You are not trying to predict the next hot token. You are deciding whether a software-based financial product can pay you for supplying useful capital, with risks you understand.

That is a much better frame for crypto than hype. It turns a noisy market into a cash management decision.

Decoding Stablecoins and DeFi Yield

The attractive part of DeFi isn’t just return. It’s access. A stablecoin holder can move from idle cash to earning yield without asking a bank for permission, waiting for business hours, or opening a stack of financial accounts.

That convenience is real. So is the complexity behind it.

Why the rewards pull people in

The upside is straightforward. On-chain markets can offer opportunities that traditional cash products often don’t surface to ordinary users with the same speed or flexibility. Capital can move quickly. Strategies can update quickly. Users can often enter or exit without the fixed structure that comes with many legacy products.

For teams managing stablecoin balances, that flexibility is operationally useful. Idle treasury funds don’t have to sit untouched while someone manually shops for rates every week.

Why the risks catch beginners off guard

The obvious risk is smart contract failure. If the code is flawed, funds can be exposed.

Less obvious risks matter just as much:

Protocol risk: A protocol can change incentives, governance, or exposure in ways that alter the strategy.

Counterparty design risk: Some products look decentralized on the surface but rely on concentrated admin powers or fragile dependencies.

Yield instability: What looks attractive today may fall quickly when liquidity moves or incentives end.

Execution risk: A poor entry, exit, or rebalance can reduce returns through slippage and fees.

Usability belongs on that list too. DeFi user retention drops 70% within 30 days due to UX friction, according to Consello’s analysis of mainstream adoption barriers. That tracks with what builders see in practice. New users don’t always fail because the strategy is bad. They fail because the process is exhausting.

What works better in the real world

The people who last in DeFi usually do three things differently.

They treat yield as a risk-adjusted decision: They don’t chase the highest number on a dashboard.

They prefer simple stablecoin strategies over complicated farms: Fewer moving parts usually means fewer hidden failure points.

They build a process for monitoring and re-evaluating positions: Yield is rarely “set and forget” when done manually.

A useful filter is whether a strategy reduces operational burden or adds to it. If earning yield means tracking five protocols, checking governance changes, watching liquidity conditions, and timing exits yourself, the headline return can become less interesting.

Some DeFi strategies fail not because the thesis is wrong, but because the operator gets tired before the strategy does.

The reward side of stablecoin yield is real. The friction side is real too. Users don’t need more access to protocols. They need a safer operating model for using them.

The Real Risks and Rewards of Earning Yield

DeFi yield sits in an unusual middle ground. It’s more dynamic than a bank savings product, but it isn’t automatically speculative in the way people often assume. Stablecoin strategies can be conservative by crypto standards. They still carry risks that traditional investors don’t always expect.

Rewards that matter

The best part of on-chain yield is control. You can often see where funds are deployed, move capital without waiting for office hours, and adapt to market conditions faster than you can in many legacy systems.

For operators and investors, the value usually comes from four traits:

Liquidity: Funds are often accessible without long lockups.

Transparency: On-chain positions are visible in a way many private products aren’t.

Programmability: Rules and strategies can be executed by software rather than spreadsheets and email chains.

Access: Smaller accounts can often participate in tools that used to be institution-only in practice.

Risks people underestimate

Beginners often focus on market risk and miss process risk.

A stablecoin can reduce price volatility, but it doesn’t remove the chance of interacting with a flawed protocol, signing the wrong transaction, or moving funds across the wrong network. Even experienced users make operational mistakes when they’re juggling wallets, bridges, approvals, and multiple dashboards.

Another issue is interpretation. A listed APY is not a promise. It can change because borrowing demand shifts, rewards end, liquidity deepens, or competitors attract capital elsewhere.

A simple decision filter

Before depositing into anything, ask:

Can you explain the yield source clearly?

Do you understand who controls key permissions?

Can you exit without unnecessary complexity?

Will you realistically monitor it after deposit?

If the answer to the last question is no, then your real problem isn’t finding yield. It’s managing it.

That’s where a lot of DIY strategies break down. The protocol may be fine. The user just doesn’t have the time or workflow discipline to manage it consistently.

Your First Safe Steps into DeFi Yield

The manual route into DeFi is useful to understand, even if you eventually automate it. Once you’ve done it yourself once, the moving parts stop feeling abstract.

Step one starts with the wallet

You need a self-custody wallet such as MetaMask or Coinbase Wallet. This is your on-chain account interface. It lets you connect to DeFi protocols, approve transactions, and manage assets directly.

The safety rule here is simple. Secure the wallet before funding it. Back up the recovery phrase properly, use strong device hygiene, and treat every signing prompt like a bank transfer authorization.

Buy stablecoins on a reputable exchange

Most beginners start by buying a dollar-pegged asset such as USDC on a centralized exchange. That part is familiar because it looks like regular fintech.

What matters next is choosing the right network for withdrawal. If you plan to use Base, withdraw to Base. A lot of early mistakes happen because users send the right asset on the wrong chain.

Move funds on-chain with intention

Once the funds reach your wallet, you’re ready to interact with DeFi apps. At this point, many people realize how much hidden operational work exists.

You need to evaluate the protocol, check whether the pool or vault matches your risk tolerance, review any approvals, and understand whether the strategy involves straightforward lending or a more complex structure.

A quick visual walkthrough can help make those screens less intimidating:

What a basic deposit flow usually looks like

Here’s the practical sequence most users follow:

Install and secure a wallet: Don’t rush this part. Most crypto mistakes happen before the “investing” even starts.

Fund the wallet with stablecoins: Keep the amount modest while learning the flow.

Leave a small balance for network fees: Transactions need gas.

Connect to a known DeFi interface: Review the app URL carefully before signing anything.

Approve token access, then deposit: These are usually separate transactions.

Verify the position after confirmation: Check that your deposit appears in the protocol and wallet history.

The hard part of DeFi usually isn’t the final deposit click. It’s the chain of small decisions before it.

Why the manual path wears people down

The DIY route teaches useful instincts, but it doesn’t scale well for busy users. You still need to compare protocols, monitor changing rates, decide when to move funds, and manage reallocation across opportunities.

That’s manageable if you enjoy on-chain operations. It’s less appealing if your real goal is to earn steady yield on stable balances with minimal maintenance.

Automating Your Strategy with an AI Agent

The cleanest reason to automate DeFi isn’t laziness. It’s discipline.

Manual yield management sounds easy when described in one sentence. In practice, it means repeated monitoring, repeated evaluation, repeated movement of capital, and repeated exposure to user error. Automation helps when the strategy is sound but the human workflow is inconsistent.

What an AI agent actually does

A useful AI agent for crypto yield should do more than chase the highest listed return. It should continuously evaluate opportunities, compare them against risk rules, and decide whether moving capital is worth the operational cost.

That includes details people often ignore, such as slippage, fees, liquidity conditions, and timing.

One practical input is market structure. AI agents can use Point of Control analysis to identify where trading volume is concentrated, helping time swaps or rebalances with lower slippage and better gas efficiency, as described in this overview of technical analysis and PoC in crypto trading. For yield management, that matters because execution quality affects net return.

Who benefits most from automation

Different users care about different parts of the workflow.

User type | Main problem | What automation helps with |

|---|---|---|

Busy professionals | No time to monitor protocols daily | Ongoing surveillance and capital movement |

Crypto-native users | Too many fragmented opportunities | Faster comparison and systematic rebalancing |

Web3 teams | Treasury management overhead | Consistent deployment and visibility |

The common thread is reduced manual burden. A good agent doesn’t remove judgment entirely. It packages repetitive judgment into a repeatable system.

The operating model that works

The most practical setup is usually a user-controlled account with a clear interface, transparent balances, and automation handling the repetitive portfolio work in the background. Some users still want to explore and learn. Others just want stablecoin balances to be deployed intelligently.

That’s where products built around AI agents become useful. If you want a non-technical explanation of the concept itself, this practical guide for business automation is a good reference because it frames AI agents as systems that monitor conditions and act within defined goals.

For DeFi specifically, this explanation of how to use AI agents is a helpful bridge from theory to on-chain application.

One example is Yield Seeker, which lets users deposit USDC on Base and have a personalized AI agent monitor and allocate capital across DeFi protocols in real time. The appeal isn’t that it makes crypto magical. It’s that it reduces protocol hunting, dashboard switching, and manual rebalancing into a simpler operating flow.

Automation is useful when it removes low-value repetition without hiding the important risks.

That’s the right standard. Not “hands-free at any cost.” Better monitoring, clearer controls, fewer avoidable mistakes.

The Future of Smart Crypto Investing

The strongest use case in crypto isn’t endless speculation. It’s giving ordinary users and small teams better financial tooling than they could build by hand.

Stablecoins made crypto more usable by creating a digital cash layer. DeFi made that cash productive. AI is starting to make the whole system manageable for people who don’t want to live inside wallets and dashboards.

That shift matters because financial access has never been only about permission. It’s also about comprehension. A tool isn’t accessible if its users can’t use it safely. As Brookings argues in its discussion of crypto and financial inclusion, progress has been uneven, and safer, more transparent tools are important if crypto is going to help more people rather than expose them to new forms of risk.

The practical future of crypto looks less like trading bravado and more like intelligent cash management. Better interfaces. Better monitoring. Better automation. Less noise.

If that future arrives, it won’t be because everyone became a crypto expert. It’ll be because the tools finally respected the user’s time.

If you want a simpler way to put stablecoins to work, Yield Seeker offers an AI-powered approach to monitoring and allocating USDC across DeFi protocols on Base. It’s designed for people who want transparent, risk-aware yield automation without manually tracking every opportunity themselves.