If you hold stablecoins today, you’ve probably felt this tension. You want yield, but you don’t want to wake up to a frozen issuer account, a broken peg, or a strategy so complex it turns passive income into a part-time job.

That’s where dai gets interesting. It isn’t just another dollar token. It’s a different design choice. Instead of asking you to trust a single company to hold dollars somewhere off-chain, dai asks you to trust transparent smart contracts, collateral rules, and governance on-chain.

For people chasing automated yield, that difference matters. The mechanics of dai shape where it earns, how risk shows up, and why some DeFi users prefer it over more centralized stablecoins. If you’ve read a dozen explainers that stop at “dai is decentralized,” this is the missing layer: what that means when you’re deciding where to park capital.

What Is the Dai Stablecoin

You have capital sitting in DeFi and want dollar stability without handing the full control stack to a single issuer. That is the problem dai was built to solve.

Dai is a dollar-pegged crypto asset created by the Maker system on Ethereum. Instead of being issued against cash in a company bank account, dai is created when users lock approved crypto collateral into on-chain vaults and borrow against it. The result is a stablecoin designed to hold close to one US dollar while staying native to DeFi.

A simple way to frame it is this. Centralized stablecoins work like digital casino chips issued by the house. You trust the house to redeem them. Dai works more like a secured credit line run by code. Users post collateral first, then mint dai against that collateral under public rules.

That design changes how you should use it.

If you are building or allocating into automated yield strategies, dai is not only a "safe parking" asset. Its structure affects where it earns, how it behaves in stress, and what kinds of risks your automation is taking. A strategy holding dai is exposed less to issuer freeze risk and more to collateral, smart contract, and governance risk. For anyone comparing stablecoin yield opportunities in DeFi, that distinction shapes portfolio construction.

New users often get tripped up by the term decentralized stablecoin. It does not mean unbacked, and it does not mean price stability appears by magic. Dai is backed by collateral. The system usually requires more collateral value than the amount of dai created, which is why people describe it as overcollateralized.

A practical analogy helps here. If you want to borrow $100 from a cautious lender, they may ask you to pledge $150 of assets first. Dai follows the same logic on-chain. That extra cushion is there because the collateral can move in price, and the system needs room to absorb those moves without the stablecoin breaking.

Another point worth being clear about is risk. Decentralized does not automatically mean safer. It means the failure modes move. With dai, you rely less on one company and more on protocol rules, liquidation mechanics, collateral quality, and governance decisions. For investors using automated tools such as Yield Seeker, that matters because the highest visible APY is only part of the job. The better question is whether the yield comes from a stablecoin whose underlying risks match the strategy horizon, rebalancing speed, and drawdown tolerance.

The History Behind MakerDAO and Dai

Back in 2017, if you wanted a crypto dollar, your options were mostly custodial. You had to trust a company to hold reserves and honor redemptions. Dai introduced a different model. It put the borrowing, collateral management, and liquidation logic on-chain, which is why MakerDAO became one of the early foundations of Ethereum finance.

The first version was Single-Collateral Dai, or SAI. It used only ETH as backing. That made the system easier to reason about, much like a lender that accepts only one type of property as collateral. The trade-off was concentration. If ETH went through a violent drawdown, the whole system had to absorb the shock through one asset and one liquidation pipeline.

From SAI to multi-collateral dai

Maker later expanded from SAI to Multi-Collateral Dai, which let the protocol accept a broader mix of collateral. That changed Dai from a focused experiment into a more adaptable credit system.

The practical benefit was diversification. A stablecoin backed by only one volatile asset has a narrow margin for error. A system that can draw support from multiple collateral types has more ways to manage stress, tune risk parameters, and keep Dai useful across different market regimes.

For anyone building automated yield strategies, this history is not trivia. It explains why Dai became a workable base asset for more than simple holding. Yield tools need a stablecoin that can remain relevant through changing market structure, because automation works best when the asset underneath it can survive more than one cycle.

The March 2020 stress test

The clearest test came during the March 2020 market crash. Dai moved off peg under extreme pressure before returning closer to parity. That episode exposed how a decentralized stablecoin behaves when collateral prices fall fast, liquidity thins out, and users rush for safety at the same time.

That is the kind of event yield farmers should study.

If you run an automated strategy on a platform like Yield Seeker, you are not only choosing an APY source. You are choosing the failure modes sitting underneath that APY. During stress, Dai can trade above or below a dollar, borrowing demand can spike, liquidation conditions can tighten, and yields can swing much faster than a dashboard suggests. A bot that reallocates into the highest advertised rate without understanding those mechanics can end up chasing temporary distortions instead of durable yield.

Two lessons from that period still matter:

Stress exposes the weak points: Dai’s peg deviation showed how liquidity shortages and fast deleveraging can pressure a decentralized system.

Recovery is part of the design: Maker adjusted incentives and risk settings, and the protocol continued operating without a traditional issuer stepping in with bank-held reserves.

Practical rule: Don’t judge a stablecoin only by whether it has ever moved off peg. Judge it by what caused the move, how the system reacted, and whether those mechanics fit the time horizon of your yield strategy.

There is one more historical detail worth knowing. MakerDAO later rebranded to Sky, while Dai stayed embedded in the same broader ecosystem. In practice, many users, dashboards, and strategy builders still say MakerDAO because that name is firmly tied to DeFi’s early architecture and to the way Dai is understood across the market.

How Dai Maintains Its Dollar Peg

Say you want dollar exposure inside DeFi, but you also want to put that capital to work in lending pools, liquidity strategies, or an automated allocator like Yield Seeker. The peg is what makes that possible. If dai drifts too far from one dollar, every downstream yield number becomes harder to trust because your "stable" base asset is adding its own risk.

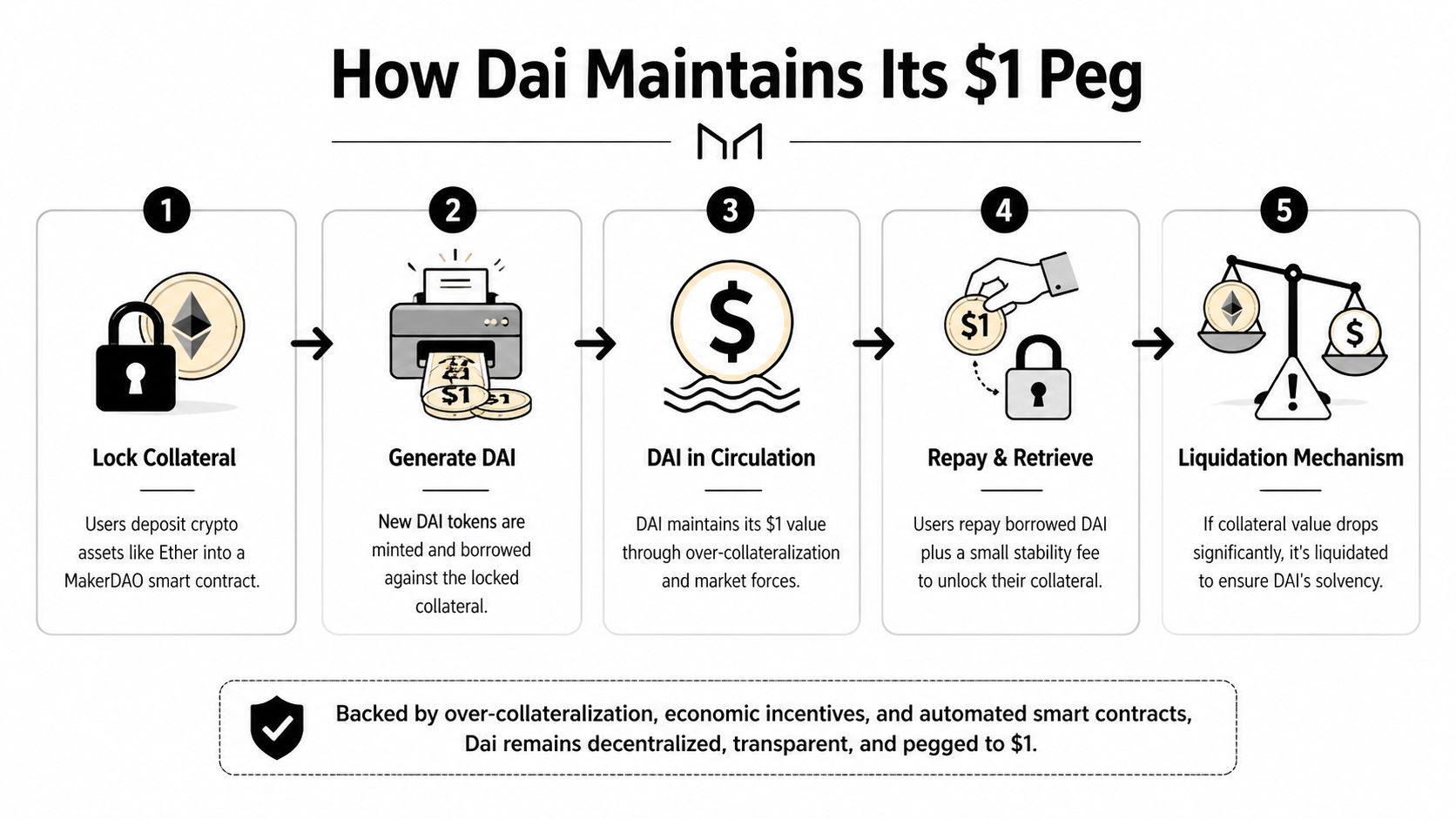

Dai maintains its peg through a system of overcollateralized loans, liquidations, and parameter changes set by governance. A simple way to picture it is a secured credit line. You post more value than you borrow, the system tracks your safety margin, and it sells collateral if that margin gets too thin.

Step one lock collateral

A user deposits approved crypto assets into a Maker smart contract. Older documentation often calls these positions CDPs, short for collateralized debt positions. In current usage, they are usually called Vaults.

The label is less important than the mechanics. The protocol holds collateral on-chain and records how much dai has been generated against it.

Step two generate less dai than the collateral is worth

This is the foundation: overcollateralization.

If a Vault holds more value than the dai created from it, the system has a cushion against price swings. That cushion is the first line of peg defense. Crypto prices move fast, so dai is not minted at a one-to-one ratio against volatile collateral.

A practical example helps. If you deposit ETH worth more than the amount of dai you want to generate, you are leaving room for ETH to fall without immediately putting the system at risk. For a yield farmer, that buffer is not just protocol trivia. It affects whether using self-generated dai is a stable funding source or a liquidation risk disguised as cheap capital.

Step three pay the stability fee

Generating dai has a cost. The stability fee works like the interest rate on the position.

That fee matters because it influences supply. If borrowing dai becomes expensive, fewer users will open or expand Vaults. If borrowing becomes cheaper, creating new dai is more attractive. Governance uses that knob to influence how much dai the market wants to generate and hold.

For automated yield strategies, this matters more than many guides admit. A high lending APY on dai can look attractive, but if the cost to generate dai rises at the same time, the spread can shrink or disappear. The useful question is not "What is the dai yield?" It is "What is the net yield after funding cost, liquidation risk, and gas?"

Step four repay and release collateral

When the borrower wants to close the position, they return the generated dai and pay the applicable fee. The smart contract then releases the collateral.

This creation and repayment loop is part of what keeps dai close to one dollar in practice. Users can generate dai when it is useful and retire dai when the trade no longer makes sense. That flexibility helps the market pull supply in and out instead of relying on a company treasury to issue or redeem tokens manually.

Step five liquidation protects the system

If collateral falls too far, the Vault can be liquidated. That process protects dai holders by trying to ensure the system remains backed even when markets move hard.

The logic is straightforward:

Collateral drops in value: The Vault becomes less safe.

The required ratio is breached: The position is eligible for liquidation.

Collateral is sold: The system covers the outstanding dai exposure.

If you mint dai against volatile collateral, your primary risk is the collateral, not the stablecoin label on the borrowed asset.

That distinction matters on Yield Seeker and similar platforms. An automated strategy can move dai between lending venues with very little friction. It cannot save a user who funded that dai by running an aggressive Vault that gets liquidated during a market drop. Stable asset strategy selection and collateral management are two separate jobs.

Why this works in practice

Dai's peg is maintained by several mechanisms working together, not by a pile of dollars sitting in a bank account. Collateral buffers absorb normal volatility. Liquidations deal with undercollateralized positions. Stability fees shape borrowing demand. Market participants also arbitrage deviations when dai trades meaningfully above or below one dollar.

The result is a peg that is dynamic rather than fixed by decree. It usually behaves the way stablecoin users want, but it does so through incentives and risk controls that can tighten under stress. That is why dai is often a strong base asset for automated yield, but not a risk-free one. If you want a broader framework for evaluating those trade-offs, this guide to stablecoin risk in real yield strategies is a useful companion.

For investors using automated allocators, the practical takeaway is simple. Dai is most useful when you treat peg mechanics as part of your yield analysis. A strategy earning a bit less on a stable, liquid venue can be better than a higher posted APY that depends on expensive dai funding or collateral exposure you cannot monitor closely.

Understanding Dai Governance and Risks

Dai isn’t run like a fintech app with a management team making unilateral calls behind closed doors. It’s governed through MakerDAO, where MKR token holders vote on core parameters such as accepted collateral and stability settings. That structure is part of what makes dai decentralized, but it also introduces its own risks.

Governance sounds abstract until you connect it to the user experience. The assets allowed into the system, the terms under which users generate dai, and the protocol’s reaction to stress all depend on decisions made by token holders. If those choices are good, the system adapts. If they’re poor, users inherit the consequences.

For a broader framework on what stablecoin risk looks like in practice, this guide on understanding stablecoin risks is a useful companion.

Smart contract risk

Dai lives in smart contracts. That’s the source of its transparency, but also the source of a category of risk that bank-issued dollars don’t have in the same way.

If the code contains a bug, if an integration behaves unexpectedly, or if a liquidation mechanism fails under pressure, users can face losses even when the theory looks sound. Smart contract risk is hard because it often stays invisible until conditions are abnormal.

This matters even more when dai is used inside stacked DeFi strategies. Holding dai in a wallet is one risk profile. Supplying dai to a lending market, then routing receipts into another protocol, is a different one.

Collateral risk

Dai is only as sturdy as the assets and rules behind it. The verified data states that the system expanded beyond ETH to accept a wider set of collateral, which improved diversification. But diversification doesn’t erase market risk.

A collateral asset can fall quickly. Correlations can rise when markets panic. Liquidity can disappear right when the protocol needs orderly liquidation.

Here’s the practical way to look at it:

Volatile collateral creates pressure: Fast price drops can push Vaults toward liquidation.

Complex collateral adds judgment calls: More asset types mean more governance work in setting risk parameters.

Stress can expose hidden weak points: A collateral model that looks safe in normal trading may behave differently in a disorderly market.

The safest way to use dai is often not to mint it yourself, but to decide whether holding or deploying dai fits your own risk budget.

Governance risk

Governance is the least discussed dai risk because it’s harder to picture than a code exploit or a market crash. But it’s real.

MKR holders decide policy. They can choose collateral types, fees, and system-level adjustments. If governance becomes inattentive, overly political, or too slow during market stress, users may feel the effects. Decentralization doesn’t remove human error. It redistributes it.

A quick way to separate the three risk buckets is this table:

Risk type | What can go wrong | Why users should care |

|---|---|---|

Smart contract risk | Code or integration failure | Funds can be affected even if the peg concept is sound |

Collateral risk | Backing assets lose value sharply | Dai’s support system can come under pressure |

Governance risk | MKR voters make weak decisions | Protocol settings may become less resilient |

The point isn’t that dai is uniquely dangerous. The point is that its risks are legible. You can inspect them, debate them, and build around them. That’s a meaningful advantage for disciplined DeFi users.

Dai vs USDC and USDT A Comparison for Investors

You want to park capital in a stablecoin, then route it into an automated strategy. The first question is not yield. It is what kind of system you are trusting while that capital waits, moves, and earns.

That is the practical split between DAI, USDC, and USDT. USDC and USDT ask you to trust an issuing company, its banking relationships, its reserves, and its ability to honor redemptions under pressure. DAI asks you to trust a protocol. Its collateral rules, liquidation design, and governance process matter more than a corporate balance sheet.

For an investor, that difference affects more than philosophy. It changes where a yield strategy can break, freeze, or keep working.

Key Decision Criteria

A useful comparison starts with the job you need the stablecoin to do.

If you need the deepest exchange liquidity and broad support across centralized venues, USDC and USDT often have the edge. If you want a dollar asset that fits naturally into permissionless DeFi rails, DAI has a different advantage. It behaves more like system-native cash inside crypto, which can matter when you are using vaults, lending markets, or automated allocators.

Three criteria usually decide the choice:

Control: Who can influence issuance, redemptions, or policy?

Visibility: Can you inspect the mechanism on-chain, or are you relying mostly on issuer reports and attestations?

Failure mode: Is the bigger risk a company and its financial partners, or a protocol and its incentive design?

Those questions matter more for automation than many guides admit. If you are using a platform that rotates funds between opportunities, the stablecoin is not just the asset you hold. It is the settlement layer for the strategy. A token with broad venue support may open more routes. A token with stronger on-chain composability may fit DeFi-native automation more cleanly.

DAI vs USDC vs USDT key differences

Feature | Dai (DAI) | USD Coin (USDC) | Tether (USDT) |

|---|---|---|---|

Issuance model | Generated against on-chain collateral through a protocol | Issued by a centralized company | Issued by a centralized company |

Primary trust assumption | Smart contracts, collateral design, governance | Issuer operations and reserve management | Issuer operations and reserve management |

Transparency style | On-chain and protocol-native | More dependent on issuer reporting and off-chain reserve processes | More dependent on issuer reporting and off-chain reserve processes |

DeFi fit | Strong for permissionless strategies and crypto-native automation | Strong due to broad integration and liquidity | Strong due to broad integration and liquidity |

Main risk emphasis | Smart contract, collateral, governance | Counterparty and regulatory exposure | Counterparty and regulatory exposure |

Liquidity profile | Useful but more niche in some DeFi routes | Broad | Broad |

What actually matters for yield users

The common summary is too shallow. DAI is decentralized. USDC and USDT are centralized. True, but that does not help much when you are deciding how to deploy cash.

A better frame is operational. USDC and USDT are often easier to move across high-volume markets, and that can improve execution for strategies that depend on tight spreads or frequent reallocations. DAI is often easier to integrate into DeFi systems where on-chain transparency and permissionless access matter more than issuer redemption rails.

That trade-off shows up quickly in yield strategy design. Suppose an automated system is scanning lending pools, DEX pools, and savings-style products. If the best opportunities sit inside DeFi-native protocols, DAI can be a natural base asset. If the strategy needs the widest possible liquidity across chains, venues, or off-ramps, USDC may reduce friction. USDT often matters where raw market depth is the priority.

This is why stablecoin selection should sit inside strategy design, not after it. A good starting map is this guide to stablecoin yield strategies, which helps compare where each stablecoin type tends to fit.

One more point gets missed. Some investors diversify across stablecoins for the same reason they diversify across protocols. They are spreading exposure across different failure modes. That does not remove risk, but it can prevent one weak link from defining the whole yield stack.

For platforms automating yield decisions, that distinction is practical. Choosing DAI can mean accepting protocol and governance risk in exchange for stronger alignment with permissionless DeFi. Choosing USDC or USDT can mean accepting issuer risk in exchange for broader liquidity and market access. The right answer depends on what your strategy needs to optimize: composability, liquidity, censorship resistance, or operational simplicity.

Practical Strategies for Earning Yield with Dai

You park a treasury balance in dai because you want dollar stability, but idle stablecoins have an opportunity cost. A week later, rates move on Aave, a stablecoin pool on a DEX starts paying better fees, and the DSR looks safer but lower effort. The practical question is not whether dai can earn yield. It is which route matches your risk budget, operating time, and need for automation.

Dai works well for yield strategies because it is already native to DeFi. That matters when an automated allocator is comparing places to park capital. The asset can move through lending markets, liquidity pools, and savings-style products without depending on an issuer redemption workflow. If you want a broader framework for comparing these routes with other stablecoins, this guide to stablecoin yield strategies is a useful reference.

Lending dai on money markets

Lending is usually the cleanest starting point. On protocols such as Aave or Compound, you deposit dai into a shared pool and earn from borrower demand.

The appeal is clarity. Your return comes from one main source, borrowing activity, so it is easier to explain and easier to monitor. For someone building or using automated strategies, that simplicity matters. A lending position is often easier to score than an LP position because the variables are fewer: utilization, protocol quality, supply rate, and any changes in market stress.

The trade-off is that yield moves. A pool paying well this week can cool off fast if fresh capital floods in or borrowing demand drops. You are also taking smart contract and protocol risk, even if the strategy itself feels familiar.

Providing liquidity on a DEX

DEX liquidity can pay more, but the income source is different. You are earning trading fees, not borrower interest, and your outcome depends on how the pool rebalances as prices move.

A stablecoin pair such as dai-USDC is often easier to reason about than dai paired with a volatile asset. The spread between the two tokens is usually smaller, so the position behaves more like a fee-generating cash buffer than a directional bet. Even then, pool design matters. Concentrated liquidity, incentives, volume quality, and pool depth all change the actual return.

Many guides stop too early. Headline APY is only part of the story. For automated yield systems, LP positions need stricter monitoring because fee income can look attractive right before volume fades or pool composition shifts against you.

Using the Dai Savings Rate and vault-style products

The Dai Savings Rate, or DSR, is the closest thing to a home-base yield option for dai holders. Instead of sending capital across multiple protocols, you keep the strategy closer to Maker's own system.

That can make the position easier to justify in a portfolio. The mental model is simple. You hold dai and earn a protocol-defined rate through a native mechanism rather than chasing fees across a stack of external apps.

Vault-style products sit one layer higher. They often route funds into lending, liquidity, or other on-chain strategies for you. The benefit is convenience. The cost is another layer of design, another set of contracts, and another manager or ruleset to evaluate.

How to choose among them

A useful filter is to ask what must be true for the yield to continue.

Choose lending if you want the most direct stablecoin income path and can accept variable rates tied to borrowing demand.

Choose LP positions if you understand pool behavior and are comfortable monitoring fee quality, rebalancing effects, and pool-specific risk.

Choose DSR or vault routes if you prefer a simpler operating model and want less day-to-day strategy work.

A good rule is simple: if you cannot explain where the yield comes from in one sentence, the position is probably too complex for a first allocation.

Dai also changes portfolio behavior in a useful way. It usually gives you a way to earn on-chain income without adding the same price volatility you would take on with reward tokens or unhedged crypto assets. That makes it a practical base asset for automation. The system can hunt for better risk-adjusted opportunities while you keep the unit of account stable.

Teams building these workflows also need a reliable way to collect docs, protocol pages, and market context for internal monitoring. A service like scrape api can help gather web content in a machine-readable format when you are evaluating protocols or tracking changes across multiple dai yield venues.

Automating Dai Yield Strategies with Yield Seeker

Dai is a strong candidate for automation because its design is inspectable. Collateral logic is on-chain. Governance is visible. Yield opportunities often emerge across lending markets, vaults, and Layer 2 environments in ways that are hard to track manually.

That’s the gap automation can close.

A time-constrained investor usually doesn’t struggle with the idea of dai. They struggle with execution. Which protocol is worth using today? Has risk changed? Is a yield opportunity attractive because it’s efficient, or because the market hasn’t priced in a problem yet?

Where automation helps most

A useful automated workflow does three things well.

First, it scans opportunities continuously. That matters because dai yield can shift across chains and venues, including environments like Base that many general explainers barely cover.

Second, it compares risk, not just headline return. A smart system should treat a dai lending opportunity differently from a dai LP route or a vault allocation. The income source is different, so the monitoring should be different too.

Third, it cuts research overhead. Teams building these systems often need reliable ways to pull protocol pages, docs, and market data into internal workflows. If you’re evaluating tooling for that pipeline, a service like scrape api can be relevant for collecting web content in a machine-readable format.

A practical dai automation playbook

Here’s a sensible way to use automation with dai:

Start with your stablecoin base. If most of your capital sits in USDC, decide whether moving a portion into dai serves a clear purpose, such as accessing a better-aligned strategy.

Use risk buckets. Separate low-complexity lending from more active LP or vault exposure.

Monitor strategy-specific signals. For dai, that can include protocol changes, collateral-related developments, and governance decisions that may affect downstream opportunities.

Keep liquidity optional. Don’t trap all your stablecoin capital in one route if your goal is flexible income management.

Dai’s character is important. Because it’s decentralized and on-chain, it can fit risk-aware automated systems well. But automation shouldn’t hide the trade-offs. It should surface them clearly enough that you can still make deliberate choices.

The best use of dai in an automated setup usually isn’t “replace every stablecoin with dai.” It’s more selective than that. Use dai where its transparency, DeFi composability, and risk profile give it an edge. Use something else when liquidity depth or operational simplicity matters more.

A good system doesn’t romanticize decentralization. It treats it as one input in portfolio design.

If you want a simpler way to put these ideas into practice, Yield Seeker helps you deploy stablecoins into DeFi yield strategies with an AI-guided workflow built for clarity, flexibility, and ongoing monitoring.