You probably already have the setup. Some cash is in a bank account earning little. Some capital is parked in USDC or another stablecoin because you want speed, flexibility, or dry powder for the next move. You’ve heard decentralized finance can put those assets to work, but every time you look closer, the environment feels like a maze of wallets, bridges, acronyms, and avoidable mistakes.

That hesitation is rational. DeFi has spent years attracting two extremes: academic explainers that stop at definitions, and “degen” content that treats risk like a personality trait. Most smart professionals need something else. They need a practical map. What matters, what doesn’t, where yield comes from, and how to participate without turning portfolio management into a second job.

Your Guide to the New Financial Frontier

Decentralized finance matters now because it’s no longer a side experiment. The market reached USD 48.4 billion in total value locked in 2024 and is projected to reach USD 1,078.5 billion by 2035 at a 32.6% CAGR, according to MetaTech Insights' DeFi market analysis. In that same market view, Savings & Yield Farming held 36.52% market share in 2025, which tells you where real user demand sits: people want onchain cash management, not just speculation.

That shift matters for stablecoin holders more than almost anyone else. If you already hold digital dollars, you already sit near the main entry point into decentralized finance. You don’t need to buy a volatile governance token or become a full-time trader to benefit from the system. You need to understand where risk sits, how protocols use your capital, and which tools reduce complexity instead of adding more of it.

Why busy professionals are paying attention

Traditional finance bundles services. A bank handles custody, yield, payments, and reporting inside one interface. DeFi unbundles them. That creates more choice, but it also pushes more responsibility onto the user.

For professionals and treasury operators, that changes the due diligence checklist. You’re no longer just asking whether a platform has an attractive rate. You’re asking whether the underlying systems are well controlled, transparent, and operationally mature. That’s why broader fintech governance frameworks still matter, even in crypto-native settings. If you want a useful reference point for how financial software teams think about controls and trust, SOC 2 for Fintech Companies is worth reviewing.

Practical rule: Treat decentralized finance like a new operating system for financial services, not like a single app.

What changed

What used to require deep crypto fluency now has better interfaces, clearer workflows, and more specialized infrastructure. That doesn’t remove risk. It does mean the gap between “I understand this” and “I can use this sensibly” is much smaller than it was a few years ago.

For stablecoin holders, that creates a simple question: if your digital dollars are already onchain, should they stay idle?

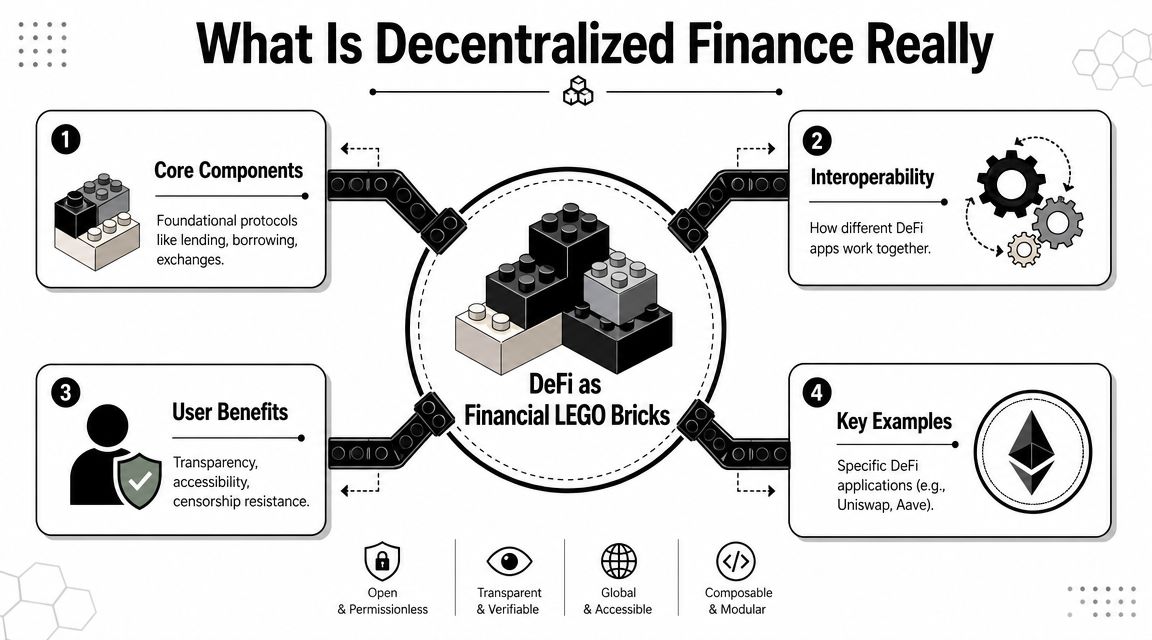

What Is Decentralized Finance Really

Most explanations say decentralized finance is “finance on a blockchain.” That’s technically fine and practically useless.

A better way to understand it is this: DeFi is a set of financial LEGO bricks. Each brick does one job. One protocol swaps assets. Another lends them. Another routes trades. Another manages collateral. Because these bricks are open and programmable, developers and users can connect them in ways that would be slow, expensive, or completely impossible inside traditional financial rails.

The three properties that matter

Open access is the first one. In many DeFi systems, users interact with software directly through a wallet instead of opening an account through a conventional financial intermediary.

Transparency is the second. The contracts are visible, transaction activity is observable onchain, and the rules are usually embedded in code rather than hidden in internal process.

Composability is the third, and it’s its defining feature. One application can plug into another. That means a wallet, a lending market, a DEX, and a yield strategy can work together like modular parts.

If you want a simple walkthrough of these mechanics, this explainer on how DeFi works is a useful companion.

Why that changes the game

Traditional finance works like a closed campus. Each institution controls its own products, customer relationship, and internal ledger. Moving value across institutions often means delays, fees, and operational friction.

DeFi works more like shared infrastructure. Developers can build on top of existing rails instead of rebuilding the whole stack from scratch. Users can move capital between services without asking one company for permission to integrate with another.

DeFi isn’t special because it removes every middleman. It’s special because it turns many financial functions into software that other software can use.

That’s why decentralized finance isn’t just another trading venue. It’s a production environment for financial products. The most useful way to approach it is not as a bet on crypto culture, but as a new distribution model for savings, payments, lending, and market access.

Understanding the Core Building Blocks of DeFi

Once you stop treating DeFi like one giant category, the system becomes easier to understand. Most activity that matters for stablecoin holders comes down to a small set of building blocks.

Stablecoins are the foundation

Stablecoins are onchain assets designed to track a fiat currency, usually the U.S. dollar. Think of them as the cash layer of decentralized finance. They’re the unit people park in, transfer, lend, borrow against, and deploy into strategies.

For a professional user, stablecoins solve a practical problem. They let you operate inside crypto infrastructure without taking full exposure to crypto price swings. That doesn’t make them risk-free. It makes them usable.

DEXs and AMMs are the marketplaces

A decentralized exchange, or DEX, lets users swap one asset for another directly onchain. Many DEXs rely on automated market makers, or AMMs, which price trades using liquidity pools instead of traditional order books.

The easiest analogy is an automated currency kiosk. You walk up with one asset, the machine quotes a price based on the assets available in the pool, and the swap executes according to predefined rules.

If you want a broader business-oriented primer on how distributed ledgers support visibility and verification, this piece on blockchain technology gives useful context.

Lending protocols are the credit engine

Lending protocols do what the name suggests. Suppliers deposit assets. Borrowers post collateral and draw against it. The protocol enforces the rules automatically, including collateral thresholds and liquidations.

That’s one reason DeFi feels mechanical compared with bank lending. A bank underwrites people and businesses through documents, judgment, and regulation. A DeFi lending market underwrites collateral first.

Liquidity pools are the fuel

Liquidity pools are shared pools of assets that power swaps and, in some cases, other strategies. Users who contribute capital help make markets function. In return, they may earn fees or other forms of compensation, depending on the protocol design.

This breakdown of what liquidity pools are is helpful if you want a deeper look at how they work under the hood.

Primitive | Purpose | Popular Example |

|---|---|---|

Stablecoins | Hold and move dollar-like value onchain | USDC |

Decentralized exchanges | Swap assets without a centralized intermediary | Uniswap |

Lending protocols | Match suppliers of capital with collateralized borrowers | Aave |

Liquidity pools | Provide assets that enable trading and fee generation | Uniswap pools |

The shortcut that saves time

You don’t need to master every niche protocol. For stablecoin yield, focus on four questions:

What asset am I depositing

Stablecoins behave differently from volatile assets in both risk and expected return.What mechanism generates the return

Lending, trading fees, and incentives are not interchangeable.Who can withdraw first

Liquidity terms matter more than headline yield.What happens when stress hits

Good protocols are built for ugly conditions, not just calm ones.

How Stablecoin Yield Is Actually Generated

Yield in decentralized finance isn’t magic. Someone pays for access to capital, liquidity, or execution. If you can’t identify that economic flow, you shouldn’t trust the return.

In 2025, DeFi protocols earned over $16 billion in revenue, with $30.3 billion in total transaction fees, according to KuCoin’s 2025 DeFi industry revenue report. The same report notes that lending revenues climbed to $15 million to $25 million per month, while Top 10 perp DEX trading volume rose 80.8% in Q4 2025, moving from $1.8 trillion in Q3 to $3.2 trillion. That’s the key point: returns come from actual activity inside the system.

Lending interest

This is the cleanest source of stablecoin yield. Borrowers deposit collateral and pay to access liquidity. Lenders supply stablecoins and receive a share of that interest.

You can think of it as a floating-rate money market with automated collateral enforcement. Rates move with demand. When more traders, arbitrageurs, or other users need stablecoins, lenders usually earn more.

Trading fees

DEXs need liquidity to process swaps. Liquidity providers make those swaps possible. In exchange, they receive a portion of trading fees.

This income is linked to market activity, not just borrowing demand. In volatile markets, trading can increase. That can lift fee generation, though the strategy risk can also get more complicated depending on the assets in the pool.

The safest-looking yield often comes from the simplest mechanism. If the explanation for the return is hard to follow, the risk usually is too.

Incentives and bootstrapping rewards

Some protocols distribute token incentives to attract deposits and deepen liquidity. This can be useful, but it’s the least durable of the three major sources.

Incentives are best treated as temporary compensation for helping a newer system grow. They can enhance returns, but they shouldn’t be the main reason you enter a position.

A useful filter is to ask one blunt question: if the incentives disappeared tomorrow, would the strategy still make sense?

Navigating the Key Risks in DeFi

The most expensive mistake in decentralized finance is chasing yield before mapping risk. Every strategy has a risk stack. The job isn’t to eliminate risk completely. The job is to know which risks you’re accepting and which ones you’re being paid for.

Smart contract risk

A DeFi protocol is software that controls value. If the code has a flaw, users can lose funds. Audits help, reputation helps, long operating history helps, but none of those are the same as a guarantee.

Mitigation starts with discipline:

Use battle-tested protocols

Older, widely used systems have faced more real-world pressure than fresh launches.Prefer simple strategies

Every extra layer, wrapper, or dependency increases the attack surface.Avoid concentration

Spreading capital across separate venues can reduce single-point failure risk.

Strategy risk and impermanent loss

Many newcomers hear “liquidity provision” and think “passive income.” Sometimes it is. Sometimes it’s a trade with a hidden cost.

If you provide liquidity to a pool with two volatile assets, your holdings can drift relative to holding the tokens outright. That’s impermanent loss. Stablecoin-based strategies often avoid the sharpest version of this problem, but strategy design still matters. You need to know whether you’re lending, market-making, or funding a more complex loop.

Don’t ask only, “What’s the yield?” Ask, “What position am I synthetically taking to earn it?”

Compliance and counterparty quality

The operational and legal layer matters more than many crypto-native users admit. The U.S. Treasury has warned that some DeFi services are structured to evade AML and CFT obligations, and that illicit actors exploit non-compliant jurisdictions and weak cybersecurity. For users, that’s a practical reminder to choose transparent, reputable, and ideally compliant protocols, as outlined in the U.S. Treasury’s DeFi risk review.

That doesn’t mean every user needs to become a lawyer. It means you should prefer systems with visible teams, clear documentation, understandable architecture, and risk controls you can inspect.

A workable approach

Most professionals do better with fewer moving parts:

Start with stablecoins, not volatile pair farming

Use protocols you can explain in one sentence

Keep funds accessible

Review where the yield comes from before you deposit

Let tools monitor conditions if you can’t watch markets all day

That’s not conservative for the sake of appearances. It’s how people stay in the game long enough to benefit from the upside.

Your Practical Path to Earning Stablecoin Yield

Most stablecoin holders begin the same way. They open a few dashboards, compare rates across lending markets and DEXs, read scattered posts on X or Discord, then move funds manually. For a while, that works.

Then the friction shows up. Rates change. Incentives rotate. Gas costs matter. A protocol that looked sensible last week no longer looks attractive today. Manual yield management starts to resemble spreadsheet operations attached to a live trading desk.

The manual path breaks for the same reasons

The challenge isn’t just finding yield. It’s maintaining a process.

A person doing this by hand has to evaluate protocol quality, watch liquidity conditions, compare opportunities, rebalance capital, and decide when a yield spike is worth the extra risk. That may suit an active onchain operator. It doesn’t suit most busy professionals or teams managing idle stablecoin balances.

Three pain points usually force a change:

Fragmentation

Capital sits across multiple apps, wallets, and interfaces.Monitoring burden

Good decisions require repeated review, not one-time setup.Execution fatigue

Even simple reallocations take attention and create room for mistakes.

Why automation is the logical next step

AI automation is a natural fit. The point isn’t to hand your judgment to a black box. The point is to automate the repetitive work that humans do poorly over time: constant scanning, comparing, reallocating, and checking whether a strategy still matches the risk you intended to take.

For stablecoin holders, the best automation tools should do a few things well. They should monitor protocols continuously, keep the user informed, preserve liquidity where possible, and make the strategy legible rather than mysterious.

If you want a focused overview of this category, this guide to stablecoin yield covers the basic setup choices.

A short demo helps show what that workflow looks like in practice:

What a practical setup looks like

One example is Yield Seeker, an AI-powered platform that lets users deposit USDC on Base and have an AI agent monitor and allocate capital across DeFi protocols in real time. The model is straightforward: reduce the research burden, keep funds accessible, and automate yield decisions for users who want risk-aware exposure without manually hunting across fragmented venues.

That approach makes sense because it matches how decentralized finance is evolving. The first era rewarded people who could deal with chaos manually. The next era rewards systems that make sensible decisions repeatable.

If you hold stablecoins, the practical path is usually not “learn every protocol.” It’s “choose a structure that matches your time, your risk tolerance, and your need for liquidity.”

Frequently Asked Questions for DeFi Users

Do I need a large amount of capital to start

No. What matters more is choosing a setup with sensible fees, clear strategy logic, and enough flexibility to move if conditions change. Small balances can still be useful for learning workflows and testing how a platform behaves before allocating more.

Do I need to know how to code

No. You need to understand the product, not write the smart contract. Coding helps if you want to inspect deeper layers, but most users should focus on reading documentation, understanding risk, and using tools with clean interfaces and visible assumptions.

What’s the difference between APR and APY

APR is the simple annualized rate. APY includes the effect of compounding. In decentralized finance, that difference matters because some strategies auto-compound and others don’t. If a platform shows a number without explaining the mechanism, treat that as incomplete information.

Is DeFi really for everyone

Not yet. One of the biggest gaps in the space is access. Despite the rhetoric around inclusion, DeFi often fails to serve the unbanked because over-collateralization and other practical barriers keep entry difficult. Bruegel notes that simplified, low-collateral pathways on chains like Base are needed if broader participation is going to become real, as discussed in this Bruegel policy brief on decentralized finance.

That doesn’t make DeFi irrelevant. It means product design still has work to do. The systems that win long term will be the ones that reduce complexity without hiding risk.

Are DeFi earnings taxable

In many jurisdictions, they can be. The exact treatment depends on where you live and how the activity is classified. Keep records, track transfers and rewards, and get advice from a qualified tax professional if your activity becomes material.

What’s the best first move for a cautious user

Start with stablecoins, prioritize liquidity, and use straightforward strategies before trying anything exotic. You want your first experience in decentralized finance to teach you how the machine works, not how quickly complexity can compound.

If you want a simpler way to put stablecoins to work without manually tracking protocols all day, Yield Seeker offers an AI-guided path built around automated, risk-aware yield on USDC. It’s a practical fit for users who want hands-on visibility without doing every step by hand.