You probably know the feeling. You’ve got stablecoins sitting in an exchange account or a wallet, and they’re doing almost nothing. You keep hearing that defi can put those dollars to work, but every explanation seems to assume you already understand wallets, bridges, liquidity pools, and token approvals.

That gap is why many smart professionals stall out. The opportunity is real, but the path looks messier than it should.

Defi gets easier once you stop treating it like a pile of jargon and start treating it like a set of money tools on open rails. If your actual goal is earning yield on stablecoins without taking reckless risk, the path becomes much clearer. Some protocols are built for lending. Some pay you for providing liquidity. Some wrap those opportunities into automated vaults. And some tools now handle the monitoring and rebalancing that used to require living inside crypto dashboards.

What Is DeFi and Why Should You Care

At a practical level, defi is finance built on the internet without banks sitting in the middle of every action. Instead of asking a bank to hold deposits, move money, issue loans, or match buyers and sellers, you interact with software called smart contracts on a blockchain.

For a stablecoin holder, that matters because idle cash can become productive capital. Rather than waiting for a centralized platform to decide what yield to pass through, you can access lending markets, liquidity pools, and onchain strategies directly.

This isn’t a niche experiment anymore. DeFi reached $100.3 billion in Total Value Locked by February 25, 2025, and 17.49 million unique addresses had interacted with DeFi by January 2025, according to Statista’s DeFi market overview. TVL means the dollar value of assets deposited into defi protocols. It’s not a perfect metric, but it’s a good way to see whether capital is being deployed.

A simple way to think about it is this. Traditional finance is like renting access to a private office building. Defi is more like using public roads. The rules are visible, the infrastructure is shared, and anyone with the right vehicle can participate.

Defi is most useful when you stop asking, “What is this category called?” and start asking, “Who is paying for the yield, and what risk am I taking to earn it?”

That question filters out a lot of noise.

If you want a plain-English primer before going deeper, this explanation of what decentralized finance means is a useful companion. The important point is that defi isn’t one product. It’s a stack of protocols that let you save, lend, trade, hedge, and automate strategies in ways that were hard or impossible in older financial rails.

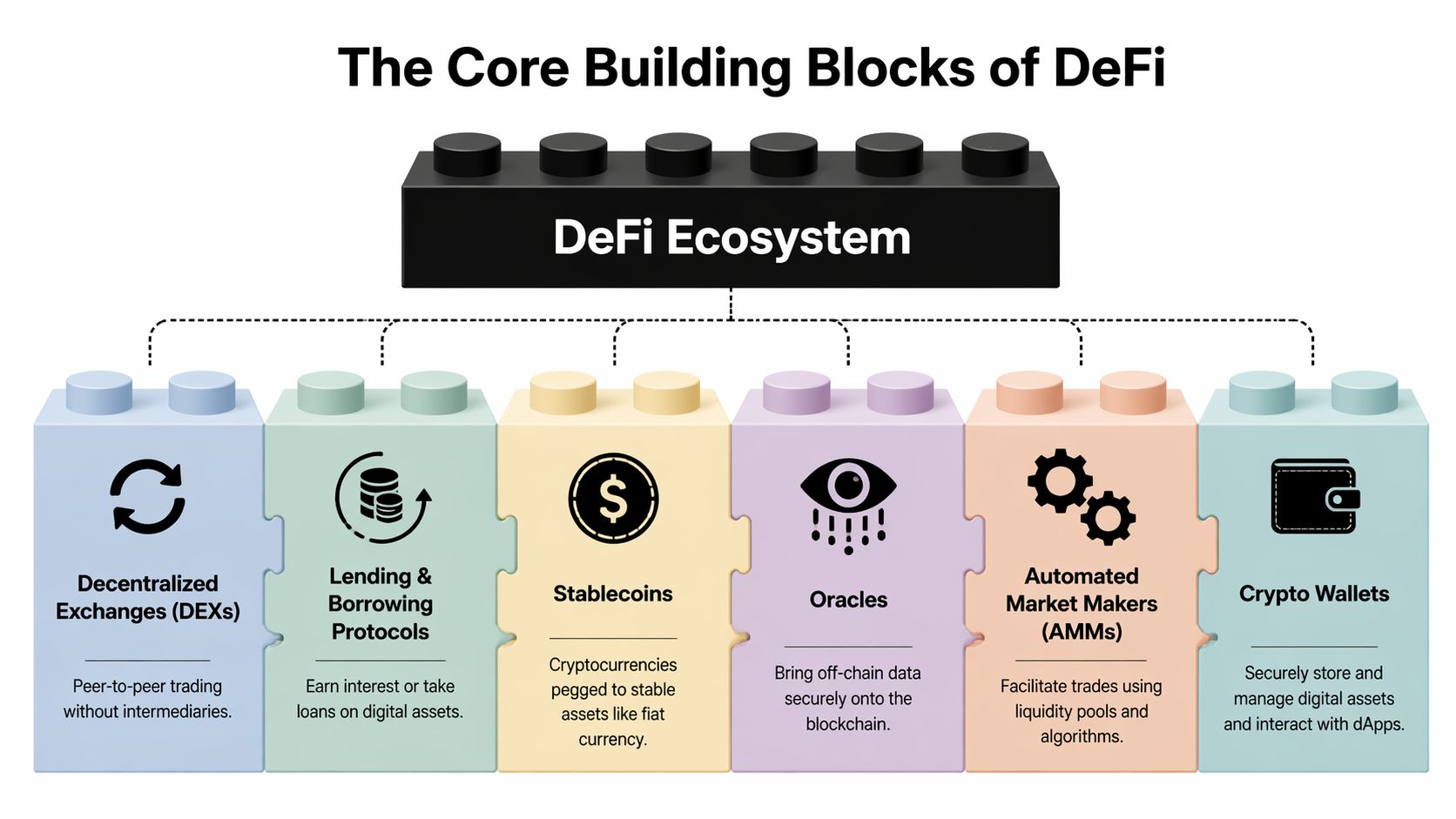

The Core Building Blocks of DeFi

Defi makes more sense when you see it as a set of financial Lego blocks. Each block does one job. The interesting part is how they snap together.

Stablecoins as the base layer

Stablecoins are the flat baseplate. They’re the part that lets the rest of the structure stand up without wobbling every time the crypto market moves.

When you hold USDC, DAI, or another dollar-pegged asset, you’re holding something designed to stay relatively stable in price. That stability is what makes yield strategies legible. If the asset itself is swinging hard, it becomes difficult to tell whether you earned yield or just rode volatility.

For those entering defi to earn passive income, stablecoins are the cleanest starting point because they reduce one major variable.

Wallets as your operating system

Your wallet is not just storage. It’s your account, signature tool, and permission layer.

MetaMask, Rabby, Coinbase Wallet, and hardware wallets all play this role in slightly different ways. In practical terms, the wallet decides how you connect to protocols, approve transactions, and protect keys. If the wallet is sloppy, the rest of your strategy doesn’t matter much.

A good mental model is to treat your wallet like the combination of your bank login, your card, and your legal signature. That’s why experienced users care so much about wallet hygiene.

DEXs and AMMs as automated exchange booths

A decentralized exchange, or DEX, lets users trade without a traditional intermediary. Uniswap is the standard example. Instead of a company matching orders in an order book, smart contracts use liquidity pools.

An automated market maker, or AMM, is the engine inside that system. It is akin to a 24/7 currency booth with an algorithmic pricing rule. Traders come in to swap one asset for another. Liquidity providers stock the booth and earn fees when people use it.

One of DeFi’s most important mechanics involves platforms like Uniswap, where higher TVL reduces slippage, which attracts more trading volume and fees, which then attracts more liquidity providers. Bitwise describes this as a liquidity flywheel and notes that protocols maintaining more than $100M in a specific pool through market cycles tend to demonstrate resilience in a way users should pay attention to, as explained in Bitwise’s framework for evaluating DeFi assets.

That’s not just theory. In practice, deeper pools are easier to trust for stablecoin strategies because they usually offer cleaner exits and less pricing friction.

Lending protocols as automated pawn shops

Aave, Compound, and similar markets work like automated pawn shops, except you can participate from either side.

Borrowers deposit collateral and take out loans. Suppliers deposit assets into shared pools and earn yield from borrower demand. The contracts handle pricing, collateral thresholds, and liquidations automatically.

If you’re a stablecoin holder, this is often the simplest first yield source to understand. You supply USDC or DAI. Borrowers pay to access that liquidity. A portion of that payment flows back to suppliers.

Oracles as data wires

Smart contracts can’t magically know offchain prices. They need data feeds.

That’s what oracles do. Services like Chainlink bring market prices and other external data onchain so protocols can decide whether collateral is sufficient, whether a loan should be liquidated, or whether a vault should rebalance.

Without reliable oracles, lending and trading systems would be flying blind. In builder terms, oracles are less exciting than trading interfaces, but they are part of the plumbing that keeps the machine from breaking.

Liquid staking as a receipt you can still use

Liquid staking confuses people because it sounds more exotic than it is. The easiest analogy is a coat check.

You hand over an asset to be staked. In return, you receive a receipt token that represents your claim on that staked position. Unlike a paper coat check ticket, this receipt can often be used elsewhere in defi.

That matters because one of the old trade-offs in crypto was simple. You could stake an asset for yield, or you could keep it liquid and useful. Liquid staking tries to soften that trade-off by giving you both exposure to staking rewards and a tradable onchain representation of the position.

Why composability matters

Defi's power is that these blocks interlock. A wallet connects you to a lending market. A stablecoin serves as the capital base. An oracle supports risk management. A DEX provides swaps and exits. An AMM turns capital into fee-generating liquidity.

Practical rule: Don’t judge a protocol by headline yield first. Judge the blocks underneath it. What asset are you depositing, what contract holds it, what data feed informs the risk model, and where does the cash flow actually come from?

That single habit will save you from a lot of bad decisions.

How DeFi Generates Stablecoin Yield

Stablecoin yield in defi usually comes from three places. Someone pays to borrow your capital. Traders pay fees to use your liquidity. Or a protocol distributes incentives to attract deposits and activity.

Lending income

The cleanest yield source is lending. You deposit stablecoins into a lending pool on a protocol like Aave. Borrowers draw from that pool and pay interest.

Why do borrowers want stablecoins so badly? In defi, lending is dominated by overcollateralized loans because borrower anonymity removes traditional credit checks. That means borrowers often post collateral worth more than the loan they take, often using volatile crypto assets to borrow stablecoins to amplify their financial positions. The BIS explains that this is a primary driver of stablecoin lending demand in its analysis of overcollateralized DeFi lending.

That dynamic is important. The yield isn’t free money. It exists because traders, arbitrageurs, and borrowers seeking to magnify returns value stable, borrowable dollars enough to pay for them.

Trading fees from liquidity provision

The second source is liquidity provision. You deposit assets into an AMM pool, and traders pay fees when they swap through it.

With stablecoin pairs, this can be attractive because the assets are designed to stay close in value. That usually makes the ride smoother than pairing a stablecoin with something volatile. But “smoother” doesn’t mean risk-free. If one asset in the pool moves away from the other, your pool position can underperform compared to holding the tokens outright. That’s impermanent loss.

A useful way to think about it is inventory drift. You stocked a two-currency kiosk. As traders hit the pool, the mix of inventory changes. If prices move enough, the mix you end up holding may be worse than what you started with.

If you want a clearer feel for the mechanics behind pool depth and borrow demand, this piece on understanding stablecoin liquidity gives practical context around how liquidity can tighten and why that matters.

Incentives and yield farming

The third source is incentives. Protocols often distribute their own tokens or direct rewards to attract deposits, bootstrap activity, or deepen liquidity in target pools.

Many new users get misled. Incentive yield can be real, but it’s also the most likely to fade, get repriced, or disappear once a protocol changes strategy. A pool paying attractive rewards today can look average very quickly if emissions fall or token prices weaken.

Good yield has an economic reason. Promotional yield has a marketing budget.

That distinction matters more than any dashboard color coding.

For a deeper walkthrough focused specifically on this goal, this guide to earning yield on stablecoins is worth reading alongside your own protocol research.

A short explainer can also help if you prefer a visual overview before trying anything hands-on:

Navigating the DeFi Risk Landscape

Yield only makes sense when paired with a risk model. In defi, the mistake isn’t usually “I didn’t know there was risk.” The mistake is lumping every risk into one blurry category and then reacting too late.

A useful way to think about it is to separate technical risk, market risk, and external risk. Each behaves differently, and each needs a different response.

Technical risk

Technical risk lives in the code and system design. Smart contracts can contain bugs. Upgrade mechanisms can be abused. Governance settings can be misconfigured. Oracles can fail in edge cases.

The ugly truth is that code can be transparent and still be dangerous. “Code is law” sounds reassuring until the law contains a loophole.

The evidence here is not abstract. Protocols with high safety scores above 90/100 from services like DeFiSafety have a 70% lower incidence of exploits, and inadequate audits have contributed to more than $3 billion in annual losses, with 80% of recent exploits tied to smart contract bugs or governance misconfigurations, according to this review of DeFi audit and security tools.

Market risk

Market risk is what happens even when the code works exactly as designed.

Liquidity can dry up. Borrow rates can swing. Stablecoin pegs can wobble. A liquidity provider can earn fees for weeks, then give much of it back because the pool composition changed during a dislocation. That’s why “I used a blue-chip protocol” isn’t the same as “my position was safe.”

Impermanent loss belongs in this category. So does liquidation risk if you borrow against collateral. In practice, many painful losses in defi come not from hacks but from users underestimating how quickly market structure can shift.

External risk

External risk sits outside the protocol but still affects your outcome. Stablecoin issuers can face operational or regulatory pressure. Front-end websites can geo-block users. Tax treatment can be unclear or change over time.

This part is less glamorous than discussing AMM curves, but it affects real returns. If you’re active in a jurisdiction with complex reporting rules, you need to account for that before scaling activity. For example, anyone dealing with local reporting obligations may want a practical overview of Australian crypto tax regulations to understand how frequent swaps, rewards, and disposals can create admin overhead.

The safest-looking defi position can still become a bad position if the surrounding legal, issuer, or access assumptions change.

DeFi risk taxonomy

Risk Category | Risk Type | What It Means | How to Mitigate |

|---|---|---|---|

Technical | Smart contract bug | A flaw in the contract can let attackers drain or freeze funds | Use mature protocols with current audits, simpler designs, and visible documentation |

Technical | Governance misconfiguration | Admin controls or upgrade paths can be used badly or maliciously | Check who controls upgrades, pause functions, and treasury permissions |

Technical | Oracle failure | Bad pricing data can trigger wrong liquidations or broken accounting | Prefer protocols using established oracle infrastructure and conservative parameters |

Market | Impermanent loss | LP positions can underperform holding assets directly when prices diverge | Favor stablecoin pairs if your goal is lower volatility and understand pool behavior first |

Market | Liquidity risk | Exiting a position can become costly or slow during stress | Look for deeper pools and avoid thin markets for core capital |

Market | Peg risk | A stablecoin may trade away from its intended value | Diversify stablecoin exposure and understand issuer design |

External | Issuer risk | Offchain reserve, banking, or operational issues can affect redemption confidence | Spread exposure across stablecoin types where appropriate |

External | Regulatory risk | Rules can alter access, disclosure, or tax treatment | Keep records and understand your local obligations before activity increases |

External | Interface risk | A fake front end or bad approval flow can compromise funds | Bookmark official apps, verify links, and review approvals carefully |

Practical DeFi Safety Best Practices

The safest users in defi usually aren’t the smartest traders. They’re the people with repeatable habits.

Start with boring protocol checks

Before depositing anything, answer a few plain questions.

What does the protocol do: If you can’t explain the cash flow in one sentence, skip it.

How mature is the market: Look at TVL, pool depth, and whether users can exit without drama.

Who has touched the code: Read public audits, not just the protocol homepage summary.

How does it fail: Every design has a failure mode. You want to know it before deposit, not after.

A lot of beginners say they’re doing research when they’re really comparing APY screenshots. Real research is slower and less exciting.

Use position sizing as a security tool

Most avoidable damage comes from sizing too big too early. Start with an amount small enough that a mistake becomes tuition, not a crisis.

That applies even if you’re technically experienced. A new chain, a new wallet flow, or a new approval pattern introduces operational risk. Running a tiny test deposit first is not hesitation. It’s process discipline.

Field note: A small live transaction teaches more than an hour of reading. It forces you to check gas, approvals, settlement, and withdrawal paths.

Clean up wallet risk

Wallet security is where many otherwise careful users get sloppy.

Use a dedicated wallet: Keep long-term holdings separate from your everyday defi wallet.

Prefer hardware signing for meaningful balances: It adds friction, which is exactly why it helps.

Revoke old token approvals: Unlimited approvals accumulate and widen the blast radius if something goes wrong.

Bookmark protocol URLs: Don’t trust search results when money is on the line.

Diversify by mechanism, not just by logo

Holding stablecoins across three protocols that all depend on the same type of yield driver is less diversified than it looks.

A better approach is to spread exposure across different mechanisms. One lending position, one highly liquid stable pool, maybe one conservative automated vault if you understand how it allocates. That way you’re not just diversifying brands. You’re diversifying sources of return and sources of failure.

Know your exit before your entry

Before you deposit, check how withdrawals work, what conditions can slow exits, and what would make you rotate elsewhere.

This sounds basic, but many people only study entry screens. In defi, the quality of your exit path matters as much as the yield path.

The AI Advantage for Automating DeFi Yield

Manual defi works. It also demands constant attention.

Rates change. Pool composition changes. Borrow demand moves. New risks appear in governance forums, audit updates, and market dislocations before they show up in a glossy dashboard. That’s manageable if defi is your full-time job. It’s much harder if you’re a professional with a calendar, a family, and a portfolio that needs maintenance rather than obsession.

Where manual workflows break down

The first problem is fragmentation. You might check a lending market in one tab, a DEX analytics page in another, a wallet view in a third, and a risk discussion somewhere else entirely.

The second problem is reaction time. A stablecoin strategy often looks conservative, but small changes compound. If liquidity thins, incentives fade, or a safer venue becomes available, the edge goes to whoever notices and acts first.

The third problem is consistency. Many users know what they should do. Fewer do it every week.

What AI is actually useful for

AI in defi is most useful when it handles repetitive judgment, not when it pretends to predict the future. The practical jobs are straightforward:

Monitoring opportunities: Scanning protocols and rates continuously is tedious but valuable.

Applying filters: Excluding venues that fail your liquidity, audit, or risk standards.

Rebalancing capital: Moving funds when the risk-reward profile changes.

Reducing interface burden: Presenting a clearer decision layer than juggling raw dashboards.

If you’ve used a personal operations tool like a finance tracker agent, the conceptual leap isn’t large. The same logic applies here. Software can watch more inputs than most humans can watch consistently.

Where an AI layer fits for stablecoin holders

A platform like Yield Seeker’s AI yield optimization workflow fits this niche because it’s built around stablecoin allocation rather than generalized crypto speculation. The model is simple: deposit USDC on Base, let an AI agent monitor protocol conditions, and let it allocate or rebalance across defi opportunities based on yield and risk inputs.

That kind of setup doesn’t remove risk. Nothing does. What it can remove is a lot of low-value manual labor that causes users to miss opportunities, neglect approvals, or leave capital sitting in weak positions because they haven’t checked dashboards lately.

Automation is helpful when the rules are clear. In stablecoin defi, the useful question isn’t “Can AI beat the market?” It’s “Can software follow my yield and risk rules more consistently than I will?”

For many users, the answer is yes.

Your First Steps into Decentralized Finance

The best way to start with defi is to make the first move deliberately small. You are not trying to maximize return on day one. You are trying to build operational fluency without making expensive mistakes.

DeFi has already shown that it can survive hype, crashes, and rebuild cycles. From its roots in Bitcoin in 2009 and Ethereum’s smart contracts in 2015, the sector expanded rapidly, saw TVL peak near $180 billion, then recovered after the 2022 crash, with monthly users growing to over 17 million by early 2025, as summarized in Wikipedia’s history of decentralized finance. The point for a new user is simple. This space is not finished, but it is persistent.

Learn with a wallet and a tiny amount

Set up a self-custody wallet. Fund it with a small amount of stablecoins and enough native gas token for transactions on the chain you plan to use.

Keep the amount small enough that you can focus on the mechanics. Learn how signing works. Learn how a token approval differs from a swap. Learn what a transaction explorer shows when something is pending.

Explore one action at a time

Don’t stack complexity. Do one thing, then reverse it.

Try a small swap on a major DEX. Then try supplying a small amount of stablecoins to a lending protocol. Then withdraw. That round trip matters because it teaches you entry, monitoring, and exit in one loop.

A simple progression works well:

Open the wallet and confirm balances

Make one small swap

Supply stablecoins to one established protocol

Wait, observe, then withdraw

Review what felt confusing before increasing size

Automate only after you understand the basics

Automation works best when you know what the machine is doing on your behalf. Once you understand lending, liquidity, and approvals at a basic level, handing monitoring and rebalancing to software becomes much more sensible.

That’s where many busy stablecoin holders land. They don’t want to become full-time defi operators. They want exposure to onchain yield with clearer guardrails and less dashboard sprawl.

The long-term direction is easy to see. More finance will move onchain, and more of the user experience will be abstracted away from raw protocol interaction. The winners won’t be the people who memorize every dashboard. They’ll be the ones who understand the incentives, respect the risks, and use better tools to stay disciplined.

If you want a lower-friction way to put stablecoins to work, Yield Seeker offers an AI-powered approach to monitoring and allocating USDC on Base. You can start small, keep funds accessible, and use the platform as a practical bridge between learning defi and managing stablecoin yield more consistently.