Your money may already be doing one job well. It covers bills, subscriptions, groceries, and maybe a little left over. The problem is what happens after that. Cash sits idle. Stablecoins sit in a wallet. Savings earn something, but often not enough to feel meaningful.

That gap is why so many people start looking for side income. In 2025, 37% of US workers currently have a side hustle and another 35% are actively considering one, meaning 72% either already have or are considering a side hustle, yet the median side hustle income is only $200 per month according to SurveyMonkey’s side hustle statistics. A lot of people are not lazy. They are just stuck trading more time for modest results.

A better question is how to make money work for you without turning your life into a second shift. That is where automated yield, especially on stablecoins, becomes interesting. It is not magic and it is not risk-free. But it does offer a practical middle path between idle cash and high-volatility speculation.

Beyond the Paycheck Your New Mindset for Building Wealth

You get paid on Friday, cover your bills, and leave the rest in checking, savings, or a wallet. A month later, that cash is still sitting there. The missed opportunity is not earning too little. It is leaving capital without a job.

They save. They earn. Some already hold USDC or another stablecoin. The sticking point is usually the handoff between "I have money available" and "I know where to put it without creating more work for myself."

Idle money is a choice

Money that stays idle still reflects a decision. Cash in a low-yield account trades return for convenience. Stablecoins parked in a wallet trade optionality for zero productivity. Both can be reasonable for money you may need soon. Both are expensive habits if they become the default for every extra dollar.

A better operating rule is simple: give every dollar a role.

Some dollars cover near-term expenses. Some protect you from surprises. If you have not built that buffer yet, start with how to build an emergency fund. The rest can be assigned to compounding.

Why older wealth advice leaves a gap

Traditional options still have a place. Savings accounts are simple. Dividend stocks can fit a long-term portfolio. Real estate can produce income, but it also adds paperwork, concentration risk, and a much higher capital threshold.

That leaves a gap for beginners and busy professionals. They want passive income without managing tenants, researching individual stocks every weekend, or adding another part-time job. They also may not have $5,000 or $50,000 ready to deploy. They may have $10, $100, or a few hundred dollars in stablecoins already sitting onchain.

That is where DeFi stablecoin yield stands out. It lowers the minimum to get started, keeps the process digital, and gives people a way to put small amounts of capital to work without turning investing into a second occupation.

AI makes DeFi usable for normal schedules

The hard part of DeFi is rarely the first deposit. The hard part is the maintenance. Rates change. Protocol risk changes. Incentives come and go. Manual yield farming asks for constant attention, and many individuals will not keep up with that for long.

AI changes the experience by handling the repetitive decisions that usually scare off beginners and drain experienced users. It can track pools, compare net yield, apply preset risk limits, and reallocate stablecoins without you checking five dashboards every day.

I have seen this shift firsthand while building and using systems like Yield Seeker. A key benefit is not that automation creates risk-free returns. It does not. The benefit is that it makes a disciplined process easier to follow. That matters because good yield decisions often fail for ordinary reasons. People get busy, miss a better allocation, or leave funds idle because reviewing protocols feels like homework.

The modern blueprint is to separate reserve cash from investable capital, choose a risk level you can live with, and use automation to keep that capital productive. That approach is a better fit for people who want passive income from digital dollars without adding more labor to the week.

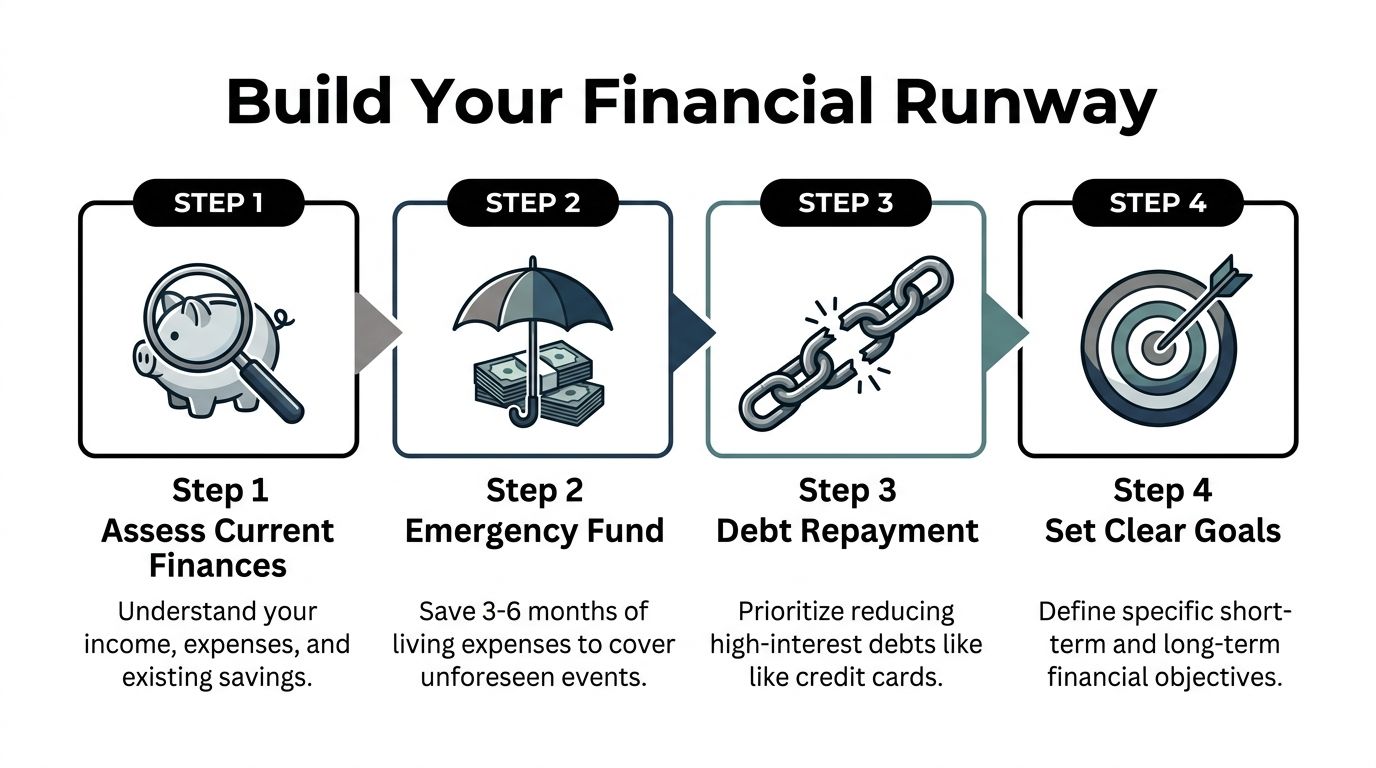

Build Your Financial Runway Before Taking Off

A lot of people decide to "start investing" right after payday, move money into a yield strategy, and then pull it back out two weeks later to cover rent, taxes, or a credit card bill. I have seen that pattern repeatedly. The problem starts in cash planning.

Start with the cash picture you have

Open a spreadsheet or budgeting app and list four things: after-tax income, fixed bills, variable spending, and current cash reserves. Add debt payments too. Do not optimize anything yet. Get a clean view of what is already happening.

This exercise usually exposes the underlying constraint fast. Sometimes there is investable cash sitting idle in checking or savings. Sometimes recurring spending is absorbing far more than expected. Sometimes the answer is simpler. There is no room to deploy capital yet, and the right move is to stabilize first.

That matters because passive income should reduce pressure, not add it. If you are deciding between another time-intensive side hustle and a low-friction way to put digital dollars to work, start by measuring what cash is already available. For readers considering stablecoins, this primer on stablecoin investing strategies for beginners helps frame what belongs in a yield strategy and what should stay liquid.

Separate emergency money from earning money

Emergency cash and investment capital do different jobs. Keep them separate.

When people combine the two, every withdrawal becomes emotional. A car repair or medical bill suddenly forces a decision about whether to unwind a position early. That is avoidable.

If you need a practical framework, this guide on how to build an emergency fund is a useful companion. Keep emergency cash accessible and boring. Put only the money with a real time horizon into yield.

Rule worth following: Emergency money handles disruption. Investment money stays deployed long enough to compound.

Remove expensive drag first

High-interest debt can erase the benefit of chasing yield. Credit card balances are the usual problem, but any expensive debt deserves a direct comparison.

I do not treat this as an all-or-nothing rule. You do not need to clear every balance before investing a dollar. You do need to look at the math carefully. If debt is compounding faster than your likely return, paying it down may be the better use of cash right now.

A workable order looks like this:

Cover fixed living costs and minimum payments.

Build a separate cash buffer so you do not need panic withdrawals.

Pay down the highest-cost debt that is slowing progress.

Deploy only the capital that can stay invested.

Define the purpose of the capital

Money without a job usually gets misused.

Write down what each pool of capital is for before you deposit anything. Near-term spending needs stability and access. Medium-term reserves need predictability. Long-term capital can pursue compounding with more patience.

Goal type | Time horizon | What matters most |

|---|---|---|

Near-term spending | Short horizon | Stability and access |

Medium-term reserve | Moderate horizon | Predictability |

Long-term wealth building | Long horizon | Compounding and disciplined allocation |

I have found that this step prevents bad decisions later. People react less when markets or rates change if they already know the role of the money.

Automate the prep before you automate yield

Automation should start before the first investment.

Set recurring transfers into your emergency reserve. Schedule a fixed transfer into the account you use for investable capital. Remove monthly decision fatigue from the process. A simple system beats good intentions that depend on motivation.

This is the part beginners often skip because it feels too basic. In practice, it is what makes low-maintenance income possible later, especially for busy professionals starting with small deposits instead of large portfolios.

Mapping Your Options from Savings Accounts to Stablecoin Yield

Not all passive income tools solve the same problem.

Some are built for liquidity. Some are built for long-term growth. Some need more capital, more patience, or more tolerance for price swings than people expect. If you want to understand how to make money work for you, compare the options by function, not by hype.

The traditional menu still has a place

The usual starting points are familiar for a reason.

A high-yield savings account is simple. It keeps cash available and usually beats a standard savings account. A money market account plays a similar role. These options are useful when capital must stay stable and accessible.

A broad stock market index fund is different. It is a long-term growth tool. According to Stash’s guide on making your money work for you, the average stock market return is approximately 10% per year. That matters because it shows why long-term investing remains one of the strongest wealth-building tools. It also comes with volatility, which means timing and temperament matter.

Real estate sits in another category. It can produce income and appreciation, but it usually demands more capital, more operational work, or both.

Compare the trade-offs directly

Here is the practical lens I use:

Option | Main advantage | Main drawback | Best fit |

|---|---|---|---|

High-yield savings or money market | Stability and accessibility | Lower upside | Emergency reserves and short-term cash |

Stock market investing | Strong long-term growth potential | Price volatility | Long-term wealth building |

Rental property or REIT exposure | Income potential | Complexity or market sensitivity | Investors comfortable with property or market cycles |

Stablecoin yield in DeFi | Yield without direct equity-style volatility | Smart contract and protocol risk | Users who want productive stablecoin exposure |

That last row is where many people pause, because it feels unfamiliar even when the mechanics are not that complicated.

Why stablecoin yield stands out

Stablecoin yield occupies a middle space that a lot of guides skip. You are not relying on a bank savings rate. You are not taking direct exposure to stock market price swings. You are using dollar-pegged digital assets in on-chain financial systems that generate yield through lending, liquidity provision, and other protocol activity.

That does not make it risk-free. It makes it a different risk profile.

For beginners, the key appeal is often this combination:

The asset itself is designed for price stability: You avoid the direct volatility associated with many crypto tokens.

The capital can remain liquid: You are not always locking funds for long periods.

The strategy can be automated: This matters more than many realize.

If you want a deeper primer on the category, this overview of https://yieldseeker.xyz/blog/stablecoin-investing is a useful place to understand how stablecoin strategies are typically structured.

What works: Using stablecoin yield for capital you want productive, but not exposed to equity-style swings. What fails: Treating stablecoin yield as if it has zero technical risk.

Where people go wrong when choosing

The common mistake is picking an option because the headline return sounds attractive, not because it fits the job.

Someone with near-term cash needs should usually prioritize access and stability. Someone with a very long horizon can afford more variability. Someone who already keeps part of their net worth in stablecoins may benefit from putting that capital to work instead of leaving it idle.

The strongest portfolio usually mixes tools. Savings for security. Long-term market exposure for growth. Stablecoin yield for productive digital cash management. The point is not to choose one religion. It is to assign each pool of capital to the right environment.

Activate Your AI Agent and Start Earning Effortlessly

Manual DeFi yield hunting looks easy from the outside. In practice, it becomes a part-time job fast.

You check rates. You compare protocols. You move funds. You wonder whether the new yield is worth the gas, the risk, or the time. Then rates change again. Many users do not need more dashboards. They need a workflow that handles the repetitive parts.

Why automation matters more in DeFi

Automation is not a convenience feature in this category. It is a practical edge.

According to Rosamond Financial Group’s write-up on automation and wealth building, automation can improve long-term portfolio performance by 2-4% annually compared to manual strategies. The same source notes that in DeFi, AI-driven reallocation can capture an additional 1-3% in annualized returns by switching protocols dynamically as conditions change.

That lines up with what I have seen building in this space. Rates move. Opportunities fragment. Manual management tends to lag because real people have jobs, sleep, and limited attention.

A simple setup flow

The cleanest way to start is to treat this like onboarding any financial tool. Keep the first deposit small, confirm the experience makes sense, then scale gradually if it fits your plan.

Here is the process I recommend:

Create an account

Use a platform with a straightforward dashboard, visible balances, and clear earning history. If the interface feels confusing on day one, it will not feel better when real money is moving.

Connect your wallet

This is the bridge between your assets and the protocol layer. Take your time. Verify the site, wallet prompts, and network before approving anything.

Fund with stablecoins on the supported network

For a platform like Yield Seeker, the setup starts with USDC on Base and supports deposits as small as $10, which lowers the barrier for testing the workflow before committing larger capital.

Choose your allocation profile

Your allocation profile is the point where automation should reflect your goals, not your mood. Shorter-term capital needs a more stable posture. Longer-term capital can tolerate more variability.

Let the AI agent manage the repetitive work

The agent monitors available opportunities, allocates based on your profile, and handles the constant scanning most users do not want to do themselves.

I like this explainer for readers who want the concept in plain terms: https://yieldseeker.xyz/blog/how-to-use-ai-agents

What the AI is doing

A good AI-driven yield workflow is not “guessing the market.” It is applying rules and reacting to available data faster than a person reasonably can.

That usually includes:

Monitoring protocol conditions: Rates, available pools, and changes in the yield environment.

Allocating capital within set constraints: Not just chasing the highest number on a screen.

Rebalancing when conditions change: Without requiring you to monitor every move.

Maintaining liquidity: So you are not trapped if your situation changes.

This is the point most beginners miss. The value is not only the yield itself. The value is removing the friction that keeps capital idle.

A look at the workflow in motion

Seeing the interface usually makes the process click faster than reading another paragraph.

What works and what does not

Some habits improve outcomes immediately.

Start small: Use the minimum practical deposit first. Learn the rhythm of deposits, earnings, and withdrawals.

Keep your goals attached to the capital: Do not use short-term money for a longer strategy just because yields look attractive.

Review the dashboard, not every headline: Obsessing over every market post usually leads to bad overrides.

Other habits cause trouble:

Jumping between protocols manually: This burns time and often adds unnecessary error risk.

Depositing money you may need next week: Liquidity helps, but planning still matters.

Treating stablecoin yield like a savings account clone: The mechanics and risks are different.

Builder’s view: The biggest shift for beginners is realizing they do not need to become protocol researchers. They need a setup that applies risk rules consistently and gives them visibility without requiring constant attention.

If you have ever left stablecoins untouched because DeFi felt too fragmented, the process becomes practical. The setup is short. The difficult part is mostly psychological: trusting a structured system more than random manual tinkering.

How to Monitor Performance and Manage Your Risk

Automation is useful only if you can inspect it.

Too many people assume passive means invisible. In DeFi, that is the wrong mindset. You want less manual work, but you still need clear oversight. The best setups reduce labor while preserving visibility.

Watch the right signals

A good monitoring routine is light, not obsessive.

Look for a dashboard that shows your current balance, earnings, recent allocation activity, and withdrawal availability in one place. If you need to bounce between several apps to understand what is happening, the setup is too fragmented for most busy users.

For people who want a clearer view into how these systems are tracked, https://yieldseeker.xyz/blog/real-time-yield-monitoring gives a useful look at what real-time monitoring should surface.

Match strategy to when you need the money

This is the part many investors skip, and it causes most of the regret later.

As True Root Financial explains, capital needed within 3-5 years should generally favor more stable, lower-yield strategies in the 4-6% range, while long-term capital over 20+ years can pursue higher-yield strategies in the 8-12%+ range. The same source warns that chasing high yields with short-term money is a common mistake.

That principle matters in DeFi because high visible yield can tempt people into misusing capital. Automation helps only when the strategy is aligned to the purpose of the money in the first place.

Use the terminal as an educational tool

One feature I think more platforms should include is a built-in terminal or activity view that shows what the agent is doing and why.

This matters for two reasons:

It builds trust through visibility: You can see that allocation changes are tied to real conditions, not mystery behavior.

It helps you learn gradually: You do not need to read every protocol doc on day one.

That learning loop is valuable. It turns automation from a black box into a guided environment. For beginners, that can be the difference between using DeFi once and using it responsibly for years.

Good oversight is simple: Check that balances make sense, earnings are updating, and liquidity remains available. You do not need to micromanage every move.

Practical risk controls that matter

There is no version of DeFi without risk. What matters is how you handle it.

I recommend a short checklist:

Start with a limited allocation: Use a portion of capital, not everything at once.

Keep emergency funds separate: Those dollars should not depend on protocol performance.

Favor liquidity: If funds are accessible without lockup, your planning becomes easier.

Know the technical risk exists: Smart contract risk is real even when the experience feels smooth.

Avoid yield chasing: A higher number is not automatically a better fit.

A lot of monitoring anxiety comes from using the wrong frame. People ask, “Is this perfectly safe?” That is not the right test. Ask instead, “Does this level of risk fit the role of this capital, and can I observe what is happening clearly enough to stay in control?”

That question leads to better decisions.

Long-Term Strategies for Security and Taxes

The people who last in DeFi are rarely the ones chasing every new opportunity. They are the ones who protect access, keep records, and think in years instead of weekends.

Security comes first because yield does not matter if your wallet hygiene is weak. Use strong wallet practices. Be skeptical of every signature request. Double-check URLs. If your balance grows, consider moving primary holdings behind a hardware wallet setup and using a separate wallet for experimentation.

Security habits worth keeping

You do not need a complicated system. You need disciplined repetition.

Verify every connection: Bookmark the platforms you use and avoid clicking random links from social feeds or group chats.

Separate roles by wallet: One wallet for long-term holdings, another for active interaction can reduce blast radius.

Review approvals periodically: Old permissions are easy to forget and worth cleaning up.

Long-term edge: In DeFi, operational discipline often matters as much as strategy selection.

Taxes are part of the strategy

A lot of people treat taxes as something to figure out later. That usually creates stress right when records are hardest to reconstruct.

Track deposits, withdrawals, and yield earnings as they happen. Keep exports, screenshots, or transaction logs in one place. The exact treatment varies by jurisdiction, so broad internet advice is rarely enough once real money is involved.

If you need professional help sorting reporting obligations, this directory to Hire Tax Accountants can help you find a specialist. The right accountant will usually save you more time and confusion than any last-minute spreadsheet scramble.

Keep the long view

A key advantage in learning how to make money work for you is not one high month. It is building a repeatable system.

Good systems usually share the same traits. Capital is allocated intentionally. Security habits are boring and consistent. Taxes are documented early. Strategy changes happen for a reason, not because a timeline post triggered fear or greed.

That is how passive income becomes durable instead of distracting.

Frequently Asked Questions

What smart contract risks are involved

Smart contract risk means code can fail, behave unexpectedly, or expose funds to loss if a protocol has a vulnerability. Automation can reduce the burden of monitoring and selecting opportunities, but it does not erase technical risk. A sensible approach is to start with a small allocation, keep emergency cash separate, and use platforms that make activity visible rather than opaque.

Can I use stablecoins other than USDC

Support depends on the specific platform and network. In the workflow discussed above, the standard setup uses USDC on Base. If you hold a different stablecoin, check whether the platform supports direct deposits or whether you need to convert first.

How is the yield generated

Stablecoin yield in DeFi typically comes from protocol activity such as lending and liquidity deployment. The user supplies stablecoins, and the platform or strategy layer allocates that capital across eligible on-chain opportunities based on its rules and risk posture.

Are there lockups or withdrawal fees

That depends on the product design. Some platforms impose restrictions, while others keep funds accessible. In the Yield Seeker model described here, funds remain accessible with no lockups or withdrawal fees.

Do I need a large starting balance

No. One reason automated stablecoin strategies are attractive is that they can be tested with small amounts. In the setup described in this article, deposits can start at $10, which makes it easier to learn the workflow before scaling up.

If you want a low-friction way to put idle stablecoins to work, Yield Seeker is built for that workflow. You create an account, deposit USDC on Base, and let an AI agent monitor and allocate capital across DeFi opportunities while keeping funds accessible. It is a practical option for beginners who want guidance and for busy users who do not want to manage yield manually.