You deposit into a liquidity pool because the APY looks attractive. A few days later, the position is up on fees, but your total value is still lower than if you had kept the tokens in your wallet. That gap feels wrong the first time you see it.

That gap is impermanent loss.

Most explanations stop at the volatile-token version of the story. They use ETH paired with a dollar stablecoin, show a dramatic price move, and leave readers with the impression that providing liquidity always means taking a major hidden hit. That is incomplete. For a large share of DeFi users, especially stablecoin holders, impermanent loss explained properly looks very different.

A key question is not “Does impermanent loss exist?” It does. The useful question is “How much does it matter for the pool I am using, and what can I do about it?”

The Hidden Cost of Providing Liquidity

A new LP usually notices impermanent loss backward. Not from a formula. From a disappointing withdrawal screen.

You add two assets to a DEX pool, watch fees accumulate, and assume you are getting paid to sit there. Then one asset moves hard, you check your position, and the composition has changed. You hold less of the asset that ran up and more of the one that lagged.

That is the hidden cost. The pool kept making a market with your assets.

Why smart users still get caught by it

The trap is not ignorance. It is intuition.

Many individuals think, “I deposited both assets, so I should still own the same basic mix, plus fees.” In an AMM, that is not how it works. Your assets are continuously rebalanced as traders interact with the pool.

If you have ever worked with teams building exchanges or market infrastructure, this becomes obvious quickly. A good DEX development company can show how pool mechanics, fee tiers, and liquidity design change provider outcomes long before users see it in their wallet balance.

You are not just parking assets in a pool. You are letting an automated system trade them for you.

What makes this frustrating

Impermanent loss does not always mean your position is down in absolute terms. It means your position can underperform a simple hold strategy.

That distinction matters in practice:

You may still earn fees: A position can produce income and still lag holding.

The pain shows up at withdrawal: While funds stay in the pool, the loss is unrealized.

Busy investors often misdiagnose it: They blame the protocol, the interface, or gas costs when the core issue is pair selection.

For stablecoin-focused users, the conversation shifts here. If your goal is earning yield on idle dollars rather than expressing a directional market view, the relevant question is not how bad impermanent loss can get in theory. It is whether your chosen pool structure makes that risk meaningful at all.

What Is Impermanent Loss Really

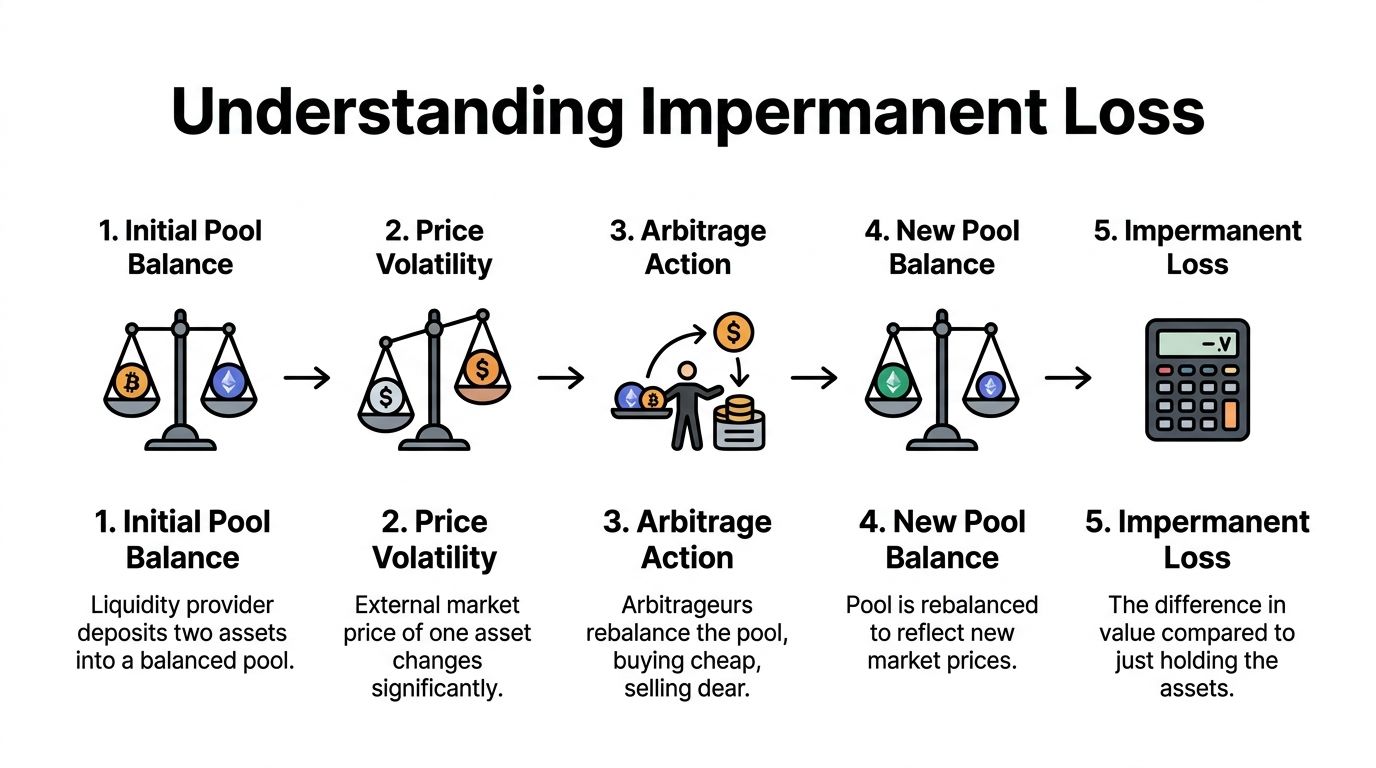

Impermanent loss is the gap between two outcomes: keeping your original assets in your wallet, or depositing them into an AMM that keeps rebalancing them as price changes.

That gap exists because the pool is always selling some of the asset that is getting stronger and buying more of the one that is getting weaker. For a directional trader, that can be painful. For a stablecoin LP, it is often a much smaller issue because the two assets are designed to stay close in price.

The mechanism behind it

In a constant-product AMM such as classic Uniswap, the pool follows x * y = k. The product stays constant, so the reserves have to shift when traders push the pool price toward the market price.

In practice, the sequence looks like this:

You deposit two assets of equal value.

The market price between them changes.

Arbitrage traders trade against the pool.

The pool ends up holding a different mix of tokens.

Your position is worth less than a simple hold of the original assets.

That last step is the whole concept. It is not a protocol fee. It is not a bug. It is the cost of letting an automated market maker keep your position market-neutral while prices move.

If you want a quick refresher on pool design before going deeper, Yield Seeker’s guide to how liquidity pools work in practice covers the mechanics clearly.

The formula and why it matters

The standard expression is:

IL = 2 × √(price ratio) / (1 + price ratio) - 1

Here, the price ratio is the new price divided by the starting price for one asset relative to the other.

The takeaway is straightforward: IL is not linear. Small deviations create small underperformance. Large deviations create much larger underperformance, which is why volatile pairs get all the attention in beginner guides.

A few standard formula outputs make the shape of the curve clear:

Price change | Impermanent loss |

|---|---|

1.25x | 0.6% |

1.5x | 2.0% |

2x | 5.7% |

3x | 13.4% |

5x | 25.5% |

That matters less for USDC/USDT than for ETH/USDC. If both assets usually trade near $1, price divergence is limited, so impermanent loss is often negligible compared with fees, incentives, and smart contract risk. That is the practical lens stablecoin investors should use.

Why stablecoin LPs should read IL differently

A lot of impermanent loss content is written around assets that can double, halve, or trend for months. That is useful for understanding the math, but it can distort decision-making for someone allocating idle stablecoins.

In stablecoin pools, the core question is not, "How bad can IL get in a volatile market?" The better question is, "How often do these two assets materially break their peg, and does the fee income justify that tail risk?"

That is a different evaluation process. It puts more weight on pool composition, peg history, liquidity depth, and the protocol’s ability to route capital toward pools where the yield is real and the divergence risk stays contained.

Yield Seeker is built around that reality. Our system focuses on stablecoin opportunities where IL is usually a secondary variable, then filters for the risks that matter more in practice: depeg exposure, incentive quality, protocol reliability, and whether net yield still holds up after conditions change.

Why the term causes confusion

“Impermanent” describes the state of the position while the price relationship can still move back toward where you entered. It does not mean harmless.

If you withdraw while the assets are still diverged, the underperformance becomes your realized result. For stablecoin LPs, that usually only becomes meaningful during stress events, which is exactly why monitoring matters. A pool can look low-risk for months, then behave like a different product during a depeg.

That is why experienced LPs do not treat IL as an isolated formula. They treat it as one variable inside a larger capital allocation problem.

A Step-by-Step Numerical Example

A volatile pair makes the mechanics easy to see, so start there before translating the lesson to stablecoins.

Starting position

A pool starts with 10 ETH at $2,000 and 10,000 USDT. Total position value is $30,000.

That is a standard 50/50 deposit by value. One side is the volatile asset. The other is the quote asset.

Then ETH doubles

ETH moves from $2,000 to $4,000.

An AMM does not keep your original token balances frozen. Arbitrage traders keep buying ETH from the pool until the pool price matches the market price. As that happens, your LP position ends up holding less ETH and more USDT than you started with.

For a constant-product pool, the rebalanced position is about:

7.07 ETH

28,284 USDT

At the new ETH price, that LP position is worth about $56,568.

Compare that with holding

If you had done nothing and just held the assets:

10 ETH × $4,000 = $40,000

10,000 USDT = $10,000

Total hold value = $50,000

That mismatch tells you the starting setup needs to be compared on a like-for-like basis. The clean way to read the example is the relative outcome: after a large move, the pool automatically sells part of the winner and accumulates more of the slower asset. Your dollar value can rise while still lagging a simple hold benchmark.

That lag is impermanent loss.

For readers who want the broader risk context around LP positions, our guide to liquidity pool risk management covers the parts the formula misses, including smart contract risk, incentive decay, and exit liquidity.

What caused the underperformance

Nothing failed. The AMM worked exactly as designed.

It kept quoting a tradable price through the whole move. Traders took the other side. Your position got rebalanced step by step.

In practical terms:

You finish with less of the appreciating asset

You finish with more of the weaker or flat asset

You collect fees, which may offset some or all of the gap

That last point is where many LP decisions are won or lost. Impermanent loss is not a standalone verdict. It is one side of a trade-off between rebalancing drag and fee income.

Here’s a good video explainer if you want to see the mechanics visually:

Why stablecoin investors should read this differently

Stablecoin LPs should not copy the fear level from an ETH example.

In a well-constructed stablecoin pool, both assets are designed to stay near the same price. That keeps divergence small most of the time, which means impermanent loss is often a secondary concern rather than the main risk driver. The primary work involves screening for depeg risk, shallow liquidity, weak incentives, and protocols that cannot keep net yield attractive after conditions change.

That is the problem Yield Seeker is built to handle. It helps stablecoin investors find pools where yield is still worth the risk after accounting for pool composition, fee quality, and the chance that a low-IL position stops behaving like a stable pair during stress.

Comparing Pool Types and Their IL Risk

Not all liquidity pools deserve the same fear premium.

The biggest mistake in impermanent loss explained content is treating every pool as if it behaves like a volatile token pair. Stablecoin investors should not make decisions from ETH-pair examples alone.

A practical comparison

Here’s the decision frame I use.

Pool type | Typical IL behavior | Main trade-off |

|---|---|---|

Volatile pair | High sensitivity to price divergence | Higher fee potential, higher risk |

Stablecoin pair | Usually minimal when peg holds | Lower directional upside |

Correlated asset pair | Often lower than fully uncorrelated assets | Correlation can break under stress |

Stablecoin pools are a different category

For a stablecoin pair, the relative price usually stays near parity. That changes the whole IL profile.

According to Soma Finance’s discussion of impermanent loss in stablecoin pools, a 1% temporary depeg in a 50/50 stablecoin pool results in about 0.05% IL. The same source notes that recent 2025-2026 data shows stablecoin pools on Base average less than 0.1% IL annually, compared to 15-25% for typical ETH pairs.

That is the overlooked point.

If your goal is earning on idle USDC rather than farming upside from a volatile asset, stablecoin LPing often turns impermanent loss from a primary risk into a secondary one. It does not remove risk entirely. Peg breaks still matter. But the baseline exposure is lower.

For a broader framework on evaluating these trade-offs, this Yield Seeker piece on navigating liquidity pool risks is worth reading.

Stablecoin LPs do not win by ignoring impermanent loss. They win by choosing a setup where it usually stays small enough that other variables matter more.

What works and what does not

Some patterns hold up consistently.

Works well: Pairing assets that are intended to stay close in value.

Usually works poorly: Chasing the highest displayed APY in a volatile pool without asking what price move would do to the position.

Works with caveats: Correlated-asset pools can reduce divergence, but only while correlation behaves.

The treasury perspective

Teams holding stable balances often do not need directional token exposure. They need accessible yield, predictable risk, and less operational overhead.

That is why stablecoin pools deserve their own category in portfolio design. For many users, especially on Base, the right comparison is not “LP versus HODL a volatile token.” It is “low-maintenance onchain yield versus idle stablecoin cash.”

Proven Strategies to Mitigate Impermanent Loss

The most effective way to reduce impermanent loss is not clever math. It is structuring the position so the math works in your favor.

That starts with pool selection. Then it moves into fee economics, position design, and automation.

Choose the right pair first

If you remember one thing, make it this: the pair determines the risk regime.

A stablecoin LP position and a volatile-token LP position may both be called “liquidity provision,” but they do not behave the same way. For many investors, the simplest mitigation strategy is also the strongest one. Use pools where both sides are designed to stay close.

Single-sided staking can also make sense when you want yield without managing a paired-asset exposure. This Yield Seeker article on staking LP tokens is a useful reference point for where LP-based yield fits relative to other options.

Understand the fee trade-off

Fees are the revenue side of the LP equation.

They can offset IL. Sometimes they more than offset it. But “high fee pool” is not a free pass. High fees often come from high trading activity, and high trading activity often exists because the assets are volatile or the market is repricing them aggressively.

That means the right question is never “What is the APY?” It is “What kind of movement generates this APY, and what does that do to my inventory?”

A pool can pay well because it is productive, or because it is dangerous. The interface usually does not tell you which one fast enough.

Use concentrated liquidity when the assets justify it

Concentrated liquidity changed the IL discussion.

With Uniswap V3, LPs choose a price range rather than providing liquidity across the full curve. That matters because the position only actively rebalances within the chosen range.

According to Speedrun Ethereum’s guide to impermanent loss math, with concentrated liquidity on Uniswap V3, IL only accrues within an LP's chosen price range, and a tight 0.99-1.01 range for a USDC/USDT pair can incur less than 0.01% IL. The same source notes that backtests from protocols like Yield Seeker show AI agents dynamically adjusting these ranges can cut effective IL by 60%.

That makes concentrated liquidity especially compelling for stablecoin pairs. The assets already tend to stay near each other. A tight range lets the LP focus capital where trading is likely to happen while keeping divergence exposure constrained.

What active management solves

Concentrated liquidity is powerful, but it creates operational work.

You need to monitor whether the range is still appropriate. If the position drifts out of range, fee generation stops. If the market regime changes, a once-sensible range can become dead capital or mispriced risk.

That is where automation starts to matter.

A practical mitigation stack looks like this:

Start with low-divergence assets: Stablecoin pairs are the cleanest example.

Use concentrated ranges where market structure supports it: Narrow when price behavior is stable, wider when uncertainty is higher.

Track realized fees against divergence risk: Do not evaluate the position from APY alone.

Automate adjustments when possible: Manual LP management breaks down fast for busy users and treasury operators.

What usually fails in real portfolios

Three mistakes show up repeatedly.

Treating all AMMs as equivalent. Pool mechanics matter.

Using a static range in a changing market. Good initial positioning still goes stale.

Confusing low effort with low risk. Passive LPing in the wrong pool is still active exposure.

The strongest IL mitigation is not one trick. It is a disciplined setup where asset choice, fee opportunity, and position management all point in the same direction.

The Yield Seeker's Takeaway on IL

Impermanent loss is real, but it is not a reason to avoid DeFi yield across the board.

It is a design constraint. Once you understand where it comes from, you can choose structures where it matters a lot less. That is the part many guides miss.

For volatile pairs, IL can be the dominant risk. For stablecoin-focused liquidity provision, it often is not. The better framing is portfolio-specific. If you want exposure to a fast-moving asset, LPing may underperform holding when prices diverge. If you want yield on stable balances, the same fear often gets overstated.

The practical takeaway

Busy professionals, treasury operators, and new DeFi users do not need to memorize every AMM formula. They need to know which setups create avoidable risk.

That leads to a simple hierarchy:

Avoid uncorrelated volatility unless you want that exposure

Prefer stable or tightly correlated pairs when yield is the goal

Use concentrated liquidity carefully

Rely on active monitoring or automation if the strategy requires it

What impermanent loss explained should leave you with

The mature view is not “IL is scary.” It is “IL is measurable.”

That changes how you act. You stop chasing raw APY. You compare expected fee income against the kind of divergence the pair is likely to experience. You pay more attention to pool design. You stop assuming every LP strategy belongs in the same risk bucket.

The best LPs do not avoid impermanent loss by pretending it is not there. They choose positions where it is acceptable, compensated, or operationally controlled.

For stablecoin holders in particular, that is good news. You can participate in DeFi without taking the full volatility profile implied by most generic LP tutorials. The safer path usually is not more complicated. It is just more selective.

If you want a hands-off way to put that approach into practice, Yield Seeker helps you earn automated, risk-aware yield on stablecoins on Base without manually hunting pools, tracking dashboards, or constantly rebalancing positions yourself. You can start with as little as $10 USDC, keep funds accessible at all times, and let a personalized AI agent monitor DeFi opportunities in real time through a clean interface built for both beginners and experienced users.