Your wallet probably has a bucket of stablecoins doing nothing. USDC sits there, price stable, no drama, no yield. That feels safe, but in DeFi, idle capital is usually a choice, not a necessity.

Liquidity pools are one of the main ways people put those assets to work. You deposit tokens into a smart contract, traders use that liquidity to swap, and you earn a share of the fees. Simple in theory. Messy in practice.

The messy part is why many people never get past the tutorial stage. They learn the definition, try one pool, then realize they now need to track price movement, fee income, pool depth, chain fragmentation, and whether the yield still makes sense after risk. That’s where the gap is. Most guides teach manual participation. Real users usually need a cleaner path.

Putting Your Stablecoins to Work

A common starting point looks like this. You moved funds on-chain, parked them in USDC, and decided to wait for a better opportunity. Days pass. Then weeks. The capital is still safe by stablecoin standards, but it’s not productive.

Liquidity pools change that equation. Instead of letting your stablecoins sit in a wallet, you place them into a market structure that traders use every minute of the day. Each swap pays fees. If your capital is in the pool, you earn a share of that activity.

For stablecoin holders, that matters because the goal usually isn’t speculation. It’s cash management. You want dollars on-chain that stay accessible while earning something better than zero. That makes stablecoin liquidity pools especially relevant. They’re built around assets that aim to stay near the same value, so the job is less about betting on price direction and more about collecting fees efficiently.

Why this attracts busy investors

Many participants aren’t trying to become full-time LPs. They want three things:

Accessible yield: a way to earn on stable balances without locking funds into a rigid product

Operational simplicity: fewer dashboards, fewer decisions, fewer chances to make avoidable mistakes

Risk clarity: a better sense of what can go wrong before capital moves

Liquidity pools can feel passive from the outside. In reality, they’re closer to renting out inventory in a market that never closes.

That’s the useful mental model. Your stablecoins become working inventory. Traders consume access to that inventory. You collect fees for making the market usable.

The catch is that not all pools behave the same, and not all yield is worth chasing. Some setups are straightforward. Others demand constant oversight. That difference matters more than the headline APY.

How Liquidity Pools and AMMs Function

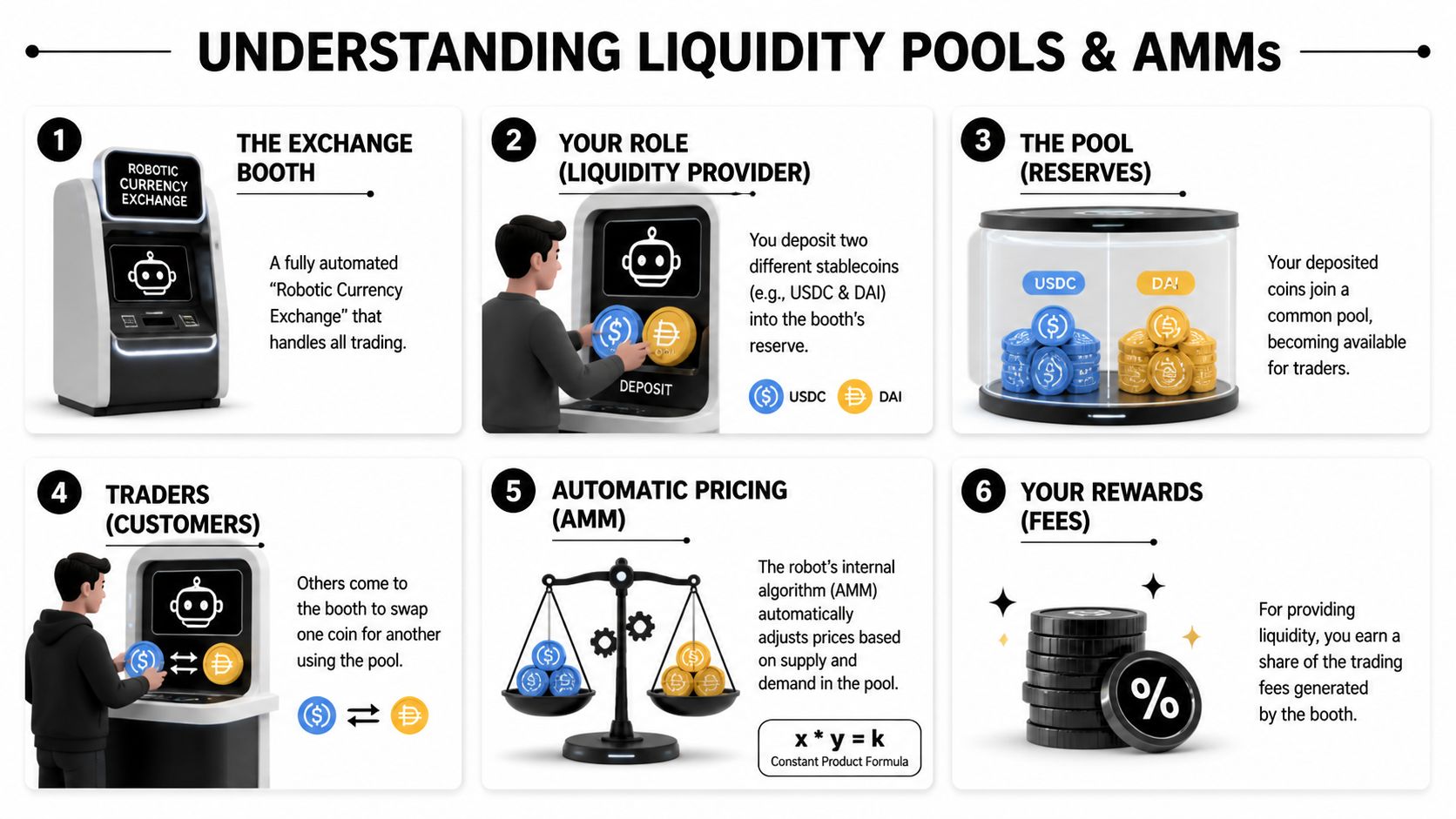

Think of a liquidity pool as a self-service exchange booth. There’s no clerk behind the glass and no order book matching buyers to sellers. The booth is stocked with assets, and a robot handles pricing and swaps based on a fixed rule.

You are the person stocking the booth. If you provide liquidity to a pair like USDC and DAI, you deposit both assets into the pool. Traders then come to that pool whenever they want to swap one for the other.

The robotic exchange booth model

The robot inside the booth is the automated market maker, or AMM. In many classic designs, it follows the constant product rule, often written as x * y = k. You don’t need to do the math by hand. What matters is what the rule does.

When a trader buys one asset from the pool, the balance shifts. The AMM responds by adjusting the price automatically. If the pool has less of one token after the trade, that token becomes more expensive relative to the other one. No human market maker has to step in.

Here’s the practical flow:

You deposit assets: usually a pair of tokens into a smart contract.

The pool holds reserves: those reserves are what traders swap against.

Trades change balances: every swap changes the ratio of assets in the pool.

The AMM updates pricing: price moves as reserves move.

Fees accrue to LPs: each trade pays the pool, and providers earn their share.

If you want a deeper look at the people who fund these markets, this guide on what liquidity providers do in practice is a useful companion.

Why AMMs replaced manual market making for many use cases

Traditional exchanges rely on bids and asks. AMMs rely on pooled inventory and code. That makes liquidity pools useful for decentralized trading because they’re always available. A trader doesn’t need to wait for someone else to take the other side manually.

Practical rule: If a DeFi product promises trading without an order book, a liquidity pool or similar pooled mechanism is usually doing the heavy lifting in the background.

That also explains why LPs matter so much. Without them, the booth is empty. No inventory means no swaps, no fees, and no market.

Where fees come from

Fees aren’t magic yield. They come from actual trading activity. If a pool has steady volume, LPs can earn consistently. If volume dries up, the fee stream dries up too.

That’s why good liquidity pools are not just about high advertised returns. They need real usage. In DeFi, sustainable yield usually starts with a market people use.

Navigating Different Pool Types

Not all liquidity pools belong in the same bucket. The first split that matters is volatile pools versus stablecoin pools. After that, you need to understand whether the pool uses broad liquidity or concentrated liquidity.

If your priority is capital preservation with yield, this distinction matters more than the protocol logo.

Volatile pairs and stablecoin pairs

A pool like ETH/USDC gives you exposure to an asset that can move hard in either direction. That can create strong fee income when volume is high, but it also creates more moving parts. Your pool position changes as price changes, and your returns depend on more than trading fees alone.

A pool like USDC/USDT is different. Both assets are designed to stay close in value, so the strategy is less exposed to major price divergence. That makes stablecoin pools easier to reason about for people treating DeFi as treasury management rather than directional trading.

A simple comparison helps:

Pool type | What you’re optimizing for | Main challenge |

|---|---|---|

Volatile pair | Higher fee opportunity during active markets | Asset price divergence can overwhelm fee income |

Stablecoin pair | More predictable fee collection and lower price mismatch | Lower upside than a well-timed volatile strategy, plus peg and protocol risk |

Stablecoin pools aren’t risk-free. Smart contract risk, pool design, and stablecoin-specific issues still matter. But they usually remove the most obvious source of chaos, which is large relative price movement between the two assets.

Full-range pools and concentrated liquidity

Older AMM designs spread your liquidity across the entire possible price curve. That’s simple, but inefficient. Much of your capital sits where no one trades.

Concentrated liquidity changed that. In Uniswap V3-style pools, LPs choose a price range where their capital is active. That design can deliver up to 4000x higher capital efficiency than Uniswap V2 because liquidity is focused where trading is most likely to happen, according to Keyrock’s guide to liquidity pool management.

That efficiency comes with a trade-off. You now have a position that behaves more like a managed strategy than a static deposit. If price moves outside your chosen range, your capital can stop earning effectively until you reposition.

Narrow ranges can boost fee capture. They also create more maintenance work.

Which pool type fits which user

If you’re choosing based on actual operating style, not theory:

Use stablecoin pools when your priority is preserving purchasing power and earning from swaps, not speculating on token appreciation.

Use volatile pools carefully if you already understand how price movement can change the composition of your position.

Use concentrated liquidity only if you’ll monitor it, or if you have a system that will.

That last point is where many LPs get tripped up. Concentrated liquidity is powerful. It just isn’t passive unless someone or something manages it.

Key Risks and Performance Metrics

Typically, the initial focus is on APY. That’s useful, but it’s not enough. A liquidity pool should be judged like an operating business. You care about revenue, depth, utilization, and downside.

The three numbers people usually check first are TVL, APY, and trading fees. TVL tells you how much capital is already in the pool. APY gives you a snapshot of projected return. Fee generation tells you whether the pool is earning from real usage or mostly relying on incentives.

Metrics that actually matter

A pool with solid depth can usually absorb trades more cleanly. A pool with healthy fee flow often reflects real demand. A flashy APY with weak underlying activity deserves skepticism.

Here’s a practical screening view:

TVL: deeper pools usually handle swaps with less slippage and tend to attract more sustained trading activity

Fee source: fees driven by real swaps are more durable than temporary token incentives

Pool composition: stable pairs behave differently from volatile pairs, even when the APY headline looks similar

Strategy burden: some pools are simple deposits; others require active position management

That last point is underappreciated. The same yield number can mean very different workloads depending on the pool design.

Impermanent loss is the risk most people underestimate

Impermanent loss, usually shortened to IL, is what happens when the relative price of the assets in your pool changes and your position ends up worth less than holding the tokens outside the pool.

The easiest way to understand it is operationally, not mathematically. You deposit two assets. The pool keeps rebalancing them as traders swap. If one asset rises sharply, the pool systematically sells some of your winner and leaves you with more of the laggard. You still earned fees, but you may own a worse mix of assets than if you had just held them.

This isn’t a niche problem. Approximately 50% of liquidity providers on Uniswap V3 experience negative returns after accounting for impermanent loss, and in some volatile pools IL exceeds fee gains by 70–75%, according to SmartCredit’s analysis of DeFi liquidity pools.

If you want a detailed breakdown of the hazards LPs face beyond IL, this piece on liquidity pool risks for DeFi users is worth reading.

The mistake isn’t joining a pool. The mistake is treating fee income as the whole return while ignoring what happened to the asset mix underneath.

A non-mathematical way to evaluate IL risk

Ask these questions before depositing:

Question | Why it matters |

|---|---|

Can these two assets diverge sharply? | Bigger divergence usually means higher IL pressure |

Does the pool need active range management? | If yes, your returns depend partly on execution, not just market activity |

Are fees likely to outweigh the position drift? | Fee income has to compensate for risk, not just exist |

Would I be comfortable simply holding both assets? | If not, providing them as liquidity may not fit your risk profile |

For stablecoin pairs, IL is usually less severe because the assets are designed to remain close in value. For volatile pairs, IL can become the main driver of outcome. That’s why a high APY can still lead to a disappointing result.

Common Manual Strategies for LPs

Manual liquidity provision is less like setting up a savings product and more like running a small trading operation. Even conservative LPs end up doing research, monitoring, and periodic rebalancing.

A careful operator usually starts with protocol selection. That means checking whether the venue is established, whether the pool is active, and whether the design matches the goal. Stablecoin treasury management and yield chasing are not the same job.

What manual LPs actually do

Some of the work is front-loaded:

Protocol review: checking the pool design, the assets involved, and whether the venue has enough usage to make fee income meaningful

Pool selection: comparing stable pairs against volatile pairs and deciding whether concentrated liquidity is worth the management burden

Execution planning: deciding how much capital to allocate, which chain to use, and how often to review the position

Then the ongoing work begins. Manual LPs watch utilization, fee trends, and whether market conditions changed enough to justify moving capital. If they’re in concentrated liquidity, they also need to watch whether the position is still in range.

What works and what usually doesn’t

One manual approach that often holds up is focusing on deeper pools where fees have a chance to offset risk. In constant product AMMs, a 2x price move causes an LP to capture only about 71% of the asset’s appreciation compared with holding, while higher fees in pools with over $100M TVL can offset some of that downside, according to Amberdata’s AMM risk analysis.

What usually fails is chasing the highest displayed yield without asking why it exists. Small pools can look attractive, but lower depth often means worse execution, weaker fee reliability, and less room for mistakes.

Good manual LPs spend less time asking “What pays the most?” and more time asking “What am I being paid to absorb?”

The hidden cost of doing it yourself

Manual management has a real operational cost:

You monitor multiple dashboards.

You compare opportunities across chains and protocols.

You decide when to stay put and when to move.

You repeat the process every time conditions change.

That’s manageable if DeFi is your day job. It’s a poor fit if you just want idle stablecoins to earn intelligently while staying liquid.

Automating Stablecoin Yield with Yield Seeker

Automation becomes useful when the strategy itself stops being passive. That’s exactly what happened to liquidity pools. The market still offers straightforward opportunities, but the best decision often depends on changing fee conditions, chain-specific opportunities, and whether moving capital is worth the effort.

One reason is fragmentation. A single LP can now face choices across multiple chains, bridges, and pool designs. That isn’t just annoying. It affects returns. A future-dated industry trend cited in Kraken’s liquidity pool explainer says TVL in L2 DEX pools on chains like Base grew 150% in Q1 2026, and that AI agents that auto-migrate capital reduced bridging losses by 25% in reported examples. The same source notes that manual users often miss meaningful APY differences across chains.

What automation changes

Instead of checking opportunities by hand, an automated system can monitor positions continuously and shift capital when the risk-reward profile changes. For stablecoin holders, that’s a more practical setup than trying to act like an active LP in your spare time.

That’s the context where automated liquidity management on Yield Seeker fits. The platform uses an AI agent to monitor and allocate stablecoin capital across DeFi opportunities on Base, including liquidity-pool-based strategies, with funds remaining accessible rather than locked. For users who don’t want to manually hunt pools, compare dashboards, and time reallocations themselves, that changes the operating model.

Where AI helps most

The best use of AI here isn’t hype. It’s task compression.

Monitoring: tracking opportunities without manually refreshing multiple protocols

Reallocation: reacting faster when yields shift or a setup degrades

Risk awareness: avoiding the common habit of judging a pool only by displayed yield

Accessibility: making a complex workflow usable for people who aren’t full-time DeFi participants

There’s also a communication layer to this. Teams explaining strategy updates or treasury decisions often need visuals that are clearer than a text thread. Tools that generate hyper-realistic videos can help turn complex on-chain strategy explanations into something clients, communities, or internal stakeholders can follow.

A short product walkthrough helps make the automation model more concrete:

The point isn’t that AI removes all risk. It doesn’t. The point is that it can remove a large share of the repetitive analysis and execution burden that makes manual liquidity provision unrealistic for the average individual investor.

Frequently Asked Questions for Beginners

Is providing liquidity the same as staking

No. Staking usually means locking a token to support a network or protocol and earning rewards for that role. Providing liquidity means depositing assets into a pool so traders can swap against them. The return profile is different, and liquidity pools introduce pool-specific risks like asset rebalancing and smart contract exposure.

What’s the difference between APR and APY here

APR is the simple annualized rate without compounding. APY assumes rewards are reinvested over time. In DeFi interfaces, the distinction matters because some returns depend on active compounding and some don’t.

Can I lose my entire initial deposit

Qualitatively, yes, in the sense that DeFi carries real protocol and smart contract risk. In more common scenarios, users don’t lose everything but can still end up with disappointing results because fees didn’t offset the risks they took. That’s especially true when people join pools they don’t fully understand.

Do I need a large amount to start

No. Many DeFi tools let users begin with relatively small amounts. The more important question is whether the amount is large enough to justify transaction costs, monitoring effort, and the learning curve.

Are stablecoin liquidity pools safer than volatile pools

Usually they’re simpler, which often makes them better suited to cautious users. They reduce one major problem, which is large price divergence between the paired assets. But they still carry protocol risk, stablecoin-specific risk, and execution risk.

Can I withdraw whenever I want

In many liquidity pools, yes, subject to how the protocol works and current network conditions. What you receive back may not match the exact token mix you deposited, because the pool composition changes as trades happen.

If you want a hands-off way to put stablecoins to work without manually managing liquidity pools, Yield Seeker offers an AI-driven approach on Base with low-friction deposits, real-time monitoring, and no lockups or withdrawal fees. It’s built for people who want DeFi yield without turning portfolio management into a second job.