You already know the feeling. You're holding stablecoins because you want optionality, low volatility, and fast access to capital. Then you check your wallet a week later and realize the balance is exactly where you left it.

That's fine if the cash is waiting for a near-term use. It's inefficient if the funds are just parked out of habit.

Traditional finance solved this problem a long time ago through the money market. Crypto didn't invent the idea of earning on idle cash. It removed some of the gatekeepers, changed the rails, and exposed the mechanics in software. If you understand how the traditional money market works, DeFi yield strategies start making a lot more sense.

Your Stablecoins Are Idle Let's Change That

A common pattern in crypto looks like this. Someone sells a volatile position into USDC, plans to “wait for the next move,” and then leaves that capital untouched. Days turn into weeks. The wallet stays liquid, but the money does nothing.

In TradFi, treasury teams don't usually leave large cash balances completely idle unless they need instant spending access with zero operational friction. They sweep excess cash into tools designed for short-term yield and liquidity. That instinct sits at the heart of the money market.

Stablecoin holders face the same decision, just on different rails. USDC in a wallet is digital cash. Useful, flexible, and easy to move. But unless it's deployed into a lending market, tokenized treasury strategy, or another cash-like yield venue, it's just sitting there.

Idle stablecoins are a portfolio choice, even when they feel like a temporary default.

That doesn't mean every dollar should be pushed into the highest advertised APY. It means cash management deserves the same attention in crypto that it gets in traditional finance. The fundamental question isn't “Should I chase yield?” It's “What level of risk, access, and complexity am I willing to accept for my cash allocation?”

Where the lightbulb usually turns on

Initial thoughts about yield in DeFi often gravitate towards speculative products: capital-amplified farming, incentive-heavy pools, long-tail tokens. That's often the wrong starting point.

A better starting point is simpler:

You want liquidity: You may need the funds back soon.

You want stability: You're using stablecoins because principal swings defeat the purpose.

You want some return: Even modest yield is better than none if the risk is controlled.

That's money market thinking.

Once you see stablecoins as working capital instead of dormant chips on the sidelines, the bridge between TradFi and DeFi becomes obvious. The tools differ. The principle doesn't. Put excess cash into short-duration, liquid strategies that aim to preserve usability while earning something along the way.

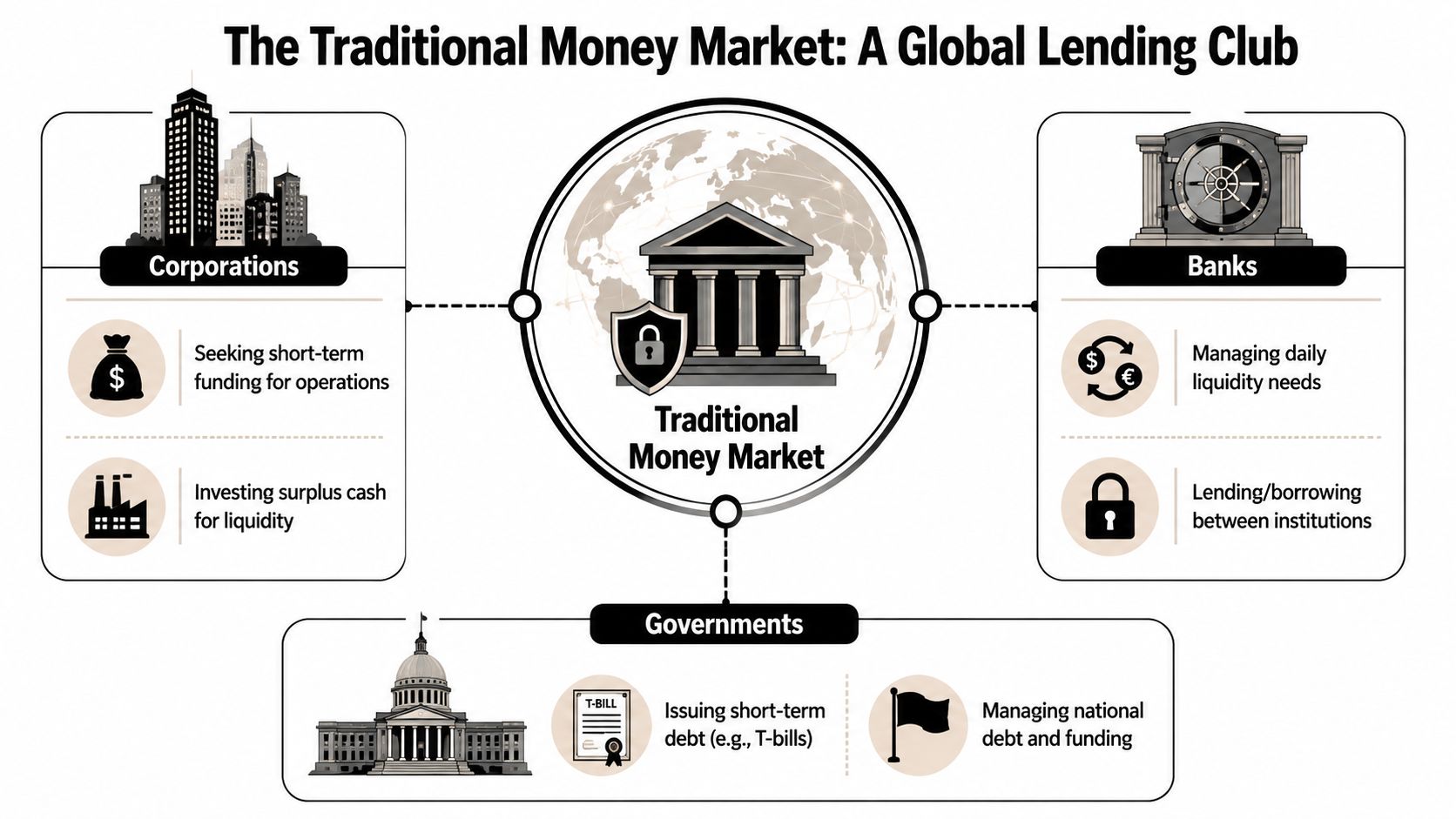

Understanding the Traditional Money Market

The traditional money market is best understood as a giant short-term funding layer for the financial system. Corporations, banks, governments, and investment funds all use it when they need to borrow cash briefly or park cash safely for a short period.

The instruments are familiar once you strip away the jargon. Treasury bills are short-term government debt. Certificates of deposit are bank-issued time deposits. Commercial paper is short-term borrowing by corporations. They usually mature in less than a year, which is why the money market is about cash management, not long-horizon investing.

In the U.S., money market funds remain a major institutional cash vehicle. The SEC reported 289 money market funds in April 2026, up 4.3% year over year, and the Investment Company Institute reported $7.87 trillion in total money market fund assets for the week ended June 10, 2026, according to Vanguard's overview of money market funds.

What participants actually use it for

A treasury team at a company may have payroll, vendor payments, and tax obligations coming up, but not all on the same day. Parking surplus cash in a money market vehicle lets that team keep funds accessible while earning a return.

Banks use the same ecosystem to manage daily funding needs. Governments issue short-term debt into it. Investors use money market funds when they care more about liquidity and capital preservation than upside.

Here's a simple view:

Participant | What they want | Typical money market use |

|---|---|---|

Corporations | Access to cash without leaving balances idle | Invest surplus operating cash |

Banks | Daily liquidity management | Borrow and lend short term |

Governments | Reliable short-term funding | Issue Treasury bills |

Investors | Stability and convenience | Hold money market funds |

For readers outside the U.S., products such as Australian cash management accounts are a useful analogue because they package the same core idea: keep cash accessible while seeking some return.

What works and what doesn't

What works is treating the money market as a cash tool, not a growth asset. It's for near-term liquidity, not for beating equities or long-duration credit.

What doesn't work is assuming all cash-like products are interchangeable. Some have different holdings, different access rules, and different behavior under stress. If you want a broader look at other short-duration yield options, treasury yield alternatives help frame where money market exposure fits versus adjacent cash strategies.

How DeFi Reimagines the Money Market

DeFi takes the same economic function and rebuilds it with smart contracts. Instead of brokers, custodians, fund transfer agents, and bank portals, you interact with on-chain pools that accept deposits and route borrowing and lending through code.

If TradFi money markets are a guarded institutional plaza, DeFi money markets are an open protocol layer. Anyone with a compatible wallet and supported assets can participate. That change in access is a big deal. It turns a treasury function that was historically wrapped in institutional infrastructure into something closer to an internet-native savings and funding network.

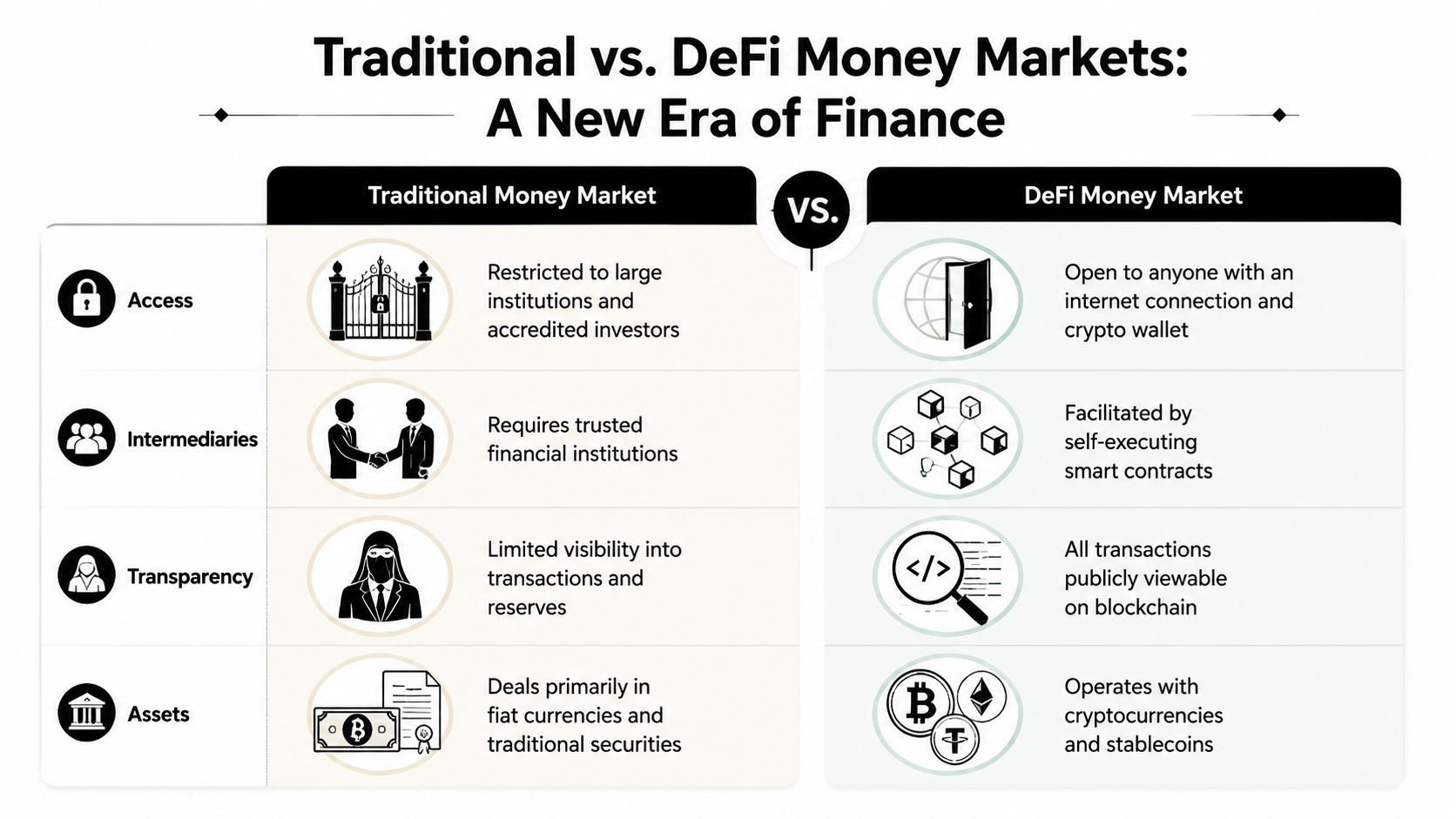

Side-by-side differences that matter

The easiest way to understand DeFi money markets is to compare mechanics, not ideology.

Dimension | Traditional money market | DeFi money market |

|---|---|---|

Access | Usually mediated by institutions | Open to wallet users |

Execution | Operational layers and intermediaries | Smart contracts handle rules |

Visibility | Limited view into positions and flows | On-chain activity is inspectable |

Assets | Fiat cash and short-term securities | Stablecoins and crypto collateral |

That doesn't mean DeFi is automatically safer or better. It means the user gets a different trade-off set. You gain speed, programmability, and direct access. You also take on new forms of technical and protocol risk.

A useful backdrop here is the growing overlap between banking and digital dollars. For anyone tracking that convergence, this insight into banks and stablecoins helps explain why the line between traditional cash infrastructure and crypto rails keeps getting thinner.

Here's a short visual explainer that helps make the comparison concrete.

What DeFi gets right

The strongest feature of DeFi money markets is programmable liquidity. A protocol can continuously price borrowing demand and lender supply, update rates automatically, and let users enter or exit without waiting for back-office processes.

That creates a more direct relationship between capital and yield. If demand to borrow USDC rises, lenders typically see rates adjust. If demand falls, yields compress. The market speaks faster.

DeFi didn't change the purpose of the money market. It changed who can access it and how quickly it can react.

What DeFi doesn't solve by itself

Open access can create false confidence. A nice interface doesn't remove smart contract risk. Transparent reserves don't guarantee good governance. Instant liquidity can disappear if too many users rush for the exit at once or if collateral quality gets questioned.

So the right mental model is this: DeFi reimagines the money market as open software infrastructure. The upside is speed and accessibility. The cost is that users need sharper risk judgment than they would in a plain bank deposit.

The Building Blocks of DeFi Money Markets

At the user level, DeFi money markets are built from a few simple pieces. Once you understand those pieces, most platforms stop looking mysterious.

Stablecoins are the cash leg

The core deposit asset is usually a stablecoin such as USDC. That's not an accident. In traditional money markets, participants want minimal principal volatility. In DeFi, stablecoins play the same role. They're the closest thing the ecosystem has to operational cash.

When someone deposits USDC into a lending protocol, that capital typically becomes part of a pool borrowers can access against collateral. The lender earns yield because someone on the other side is paying to use that liquidity.

This is why stablecoin yield is usually the first serious DeFi strategy professionals explore. It maps cleanly to a familiar treasury question: how do I keep cash productive without turning it into a directional bet on crypto prices?

Yield-bearing tokens are the receipt

Many protocols issue a tokenized claim on your deposit. Depending on the protocol, that might look like an interest-accruing balance or a receipt token that represents your share of the pool.

Think of it as a programmable account statement. Instead of waiting for month-end reporting, the protocol updates value on-chain. Your position reflects accrued yield in real time or near real time, based on the protocol's accounting design.

Practical takeaway:

Deposit stablecoins: You supply the cash-like asset.

Receive a claim token or updated balance: This proves ownership of the deposit.

Earn variable yield: The rate moves with market conditions.

Redeem when needed: You exchange the claim back for underlying funds, subject to protocol liquidity.

Risk management still exists, just in a different form

Traditional markets are full of guardrails, even when users don't notice them. One useful benchmark comes from the SEC's 2023 final rule, which required institutional prime money market funds to transact at a floating NAV rather than a fixed $1.00 share price, a structural shift described in the verified SEC rule summary provided in your brief. That's a reminder that even cash-like products need explicit mechanisms to handle stress and asset-value movement.

DeFi protocols deal with the same underlying problem in software form. They may use collateral rules, utilization-driven rate changes, reserve parameters, withdrawal logic, or governance-controlled safeguards to keep the system solvent and liquid.

Practical rule: If a DeFi product advertises money-market-like stability, check the mechanism. Stability only counts if the protocol can explain how it manages liquidity under pressure.

What works is choosing protocols where the moving parts are understandable. You should be able to answer basic questions: What assets back the market? Who borrows? How does the protocol respond when utilization spikes? What can change through governance?

What doesn't work is treating “stablecoin yield” as if it's self-explanatory. In practice, the details under the hood matter more than the label on the front end.

Navigating DeFi Risks and How to Mitigate Them

The mistake most new users make is focusing only on the displayed yield. In a DeFi money market, the better question is what has to go right for that yield to be earned safely.

Traditional regulation offers a useful benchmark for liquidity discipline. In Europe, MMFs must hold 10% daily and 30% weekly liquid assets, while U.S. rules require similar buffers. Those requirements matter because they show how serious cash products plan for withdrawals before stress hits, not after. The same principle should guide how you evaluate DeFi lending markets.

Four risks that deserve real attention

Smart contract risk: Bugs, flawed logic, or integration failures can break a protocol that looked fine from the surface.

Stablecoin risk: A stablecoin can lose its dollar parity, face issuer-specific problems, or become harder to redeem smoothly.

Liquidity risk: Your funds may be theoretically withdrawable but practically delayed if protocol liquidity is tight.

Governance and operational risk: Teams or token holders can approve changes that alter risk, collateral standards, or strategy behavior.

None of these are abstract. They're the actual cost of operating on open rails.

Mitigation is mostly about process

The good news is that risk control in DeFi is usually less about prediction and more about filtering.

Risk | What to check |

|---|---|

Smart contract issues | Audit history, code maturity, simplicity of design |

Stablecoin weakness | Issuer credibility, reserve transparency, redemption reputation |

Liquidity pressure | Withdrawal conditions, pool depth, borrower quality |

Governance changes | Upgrade powers, admin controls, decision track record |

Some practical habits help more than people expect:

Prefer boring over novel: Mature protocols with understandable mechanics usually beat flashy launches for cash allocations.

Split exposure: Diversifying across more than one protocol or stablecoin reduces single-point failure risk.

Read the withdrawal path: It's not enough to know how deposits work. Know what redemption depends on.

Track governance: A protocol can become riskier even when your wallet balance looks unchanged.

For a more detailed framework, this guide to DeFi risk management is useful because it focuses on process rather than hype.

When users lose money in DeFi cash strategies, it's often because they outsourced due diligence to the APY number.

What good operators do differently

Good operators assume yields are variable, liquidity can tighten, and stablecoins are not identical. They build around those assumptions.

Bad operators chase the highest number on the screen and call that a strategy.

That difference sounds small, but it changes everything. A money market mindset in DeFi means preserving access to capital comes first. Yield is the reward for disciplined placement of liquidity, not an excuse to ignore the plumbing.

A Safe Path for Stablecoin Holders to Earn Yield

If you wanted to do this manually, the path is straightforward on paper.

You set up a self-custody wallet. You fund it with a stablecoin such as USDC. You choose a DeFi lending protocol, approve the transaction, deposit funds, and monitor the position over time.

That sounds simple because the transaction flow is simple. The hard part is everything around it.

The manual workflow behind one “easy” deposit

A stablecoin holder doing this properly has to make several judgment calls:

Pick the chain Gas costs, ecosystem depth, and protocol quality differ by network.

Pick the stablecoin Not all stablecoins carry the same issuer, collateral, or liquidity profile.

Pick the protocol A familiar brand name helps, but it doesn't replace checking risk parameters and current conditions.

Watch yield changes DeFi rates move. A good venue this week may be mediocre later.

Reassess risk Governance changes, liquidity shifts, and market stress can alter the safety profile fast.

This is why many first-time users either freeze and do nothing or swing too far in the other direction and over-optimize for headline yield.

Cash management needs active judgment

In traditional markets, large cash pools don't become useful just because they exist. Commentary around record cash balances makes this point clearly. Total U.S. money market fund assets reached $7.87 trillion on June 10, 2026, but that “dry powder” isn't guaranteed to rescue risk assets, according to this discussion of money market cash on the sidelines. Capital only matters when someone actively allocates it.

The same logic applies to stablecoins. Holding cash-like assets gives you flexibility. It doesn't automatically produce a good outcome. You still need a view on where to park funds, when to move them, and when to stay conservative.

A pile of liquid capital is not a strategy. It's raw material for a strategy.

What usually works for beginners

Start with a small amount: Learn the mechanics before scaling.

Use simple protocols: Cash management and experimentation shouldn't happen in the same transaction.

Favor accessibility: If you might need funds soon, avoid structures that complicate exits.

Review positions regularly: Even conservative DeFi positions need periodic attention.

Manual money market management in DeFi can work well. Plenty of experienced users prefer it. But for most professionals, the issue isn't whether they can make a deposit. It's whether they want to keep doing the research, monitoring, and rotation every week.

Automating Your Yield Strategy with Yield Seeker

That research burden is where automation becomes compelling. Not because users are lazy, but because the work is repetitive and easy to get wrong when life gets busy.

A good automated system applies the same discipline a serious operator would use manually. It watches available venues, compares risk-adjusted opportunities, and adjusts allocations without requiring the user to live inside dashboards and Discord channels.

FINRA notes that money market funds are designed for stability, but investors often chase yield without fully weighing the opportunity cost when rates may fall, as explained in FINRA's money market funds overview. That observation translates cleanly to DeFi. Chasing the highest visible rate is rarely the same as managing cash well.

What automation should actually do

The bar for a useful platform is higher than “shows APYs.”

It should help with:

Continuous monitoring: Markets change faster than most users can track manually.

Risk-aware allocation: Yield matters, but not without context around protocol quality and liquidity.

Rebalancing: Capital should move when the trade-off between safety and return changes.

Usability: A cash strategy people can understand is better than a black box they abandon.

If you want a deeper look at that logic, AI yield optimization is worth reading because it focuses on how automated systems can reduce decision fatigue while keeping strategies adaptive.

Why this matters for stablecoin holders

The best use of automation isn't replacing judgment. It's encoding judgment into a repeatable process.

That's especially relevant for stablecoins, where the goal often isn't maximum upside. It's keeping capital productive without turning yield collection into a second job. In that sense, automated DeFi money market strategy looks a lot like professional treasury management. Set clear constraints, monitor continuously, rotate when needed, and keep liquidity usable.

If you're holding USDC and want a simpler way to put idle stablecoins to work, Yield Seeker offers an AI-powered approach to automated, risk-aware DeFi yield. You can start with a small deposit, keep funds accessible, and let the platform handle the ongoing monitoring and allocation work that usually makes money market-style stablecoin strategies feel harder than they should.