You’re probably in the same spot as a lot of stablecoin holders right now. You see DeFi vaults, lending markets, and automated yield strategies offering returns that look meaningfully better than idle USDC, but you also assume there has to be a catch.

There is a catch. The yield is real, but the safety depends on a mechanism commonly misunderstood.

That mechanism is overcollateralized borrowing.

If you want to understand why automated stablecoin yield farming can be safer than it first appears, this is the concept to learn. It’s the buffer that lets strangers borrow on-chain without a bank, a credit score, or a collections team. It’s also the reason many DeFi strategies can function with rules instead of trust.

Why High DeFi Yields Have a Hidden Safety Net

DeFi's initial appeal often stems from its upsides. Higher yield. Faster settlement. No paperwork. No lockups on some platforms. Then the skepticism kicks in. If this is all so efficient, why doesn’t it blow up immediately?

The answer is that many of the core systems don’t start with trust. They start with excess collateral.

A simple analogy helps. In traditional finance, lenders reduce risk by asking for a cushion. Mortgages have down payments. Securities deals use credit enhancement. Asset-backed products often include extra protection so losses have to chew through a buffer before investors get hit. In that sense, overcollateralization didn’t start in crypto at all.

According to FinchTrade’s overview of over-collateralization, the concept has long been standard in asset-backed securities, and the 2008 Global Financial Crisis showed its limits when subprime mortgage-backed securities with 105-110% ratios still failed. That failure pushed finance toward much higher buffers. DeFi learned from that playbook and generally starts with stricter requirements.

Why this matters for your money

When a DeFi borrower wants cash-like liquidity, they usually can’t just post minimal collateral and hope for the best. They have to lock up more value than they borrow.

That does two things:

It protects the lender: if markets move, there’s still a recovery path.

It protects the protocol: the system doesn’t depend on courts, collections, or identity checks.

It protects the yield opportunity: stablecoin depositors can earn because the borrower is paying for access to liquidity, backed by assets already on-chain.

Practical rule: In DeFi, “high yield” isn’t automatically a red flag. The better question is what risk control makes that yield possible.

Why the safety net feels invisible

The reason people miss this is that good infrastructure fades into the background. If you deposit stablecoins into a lending market or into an automated strategy built on top of one, you don’t always see the borrower on the other side posting more value than they take out.

But that’s the core deal.

Without overcollateralized lending, a lot of stablecoin yield would look much riskier, because the system would have to rely far more heavily on unsecured credit assumptions. With it, DeFi can replace credit committees with transparent thresholds and automated enforcement.

That doesn’t make the system risk-free. It makes the risk legible.

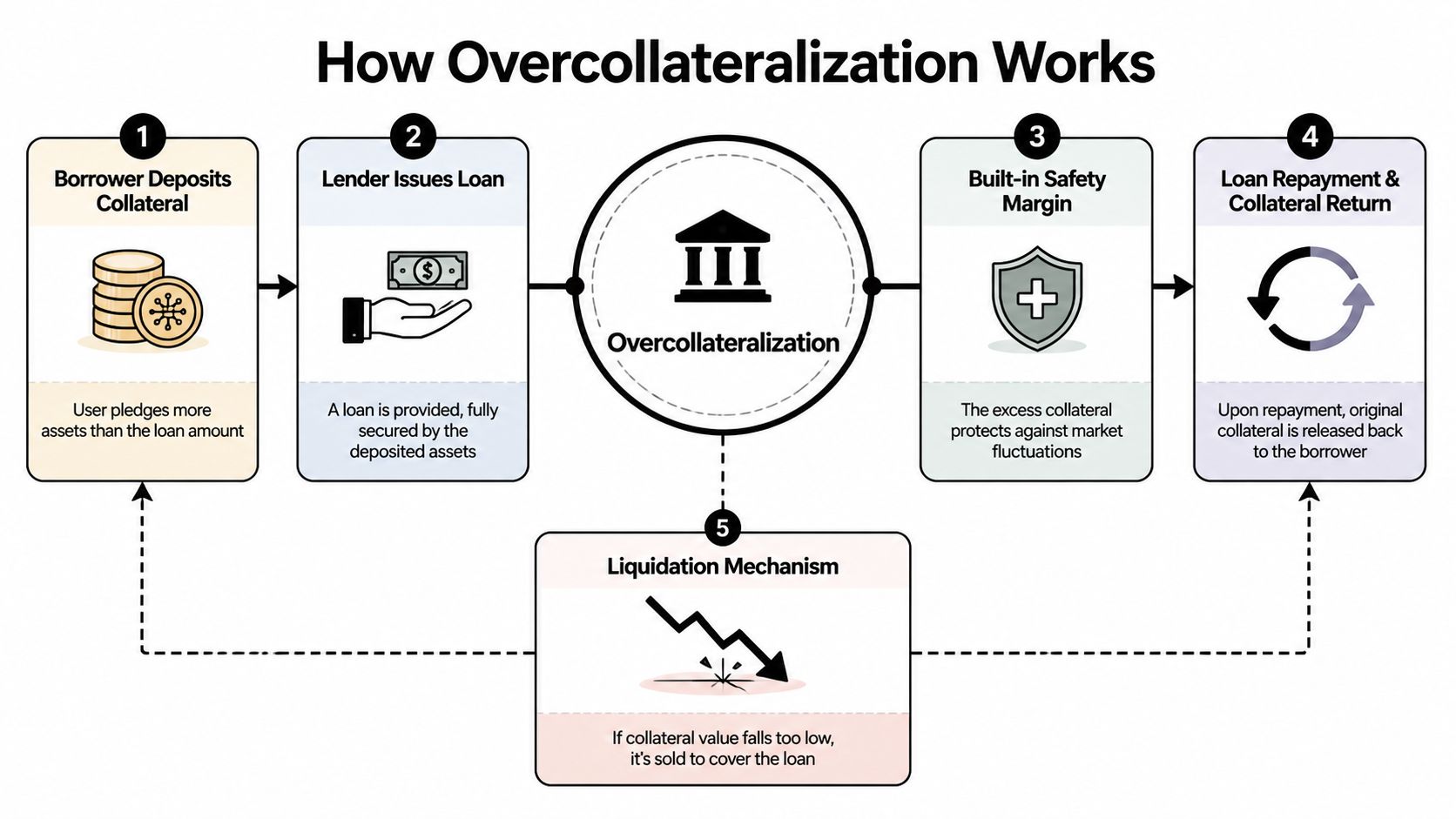

How Overcollateralization Actually Works

A borrower locks crypto into a protocol, then borrows less than that collateral is worth. That gap is the safety margin. It is the reason stablecoin yield can exist on-chain without relying on unsecured credit.

For someone depositing into an automated yield strategy, this matters more than the jargon. Your yield is often funded by borrowers paying to access liquidity, and those borrowers usually had to post more value than they took out. That extra collateral is the first loss absorber. It is a big part of why systems like DeFi lending markets can support stablecoin returns in a way that is more structured than it first appears.

The three numbers that matter

Protocols surface a lot of metrics, but three drive the risk.

Loan-to-Value or LTV

This tells you how much a user can borrow against posted collateral. DeFi protocols often set different LTV limits depending on the asset, as outlined in CWallet’s overview of overcollateralization in crypto lending. Lower LTV gives the position more room to survive volatility. Higher LTV uses capital more efficiently, but the liquidation buffer gets thinner.Liquidation threshold

This is the point where the protocol no longer considers the loan safe enough. If collateral value drops or debt grows relative to that threshold, the position becomes eligible for liquidation.Health factor

This is the live risk score most users watch in the dashboard. It compresses collateral value, debt, and protocol parameters into one number. Higher means more breathing room. Lower means a smaller market move can force a sale.

What happens when markets move

Take a common setup. A user deposits ETH and borrows a stablecoin against it.

If ETH goes up, the loan usually gets safer. If ETH drops, the buffer shrinks. Once the position crosses the protocol’s risk limit, third-party liquidators can repay part of the debt and buy the collateral at a discount. That incentive keeps the system solvent without a credit team calling borrowers one by one.

This is the part many depositors never see. The yield side feels simple, but under the hood the protocol is constantly checking whether every loan still has enough backing.

Liquidation is the enforcement mechanism that keeps lender capital protected when prices move fast.

Why the trade-off matters

Overcollateralization is a compromise between safety and capital efficiency. Post more collateral, and the system gets a wider buffer. Borrow more aggressively, and capital use improves, but liquidation risk rises quickly.

For a busy operator or treasury manager, the practical read is straightforward:

Term | What it means for you |

|---|---|

Higher collateral buffer | More safety, less borrowing power |

Higher LTV usage | More efficiency, more liquidation risk |

Falling health factor | You may need to add collateral, repay debt, or cut exposure |

That trade-off is why automated stablecoin strategies can be safer than they look at first glance, but never risk-free. The income comes from borrowers using on-chain liquidity. The protection comes from the fact that they had to overpost assets before they could borrow in the first place.

Overcollateralization in DeFi Lending Markets

The cleanest place to see this mechanism in action is a lending market.

On major platforms like Aave and Compound, it’s common to see collateralization ratios of 150-200%, and that model became a cornerstone of DeFi during 2018-2020. It has since scaled into a market where overcollateralized loans account for over 90% of lending activity, with DeFi reaching over $100 billion in TVL peaks in 2024, according to Amberdata’s analysis of institutional DeFi lending.

A concrete borrowing example

Here’s the basic shape of a trade.

You deposit ETH as collateral. You borrow USDC against it. You keep ownership exposure to ETH, but access stablecoin liquidity without selling. That borrowed USDC might be used for working capital, market making, treasury management, or a yield strategy elsewhere on-chain.

A common setup looks like this:

Collateral first: you post more value than you borrow

Stablecoin second: the borrowed asset is often USDC, DAI, or another stable asset

Buffer always: the extra collateral absorbs normal market swings

For a quick background on the moving parts, this guide to DeFi lending mechanics is a useful companion.

Why different assets get different treatment

Not all collateral is equal.

A protocol may allow a relatively stronger borrowing capacity against one asset and a lower one against another. The logic is straightforward. Some assets trade with high liquidity and move less violently. Others gap fast, especially during stress. The more volatile the collateral, the more conservative the protocol needs to be.

That’s what makes trustless lending possible. The system doesn’t ask whether you’re a good borrower. It asks whether your posted collateral can cover the debt if prices move.

A short walkthrough helps if you want to see this in action:

What works and what doesn’t

What works is using lending markets for liquidity without forced selling. That’s valuable if you want stablecoins now but don’t want to dispose of long-term crypto holdings.

What doesn’t work is borrowing near the maximum just because the app lets you. A position can look efficient on the way up and fragile on the first hard down move. In practice, the strongest users leave room for volatility and treat the borrow limit as a ceiling, not a target.

Powering Crypto-Backed Stablecoins Like DAI

You deposit ETH, mint DAI against it, and put that DAI to work in a yield strategy. The yield only makes sense if the stablecoin itself has a credible safety buffer underneath it.

That buffer is overcollateralization.

How minting differs from borrowing

A lending market matches borrowers with an existing pool of capital. A crypto-backed stablecoin system such as Maker works differently. You lock collateral in a vault and mint new DAI against that position.

For anyone farming stablecoin yield, that difference matters. The stablecoin is not coming from a bank account or a centralized issuer’s balance sheet. It is being created on-chain against excess collateral, with rules that are visible and enforced automatically.

According to Frontiers in Blockchain’s analysis of overcollateralized stablecoins, DAI uses collateral requirements above the value of the debt, including a 150% ratio for certain vault types. That surplus is what gives the system room to absorb price moves without immediately putting every position underwater.

If you want the portfolio context, this guide to what stablecoins do in DeFi portfolios is a useful companion.

Why this structure matters for yield

For a yield farmer, DAI is more than a dollar substitute. It is often the base asset that gets deployed into lending pools, market-neutral strategies, and automated vaults. If the minting system behind it is weak, the yield on top is built on soft ground.

Overcollateralization is what makes the stack investable in the first place. Volatile collateral sits at the base. A conservatively issued stablecoin sits above it. Yield strategies sit on top of that. The farther you are from the collateral engine, the easier it is to forget that the whole structure still depends on disciplined collateral ratios and a liquidation process that works during stress.

That is also why teams responsible for managing self-custodial control for treasury pay close attention to collateral design, not just yield screens. The safety model starts below the strategy layer.

Why DAI remains the reference point

DAI is still the canonical example because it showed that crypto-backed issuance can survive real volatility, recover, and continue operating. The same review notes that Maker and DAI kept evolving after the 2020 stress events and grew into a system used at meaningful scale across DeFi.

The practical takeaway is straightforward. Overcollateralized stablecoins are not safe because crypto is stable. They are safer because the system demands extra backing, monitors positions continuously, and closes weak ones before losses spread to the peg.

That is the hidden safety net behind a lot of automated stablecoin yield. Without it, the yields look attractive and the risk is badly misunderstood.

Understanding Liquidation Risks and Hidden Costs

The marketing version of overcollateralized borrowing sounds clean. Post collateral, borrow stablecoins, keep exposure, earn yield.

The lived version has rough edges. Liquidation is one of them.

What liquidation actually feels like

If your collateral drops too far, the protocol can sell part or all of it to repay the debt. You don’t just lose optionality. You often lose assets at the worst possible time, during a fast market drawdown when prices are already under pressure.

That’s why experienced users talk less about borrow limits and more about survival ranges. The important question isn’t “How much can I borrow?” It’s “How much volatility can this position survive without forcing a sale?”

During broad market stress, many borrowers hit those thresholds around the same time. That can create a chain reaction where falling prices trigger liquidations, and liquidations add more selling pressure. The system may still work as designed, but your outcome can still be painful.

The tax issue most people miss

One of the least discussed costs is tax.

According to Coinmetro’s glossary entry on over-collateralization, taking an overcollateralized crypto loan in the US isn’t a taxable event at inception, but liquidation can be. The same source notes that 28% of DeFi liquidations led to unexpected tax bills for users in 2025.

That matters because a forced sale can trigger capital gains on appreciated collateral even though the liquidation itself feels like a loss of control, not a profit-taking decision.

Often overlooked: A liquidation can hurt twice. First through lost collateral, then through taxes on the forced sale.

Operational risk still matters

The collateral model can be sound and your setup can still fail if your operational controls are weak. Treasury managers and serious users should think about wallet access, approval flows, and monitoring as part of risk management, not as separate admin work.

For teams handling meaningful balances, this guide on managing self-custodial control for treasury is worth reading because bad key management can undo all the elegance of a good collateral model.

A practical checklist helps:

Keep larger buffers than the UI minimums: the minimum is a protocol survival line, not your personal comfort zone.

Watch taxable disposals: liquidation accounting can become messy quickly.

Reduce fragmented oversight: if collateral sits in one place and debt in another, it’s easier to miss risk buildup.

Respect correlation risk: collateral that falls when the rest of your strategy also weakens deserves extra caution.

The biggest mistake isn’t using overcollateralized borrowing. It’s assuming the buffer means you can stop paying attention.

How Yield Seeker Automates Safety and Maximizes Yield

Overcollateralization makes DeFi lending and stablecoin strategies possible. It doesn’t make them effortless.

That gap between “possible” and “manageable” is where most users struggle. Monitoring collateral health across protocols, deciding when to rotate capital, avoiding liquidation bands, and comparing risk-adjusted yield on stablecoins takes time. Busy professionals usually don’t have that time, and beginners often don’t have the context.

The problem with manual management

Manual yield farming tends to fail in predictable ways.

One person chases the top headline APY and ignores how the underlying protocol handles collateral risk. Another person opens safe positions but forgets to monitor them consistently. Treasury teams often have the opposite problem. They care about control and auditability, but fragmented dashboards make simple decisions slower than they should be.

What works better is automation with guardrails.

A risk-aware system can monitor positions continuously, react faster than a human checking a dashboard between meetings, and favor protocols whose collateral frameworks are transparent and battle-tested. That’s a different mindset from pure yield chasing. The objective isn’t just earning more. It’s earning without introducing sloppy liquidation exposure.

Where automation changes the experience

The best use of automation in this category is narrow and practical:

Position monitoring: watch health metrics continuously instead of occasionally

Capital routing: move stablecoins where the opportunity is attractive without ignoring risk structure

Rebalancing discipline: reduce the odds that inaction becomes the reason a safe-looking setup turns fragile

For readers evaluating automated approaches, this look at secure yield automation is a helpful reference point.

Good automation doesn’t remove risk. It removes neglected risk.

Why this matters for stablecoin holders

Stablecoin yield is appealing because it promises cash-like usability with on-chain returns. But the value isn’t just the headline number. The value is getting that return while keeping funds accessible and keeping risk understandable.

That’s why overcollateralized infrastructure matters so much. It gives automation something solid to build on. If the underlying lending and minting systems had weak collateral standards, an AI layer on top wouldn’t fix the problem. If the collateral model is strong, automation can help users interact with it more safely and consistently.

That’s the practical takeaway. You don’t need to become a full-time DeFi risk analyst to benefit from on-chain yield. You do need to understand the safety net under the strategy, and you want systems that manage the details with more discipline than a casual manual workflow.

Yield Seeker helps stablecoin holders put this into practice. If you want automated, risk-aware yield on USDC without manually tracking every protocol and position, explore Yield Seeker to see how AI-guided allocation can help you stay productive, liquid, and more disciplined on-chain.