You swap into a stablecoin vault, approve the transaction, and the interface says you should receive one amount. A moment later, the transaction confirms and you got less. Not dramatically less. Just enough that you shrug and move on.

That gap is often slippage. In DeFi, it's one of the easiest costs to underestimate because it rarely arrives as a line item labeled “you lost money here.”

If you hold stablecoins and move capital between pools, vaults, and strategies, slippage isn't a side issue. It directly affects your net yield. The mistake often made is treating it like a minor trading annoyance. It's better to think of it as an execution cost that sits between your strategy and your actual wallet balance.

The Hidden Cost of Your Last DeFi Trade

You move $20,000 from a stablecoin position into a new vault. The quote looks fine. The gas is acceptable. The APY still clears your hurdle. Then the transaction lands, and your starting balance is lower than the screen suggested. Nothing broke. You just paid an execution cost that many dashboards barely surface.

That hidden cost is slippage. It sits between the strategy you planned and the balance that reaches your wallet.

In DeFi, it is common to focus on the visible numbers: yield, gas, protocol fees, and risk. Execution quality gets less attention, even though it decides how much capital enters or exits a position. If your trade clears at a worse price than expected, your real return starts lower from the first block.

Slippage matters because it is not linear in practice. A small trade in a deep pool may barely move the outcome. A larger trade, or a strategy that rebalances often, can lose much more than expected because the cost rises faster as you push against available liquidity. If you need a quick refresher on why pool depth matters, this guide on what liquidity means in crypto helps frame the problem.

Why this hits DeFi strategies harder

A single swap can absorb a small amount of slippage and still be acceptable. Automated strategies are different. They enter, rebalance, harvest, rotate, and exit. Each action adds another point where execution can drift from the quote.

That turns slippage from a trading annoyance into an infrastructure problem.

For stablecoin users, that distinction matters. A strategy can look safe because the assets are stable and the yield source is familiar, yet repeated execution drag can gradually pull net returns down. The wallet only sees the final result.

Three ideas that are easy to confuse

It is easy to confuse these three concepts:

Market movement: the price changes while your transaction is pending

Price impact: your own order pushes the pool price against you

Slippage: the final gap between the quote you saw and the execution you got

They are related, but they are not the same. If you mix them together, you cannot diagnose the correct fix. Smaller order size solves one problem. Better routing solves another. Better timing, batching, or automation may solve a third.

That last point is where this gets interesting. Slippage is often treated like weather. Something annoying, but unavoidable. In practice, much of it is an execution design problem. Trade size, route selection, timing, and whether a strategy acts mechanically or adaptively all change the outcome. That is why modern execution tooling, including AI agents, is becoming part of yield infrastructure. The goal is not just to find yield. It is to deliver more of that yield to the wallet after real market conditions and trade costs.

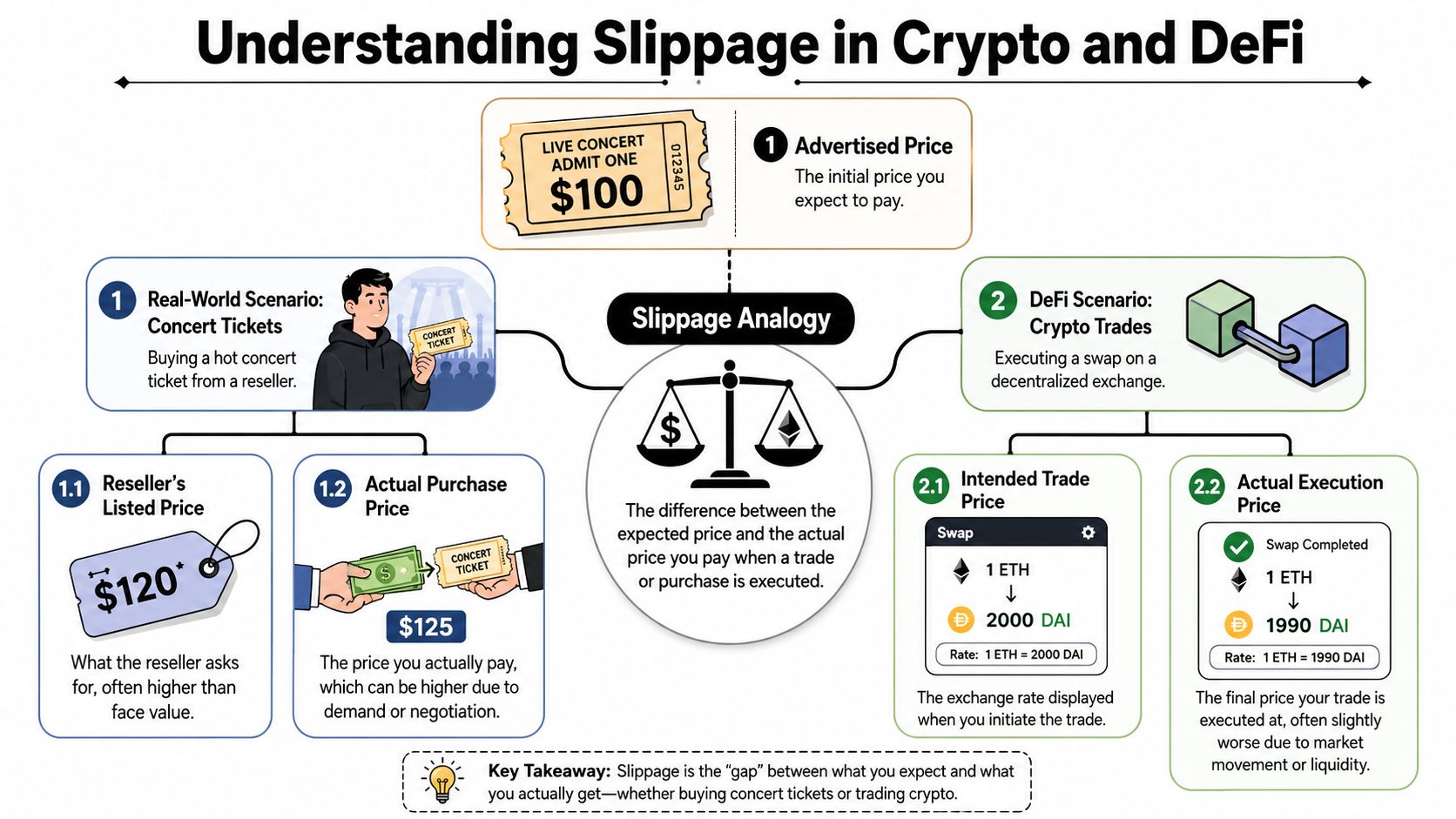

Understanding Slippage in Crypto and DeFi

You submit a swap at one price, confirm the transaction, and receive a different one. That gap is slippage. In DeFi, the quote is only a snapshot. Your final fill depends on what the market looked like by the time your transaction executed.

Crypto makes this easy to miss because the interface often shows a clean number up front. Under the surface, your order is moving through a live system where liquidity can shift, routes can change, and other traders can reach the pool before you do. On a DEX, that gap can come from pool movement while your transaction is pending, from your order being large relative to available liquidity, or from an inefficient path through the market. If you want a clearer model for the first part, it helps to understand what liquidity means in crypto.

The plain-English definition

In crypto and DeFi, slippage is the difference between the price you expected and the price your trade got.

Platforms usually let you set a slippage tolerance, often as a small percentage band. That setting does not improve your execution. It sets the maximum drift you are willing to accept before the trade reverts. A wider tolerance increases the chance that a transaction goes through. It also increases the chance that you accept a materially worse fill.

That distinction matters for wallet outcomes. Many users treat slippage tolerance like a convenience setting. It is closer to a risk setting.

Slippage can be good or bad

Slippage is often treated as automatically negative because bad fills are painful and visible. But the term itself is neutral. It only describes the difference between the quoted price and the execution price.

Negative slippage means you got a worse price than expected.

Positive slippage means you got a better price than expected.

Execution data can move in both directions. FXCM's published execution statistics show both positive and negative slippage across order types, and the distribution changes based on how the order is structured, according to FXCM's slippage statistics page.

The practical lesson is simple. Slippage is part of execution quality, not just a trading fee you tack on afterward.

Why DeFi users should care

For a one-off swap, slippage may look small. For a strategy that deposits, rebalances, rotates incentives, harvests, and exits, it behaves more like hidden infrastructure drag.

That is why the cost is often non-linear. A trade that is twice as large is not always twice as expensive to execute. Once you start pushing into thinner liquidity, the pool has to give you progressively worse prices to fill the order. The same thing happens when an automated yield strategy repeats this process across many transactions. A few basis points here and there can erase a surprising share of the advertised return.

This is the part basic advice misses. "Use limit orders" is helpful in some venues, but it does not solve the broader DeFi problem of timing, routing, sizing, and repeated execution. Better results often come from better trade design and better automation. That is why modern execution tooling, including AI agents, is becoming part of yield infrastructure. The goal is not only to find yield, but to keep more of it after real trading conditions hit your wallet.

A quote is an estimate. Your wallet records the fill.

The Technical Causes of Slippage You Must Know

You approve a swap, the quote looks fine, and the final fill still comes back worse. That gap usually comes from market structure, not a random glitch. Slippage is what happens when your order meets real liquidity, real time delays, and a pricing mechanism that changes as you trade.

In execution analysis, traders often measure this gap against the market's starting reference price, such as the midpoint between the best bid and ask. A concise overview of that approach, along with the role of liquidity, volatility, and order flow, appears in this market microstructure discussion of slippage.

Liquidity depth changes everything

Start with liquidity depth. If the market only offers a small amount at the quoted price, your order has to reach into worse prices to get fully filled. A shallow pool or thin order book works like a small stack of inventory on a shelf. The first units are cheap. The next units cost more because you are clearing out the easy liquidity first.

That is why slippage is non-linear. A trade that is 5 times larger can create far more than 5 times the price impact once it pushes past the top layer of available liquidity. For DeFi users running large entries, exits, or automated reallocations, this is an infrastructure problem, not a minor nuisance.

AMM design builds price impact into the trade itself

On DEXs, the pricing model adds another layer. Automated market makers reprice the pool as your swap changes the token balances. Your order is not just accepting a price. It is reshaping the pool and getting a new price quote with each increment of size.

That is why the curve matters so much. In a balanced, deep pool, a modest trade may barely move the price. In a smaller or more imbalanced pool, the same trade can slide quickly into worse execution. If you want a refresher on that mechanism, this guide to how automated market makers price trades is a useful reference.

Volatility and latency create quote decay

Price impact is only one part of the story. Time matters too.

Between signing a transaction and getting it included onchain, the market can move. If blockspace is crowded or trading activity spikes, the quote you saw at submission can be stale by the time validators process it. The result feels confusing because the interface showed one number, but your wallet settles at another.

For active strategies, that delay is expensive. A vault that rebalances once in a while may absorb it. A strategy that rotates often, harvests rewards, and redeploys capital keeps paying this timing tax over and over.

Slippage is also commonly confused with front-running

The distinction matters because the fix depends on the cause.

Slippage is the difference between the price you expected and the price you received. Front-running and sandwich attacks are specific transaction ordering attacks that can worsen that outcome, but they are not the only explanation. Thin liquidity, large trade size, and ordinary market movement can produce slippage even in the absence of any adversarial actor.

That diagnosis changes what you do next. If the problem is pool depth, you adjust sizing or route selection. If the problem is latency, you improve timing and execution logic. If the problem is adversarial ordering, you need protection in the transaction path. Getting this right matters more for automated yield systems than for one-off swaps, because repeated execution turns small mistakes in trade design into persistent drag on returns.

How Slippage Silently Reduces Your Yield

You can pick the right pool, time the market well enough, and still end up with less yield than the dashboard suggested.

The missing piece is execution. Yield is not just the rate a strategy advertises. It is the return left after your capital enters, exits, rebalances, harvests, and redeploys across real liquidity. Every one of those steps can shave value off the result.

The loss usually hides in the workflow

A stablecoin strategy can look boring on the surface. Deposit into one pool. Later rotate into another with a better rate. Claim rewards. Convert back to the base asset. None of that feels like active trading, but the market still charges you for each move through price impact and execution friction.

That is why slippage becomes yield drag, not just a trader's annoyance.

The drag is easy to miss because it rarely shows up as a line item. You see it in a slightly worse entry price, a weaker rebalance, or a smaller amount returned to the wallet at exit. One event may seem trivial. Repeated across an automated strategy, it starts to act like a slow leak in a pipe.

A better question is not "What APY does this strategy show?" It is "What return survives after the strategy does all the work required to earn it?"

Why larger moves get disproportionately worse

Trade size matters more than many users expect. It is a common assumption that a trade ten times larger creates roughly ten times the cost. In practice, slippage often gets worse faster than trade size because larger orders push further into available liquidity and hit less favorable pricing at each step, as explained in Quant Journey's analysis of slippage as a non-linear execution cost.

That changes how you should evaluate yield systems.

A small rebalance may pass through a pool with limited damage. A treasury-sized rebalance through the same route can produce a meaningfully different result, even if both trades target low-volatility assets. The problem is not only direction. It is market depth.

This is why execution is an infrastructure problem. Once capital reaches a certain size, "just swap and redeploy" stops being a harmless operational step. Routing, sizing, timing, and chunking start to determine whether the strategy's gross yield can survive contact with the market.

Why this hits automated strategies harder than manual users

Manual users usually notice slippage on entry and exit. Automated yield systems can pay it on every maintenance action.

A vault that rebalances weekly has one slippage profile. A strategy that harvests, swaps rewards, reallocates across venues, and responds to small yield changes can create many more moments where value leaks out. The strategy may be correct on allocation and still underperform in net terms because it trades too often or too bluntly.

That is why execution logic deserves the same attention as asset selection. Teams that study gas-efficient allocation design already understand part of this idea. Operational costs shape outcomes. Slippage works the same way, except the cost is less visible and often less linear.

A useful review framework looks like this:

Question | Why it matters |

|---|---|

Does the system check liquidity before trading? | A strong allocation can still produce weak net returns if the route cannot absorb the size efficiently. |

Does it size trades relative to pool depth? | Larger moves can trigger disproportionately worse fills. |

Does it rebalance only when expected gain exceeds execution cost? | Frequent optimization can turn into churn. |

Does it track realized execution, not just quoted prices? | Quotes show intent. Wallet outcomes show performance. |

Modern execution tools, including AI agents, are being built to handle exactly this kind of problem. Not because slippage is mysterious, but because monitoring many venues, adjusting trade size, choosing routes, and deciding when not to trade is hard to do well by hand and hard to do consistently with static rules.

For yield seekers, that distinction matters directly to the wallet. A strategy can win on paper and still lose in practice if its execution layer treats slippage like a minor trading fee instead of a recurring system cost.

Practical Tactics to Minimize Slippage

You approve a rebalance that looks harmless. The quoted price looks fine, the expected yield improvement looks fine, and the transaction confirms. Later, the gain is smaller than expected. Nothing obviously broke. The loss came from execution.

That is why slippage control needs to be part of the trade plan, especially for larger positions and automated strategies. Small swaps can absorb a bit of pricing friction. Bigger moves often cannot. Slippage rises with size in a way that is often uneven, which means doubling trade size can do more than double the damage to realized return.

Start with the controls in front of you

Your first line of defense is slippage tolerance. It sets the worst fill you are willing to accept before a trade reverts. That setting is a guardrail. It does not improve your price by itself.

Set it too tight and the trade may fail in normal market movement. Set it too loose and you give the protocol permission to execute at a much worse price than the quote suggested. The Coin Course's slippage guide is a useful primer if you want a quick reference on how traders use that setting in practice.

Order type matters too. Market orders work like telling a cashier, “fill the cart at whatever the shelf price becomes while I walk to the register.” That is fine in deep, calm markets. In thin or fast markets, it is expensive. Limit orders give you tighter control over price and are often the better choice when execution quality matters more than immediate completion, as discussed in LiteFinance's slippage explainer.

Read the pool before you trade into it

A quote is not a promise. It is a snapshot of what the pool can offer at that moment and size.

For DeFi, that means checking whether your order is large relative to available liquidity. A shallow pool can look cheap for the first few dollars and expensive for the rest of the trade. That is the part many users miss. Slippage is not just “a bit worse than expected.” It often behaves like a curve. The deeper you push into the pool, the faster the price moves against you.

A few habits help:

Check pool depth against your trade size. If your order is a meaningful share of nearby liquidity, expect the fill to worsen quickly.

Avoid unstable windows. Fast markets make quotes stale faster and increase the odds of poor execution.

Be more cautious with thin pairs. A process that works on major stablecoin routes can fail on lower-volume assets.

Pause if the trade is optional. Waiting is sometimes the cheapest execution decision available.

One sentence can save a lot of money here. If the market looks messy, your quote probably is too.

Split trades when size starts to matter

For larger swaps, order splitting is often the simplest practical fix. Instead of forcing one large trade through the curve, break it into smaller pieces and compare the realized fill.

The logic is straightforward. Automated market makers reprice as you consume liquidity. Smaller trades disturb the pool less at each step, which can reduce total slippage and sometimes improve routing options. You do pay for that with extra operational work and, on some chains, more gas. So this is not a universal rule. It is a sizing rule.

That tradeoff matters even more for yield automation. A stablecoin rotation can look like routine maintenance at the strategy layer while acting like a large market order at the execution layer. If a system rebalances frequently and in big chunks, slippage can erase a meaningful share of the yield it was trying to capture.

Use execution tools, not just opportunity dashboards

A yield dashboard answers one question: where is the return right now?

Execution tools answer the harder question: can you get into that position cheaply enough for the move to still make sense after routing, price impact, and gas?

That distinction is where many automated strategies win or lose. A strong system checks liquidity before trading, sizes orders to market depth, and skips rebalances when the expected benefit is too small to cover execution cost. If you want a related framework, this guide to gas-efficient allocation design helps show why gas and slippage should be evaluated together, not as separate line items.

Some users manage this manually with aggregators and careful timing. Others use platforms that combine monitoring and reallocation logic. Yield Seeker is one example. It uses an AI agent to monitor DeFi opportunities and allocate stablecoin capital in real time. The point is not convenience alone. The point is that execution quality is an infrastructure problem, and infrastructure is exactly what automated systems are built to handle.

A practical checklist before you confirm

Use this before any meaningful swap or rebalance:

Check the route. Default routing is not always the cheapest path in realized terms.

Set tolerance intentionally. Treat slippage tolerance as a loss limit, not a convenience setting.

Compare size to liquidity. Large trades deserve extra scrutiny because price impact often rises faster than expected.

Split the order if needed. Test whether smaller chunks improve the net result after gas.

Check whether the rebalance is worth doing at all. If the expected gain is marginal, execution cost can wipe it out.

Review realized execution afterward. Quotes are estimates. Wallet outcomes are the result that matters.

The goal is not to remove slippage entirely. The goal is to stop treating it like a minor trading fee when it behaves more like a hidden tax on size, frequency, and automation.

Thinking Beyond Slippage as a Trading Fee

You rebalance into a higher-yield pool, the dashboard says the move was smart, and a day later your net return is worse than if you had done nothing. That gap is often slippage, but not in the narrow sense of a one-off trading fee. It behaves more like execution drag across an entire system.

That distinction matters because slippage is rarely linear. A small swap in a deep pool may barely move the price. A larger rebalance, or a strategy that trades again and again, can lose much more than expected because price impact, routing quality, and timing all start interacting with each other. The result hits large positions and automated yield loops hardest.

A useful way to frame this comes from OANDA's explainer on slippage and execution risk, which describes slippage as an execution-risk problem shaped by liquidity, volatility, and delays between decision and fill. In DeFi, that same logic extends one layer deeper. Your strategy can be correct on paper and still underperform because the infrastructure moving capital is inefficient.

The mental model that helps

It is more effective to treat slippage as execution quality.

A router works like a shipping network. If the route is inefficient, the package still arrives, but it costs more and takes longer. DeFi capital movement has the same problem. The wallet only sees the final amount, yet that amount depends on pool depth, route selection, block timing, and whether the trade size itself changes the market while the order is being filled.

That perspective changes how you judge a strategy:

Trade size matters more than many users expect. Slippage often rises faster than trade size, which is why large reallocations can erase a meaningful share of quoted yield.

Frequency matters too. A strategy that rebalances often may leak value even if each individual trade looks acceptable.

Automation needs judgment, not just speed. An automated system should decide whether a rebalance is worth executing after expected slippage and gas, not merely chase the highest displayed APY.

Infrastructure becomes part of performance. Routing logic, timing rules, and execution controls affect wallet outcomes just as much as headline yield does.

This is why slippage deserves more attention from anyone running stablecoin strategies, DAO treasury operations, or vault logic. Gross yield is the top line. Execution quality decides how much of it you keep.

A useful outside reference

If you want a trading-focused companion read, The Coin Course's slippage guide explains the mechanics clearly from the market side.

The broader takeaway is simple. Slippage is not just a fee to tolerate. It is a system cost to control. Once you view it that way, tools that monitor routes, timing, and rebalance decisions start to look less like convenience features and more like necessary infrastructure for protecting net yield.

If you want a simpler way to manage stablecoin yield without manually tracking every pool, route, and rebalance, Yield Seeker lets you deposit USDC on Base and use an AI agent to monitor and allocate capital across DeFi opportunities in real time. It is built for users who care about net returns, not just headline APYs.