You're probably in one of two camps right now. You're holding USDC or another dollar-pegged asset and you don't want it sitting idle, or you've looked at DeFi yield options and backed away because every dashboard looks like a cockpit.

That hesitation is rational. Stable yield sounds simple. Deposit stablecoins, earn a return, move on. In practice, the hard part isn't finding yield. It's figuring out whether the yield is real, whether it will still be there next week, and what hidden risk you're taking to earn it.

Many individuals get this backwards. They start with the APY and ask whether it's attractive. Experienced operators start with the mechanism and ask whether the return is durable. That one change in mindset filters out a lot of bad decisions.

The Promise and Problem of Earning Stable Yield

Stable yield appeals to a very specific need. You want crypto-native cash management. You want something more productive than leaving stablecoins idle, but less chaotic than chasing volatile tokens, farms using borrowed capital, or directional bets.

That's the promise. The problem is that DeFi rarely presents yield in a way that matches how professionals assess risk. Interfaces highlight headline returns. They often make it harder to see the moving parts underneath, such as who is paying, why they are paying, how quickly the rate can change, and what happens when market conditions tighten.

Why stable yield looks easier than it is

On the surface, stablecoins feel close to cash. That creates a dangerous mental shortcut. People assume the yield should behave like a savings rate or money market rate.

It usually doesn't.

In DeFi, getting to a sensible stable yield position takes work:

You need source-level clarity about whether yield comes from T-bills, borrower demand, trading fees, funding, or token incentives.

You need protocol judgment because two products can show similar rates while carrying very different contract, liquidity, and de-peg risk.

You need ongoing monitoring because a strategy that looked conservative on Monday can become thin, crowded, or subsidy-driven by Friday.

Practical rule: If you can't explain who is paying the yield and why they keep paying it, treat the number as temporary.

The opportunity is real. So is the operational burden. That's why stable yield shouldn't be framed as “easy passive income.” It's better understood as active risk selection on low-volatility assets.

For busy professionals, the core question isn't whether DeFi can generate stablecoin yield. It can. The key question is whether you want to do the screening and repositioning yourself, every week, across fragmented protocols and changing incentives.

What Stable Yield in DeFi Really Means

The word stable causes most of the confusion.

In traditional finance, people hear “stable yield” and think of a relatively predictable return tied to low-risk instruments. In DeFi, the term usually means the asset is stable relative to the dollar. It does not mean the yield itself is fixed, guaranteed, or risk-free.

Stable asset, variable income

That distinction matters. A dollar-pegged token can reduce price volatility compared with ETH or SOL, but the return on that token still depends on the engine producing it. If the engine changes, the yield changes.

A better analogy is a managed spread portfolio, not a savings account. You are collecting income from specific activities inside crypto or from reserve assets outside crypto. Those activities can be healthy and durable. They can also thin out quickly.

Spark's research makes this point clearly. It warns that stablecoin yields are only durable when they can be traced to identifiable income sources such as T-bills, lending interest, or funding rates. Otherwise, the headline return may come from emissions or other unsustainable incentives. The same research notes that yield-bearing stablecoins grew from under $1.5 billion in early 2024 to over $19 billion by late 2025 and highlights how realized yields can move sharply, citing Angle's stUSD as historically ranging from 6% to 25% before recently stabilizing around 8.5% (Spark's research on yield-bearing stablecoins).

The right way to read a high APY

When you see a strong stablecoin APY, don't ask only whether it's higher than alternatives. Ask these questions first:

Is the income identifiable? T-bills, borrower interest, trading fees, and funding are easier to underwrite than vague rewards.

Is the yield organic or subsidized? Token emissions can create a temporary optical boost.

Can it reprice fast? If the strategy depends on market demand, it can compress hard when demand changes.

What's absorbing losses? A reserve fund, overcollateralization model, or insurance mechanism matters, but only if it's real and understandable.

“Stable yield” often means controlled instability, not fixed income.

That sounds less comfortable, but it's more useful. Once you accept that stable yield is conditional rather than guaranteed, you start evaluating it the right way. You stop shopping for the highest number and start screening for the cleanest income source, the best structure, and the fastest exit if conditions deteriorate.

The Four Engines of DeFi Yield Generation

There are many wrappers and product labels in DeFi, but most stable yield comes from four underlying engines. If you understand these, you can usually see through the marketing.

Lending markets

This is the cleanest place to start. You deposit stablecoins into a lending protocol, borrowers take those assets, and you earn part of the interest they pay. Protocols like Aave made this model familiar, and the logic is straightforward.

The catch is that rates move with utilization and borrow demand. A lending market with active borrowing can offer solid yield. The same market can soften fast when borrowers leave or when a better venue pulls demand away. If you want a deeper breakdown of the mechanics, this guide to DeFi lending protocols is a useful companion.

Liquidity provision

This engine pays you for helping a market function. You deposit assets into a pool on a decentralized exchange, traders use that pool, and the protocol distributes a portion of trading fees to liquidity providers.

For stablecoin-heavy pairs, this can look conservative compared with volatile pairs. But “more conservative” isn't the same as simple. Pool composition, fee tier, pool depth, and temporary pricing dislocations all matter. If the pool includes a stablecoin that weakens or an asset that diverges, your realized outcome can disappoint even when fees look attractive on paper.

Here's a quick operating view:

Engine | Who pays | What moves the yield |

|---|---|---|

Lending | Borrowers | Utilization, borrow demand, liquidity conditions |

Liquidity provision | Traders | Volume, fee tier, pool composition |

Yield-bearing stablecoins | Reserve assets or protocol strategy | Reserve income, structure quality, redemption design |

Vaults and aggregators | Underlying strategies | Allocation logic, timing, and risk controls |

A useful macro point sits beneath all of this. A BIS working paper found that a $3.5 billion inflow into dollar-backed stablecoins can lower 3-month T-bill yields by about 4 basis points within 10 days, showing that stablecoin demand can mechanically affect the reserve assets backing many stable yield strategies (BIS working paper on stablecoins and T-bill yields).

That matters because some “onchain yield” is tightly linked to offchain reserve markets. It isn't isolated from external markets. Capital moving into stablecoins can change the pricing of the assets those structures rely on.

Later in the stack, it helps to see one visual explanation before comparing products:

Yield-bearing stablecoins and vaults

Some products package the strategy for you. A yield-bearing stablecoin may hold or route into income-producing assets and pass part of that income through the token structure. Vaults and aggregators go one step further by shifting capital across protocols to capture better opportunities.

This packaging is convenient, but it can hide complexity. The wrapper doesn't remove risk. It changes where the risk sits. You need to know whether the wrapper is earning from reserve assets, from lending, from market-neutral trading, or from incentives that may disappear.

The wrapper is not the strategy. It's just the interface.

That single sentence prevents a lot of mistakes.

Navigating the Hidden Risks of Chasing Yield

Most stable yield failures don't start with fraud. They start with a mismatch between what the user thought they owned and what the product did.

The risk people underestimate most

Yield volatility is the least dramatic risk, so it often gets ignored. That's a mistake. For many stablecoin strategies, the return is a spread trade. You're earning the difference between one rate and another. If that spread narrows, your return shrinks. If it inverts, the strategy can go negative.

Galaxy describes this clearly in its research on onchain yield. In a common DeFi lending loop, users supply stablecoins, borrow a volatile asset, sell it for more stablecoins, and earn only when the stablecoin lending APY exceeds the borrowing cost. The yield compresses or can turn negative when crypto borrow demand rises or liquidity falls (Galaxy research on the state of onchain yield).

That's the core instability behind many “stable” yields. The asset may hold its peg while the economics underneath it deteriorate.

The rest of the risk stack

A practical way to think about risk is to separate loss of principal, loss of liquidity, and loss of expected income.

Smart contract risk

If the code breaks, gets exploited, or behaves unexpectedly, funds can be impaired. Mitigate this by favoring battle-tested contracts and keeping exposure sized to the trust you place in the codebase.De-peg risk

A stablecoin can fail to hold its dollar reference. Even temporary de-pegs can force bad exits. Mitigate this by understanding redemption design, reserve composition, and whether the peg depends on confidence or direct convertibility.Protocol risk

Teams make poor decisions, governance can drift, and product design can fail under stress. Mitigate this by judging the operating culture, communication quality, and whether the mechanism still makes sense when incentives are stripped away.Liquidity and exit risk

You may be able to mark a position at one value and only exit at a worse one. Mitigate this by checking withdrawal paths before deposit size grows.

For a broader breakdown of common failure modes, this piece on yield farming risks is worth reading.

What experienced users do differently

They don't ask whether a product is safe in the abstract. They ask where it breaks first.

If the APY vanished tomorrow, would the product still be coherent?

That question exposes weak structures fast. If the answer is no, the yield likely depended on temporary incentives, reflexive demand, or fragile assumptions about liquidity.

Another habit matters. Skilled users treat monitoring as part of the strategy, not a separate admin task. In DeFi, risk often arrives as drift. A protocol doesn't fail in a single headline event. The reserve mix changes. Borrow conditions tighten. liquidity thins. Governance passes a parameter update. By the time the dashboard shows a problem, the edge may already be gone.

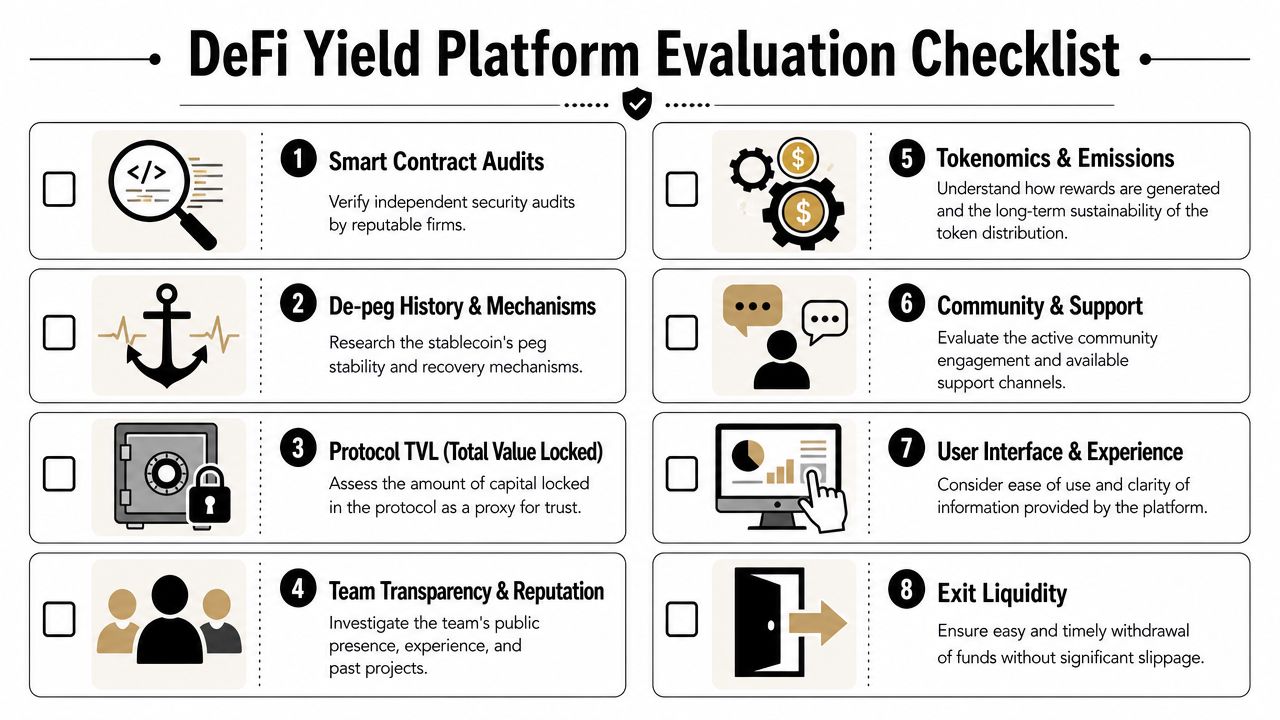

Your Checklist for Evaluating Yield Platforms

Most due diligence failures come from skipping basic questions because the interface feels polished. A clean app doesn't mean a clean strategy.

The questions that matter before deposit

Use this checklist before you move funds anywhere.

Where does the yield come from?

If the answer is vague, stop. You want identifiable income, not a rotating mix of incentives and marketing language.What exactly am I holding?

Is it a plain stablecoin, an LP token, a vault receipt, or a rebasing wrapper? Each changes your risk and exit path.How quickly can the return change?

Some strategies reprice continuously. That's fine if you expect it. It's dangerous if you assume the current rate is durable.

The questions that matter after deposit

The second layer is operational.

Can you exit cleanly?

Check whether funds remain accessible, whether there are queue delays, and whether leaving requires selling into thin liquidity.Has the protocol earned trust the hard way?

Audits help, but they aren't enough. Look for time in market, incident handling, and whether the team communicates clearly when conditions change.Do the incentives distort the product?

A protocol can look attractive because it is paying users to ignore the underlying economics. That rarely ages well.Is the interface transparent about strategy changes?

If allocations shift behind the scenes, you should be able to see where capital went and why.

A quick mental model helps:

If you can answer this clearly | You probably understand the product |

|---|---|

Who pays the yield | Income source is identifiable |

When yield drops | Repricing risk is visible |

How you exit | Liquidity path is clear |

What can impair principal | Risk is being priced consciously |

Working heuristic: Don't outsource judgment to APY. Use APY as the final check, not the first one.

That's how practitioners avoid most unforced errors. They make the product prove itself before they let the rate influence them.

The Hands-Off Approach with AI Automation

Manual yield management breaks down for the same reason manual portfolio ops break down anywhere else. The work compounds. You're tracking protocols, comparing rates, checking whether returns are organic, watching for parameter changes, and deciding when to rotate. That can be manageable with a small book and lots of time. It doesn't scale well for busy operators.

What automation should actually do

A useful AI workflow for stable yield isn't just “find the highest APY.” That would automate the wrong instinct. It should do four harder jobs:

Monitor markets continuously so yield compression or deteriorating conditions are caught early.

Screen opportunities against risk rules rather than rate alone.

Allocate dynamically when the relative trade-off between return, liquidity, and protocol quality changes.

Keep the user informed with an interface that explains positions instead of hiding them.

That's the logic behind newer tools in this category, including AI agent workflows for DeFi yield management. The attraction isn't novelty. It's reduced operational drag.

Where Yield Seeker fits

One example is Yield Seeker, which lets users deposit stablecoins on Base and have a personalized AI agent monitor and allocate capital across DeFi protocols in real time. The product is built around a simple operating model: low minimum entry, no lockups, no withdrawal fees, and a dashboard that shows balances and earnings without forcing users to juggle multiple apps.

That model makes sense for the exact problem stable yield creates. The challenge isn't access. It's maintaining a disciplined process after access. An AI-driven setup can automate parts of the checklist above, keep watching when you aren't, and reduce the temptation to chase every shiny rate change manually.

This doesn't remove risk. Nothing does. It changes how the risk is managed. Instead of relying on sporadic human attention, you use a system that can keep evaluating the same variables with more consistency than an individual can maintain on their own.

For professionals with treasury balances, creators holding stablecoin income, or investors who want exposure without a second job in protocol monitoring, that's the practical case for automation.

Conclusion Earning Smarter Not Harder in DeFi

Stable yield is real, but the label is misleading if you take it too strictly. The stable part usually refers to the asset, not the income stream. The income still depends on lending demand, reserve assets, market structure, liquidity, and protocol design.

That's why the right approach isn't to hunt the highest advertised return. It's to ask better questions. What funds the yield? How fast can it reprice? What can break? How fast can you exit? People who stay in DeFi long enough learn that these questions matter more than the headline APY.

There are two workable paths from here. One is manual. You build your own watchlist, monitor protocol changes, compare opportunities, and move capital yourself. That can work well if you have the time and the interest.

The other path is automated. You still care about risk, but you let software handle more of the scanning, monitoring, and allocation work. For many time-poor professionals, that's the more sensible model. It aligns with what stable yield is: not free money, but a set of changing spread opportunities that reward disciplined oversight.

If you want to earn in DeFi, the decision isn't whether to participate. It's how much operational burden you want to carry yourself.

If you want a lower-friction way to put stablecoins to work, Yield Seeker offers an AI-powered workflow for automated, risk-aware stablecoin yield. You can start with as little as $10 USDC on Base, keep funds accessible with no lockups or withdrawal fees, and let a personalized AI agent handle the monitoring and allocation work that usually makes DeFi yield so time-consuming.