You’re probably in one of two positions right now. You either hold stablecoins because you’re tired of watching portfolio value swing wildly with the rest of crypto, or you hold them because you want yield but don’t want the full risk profile of directional bets.

That’s where most explanations stop. They tell you a stablecoin is “a token pegged to a fiat currency” and move on. In practice, that definition isn’t enough to help you decide where to park capital, what kind of yield is worth taking, or how to avoid the quiet ways stablecoin strategies can fail.

The useful question isn’t just what a stablecoin is. It’s what happens after you own one.

The Search for Stability in a Volatile Market

Crypto gives you speed, access, and programmable finance. It also gives you price moves that can turn a normal workday into risk management. Many stablecoin users aren’t chasing novelty. They’re trying to hold value without leaving the digital asset ecosystem.

A stablecoin is the simplest answer to that problem. It’s a blockchain-based asset designed to track a reference value, usually the US dollar. For traders, it’s where capital waits between positions. For treasury teams, it’s digital cash. For DeFi users, it’s often the base asset for lending, liquidity, and automated yield strategies.

This has moved far beyond niche crypto plumbing. By October 2025, the total stablecoin market capitalization reached $312 billion, and transaction volumes hit $33 trillion in 2025, a 72% year-over-year increase, even outpacing Visa’s payment volumes in 2024, according to Stablecoin Insider’s 2025 market statistics.

Stablecoins matter because they let users keep the speed of crypto without taking full exposure to crypto volatility.

That scale changes how you should think about them. Stablecoins aren’t just a defensive parking lot anymore. They’re part of the operating layer of digital finance. They settle trades, move funds across chains, support lending markets, and increasingly act as the unit of account for on-chain activity.

If you already understand DeFi at a high level, stablecoins are the cash leg inside that system. If you want a quick refresher on how those rails fit together, this DeFi overview breaks down the broader mechanics.

Why busy professionals gravitate to stablecoins

A smart, time-constrained investor usually wants three things:

Capital stability: Less exposure to sudden drawdowns than holding volatile assets directly.

Operational flexibility: Funds that can move quickly between wallets, exchanges, and protocols.

Yield potential: The ability to earn on idle balances instead of leaving them unproductive.

Stablecoins can deliver all three. But only if you understand what’s backing the peg, how redemption works, and where your yield is coming from.

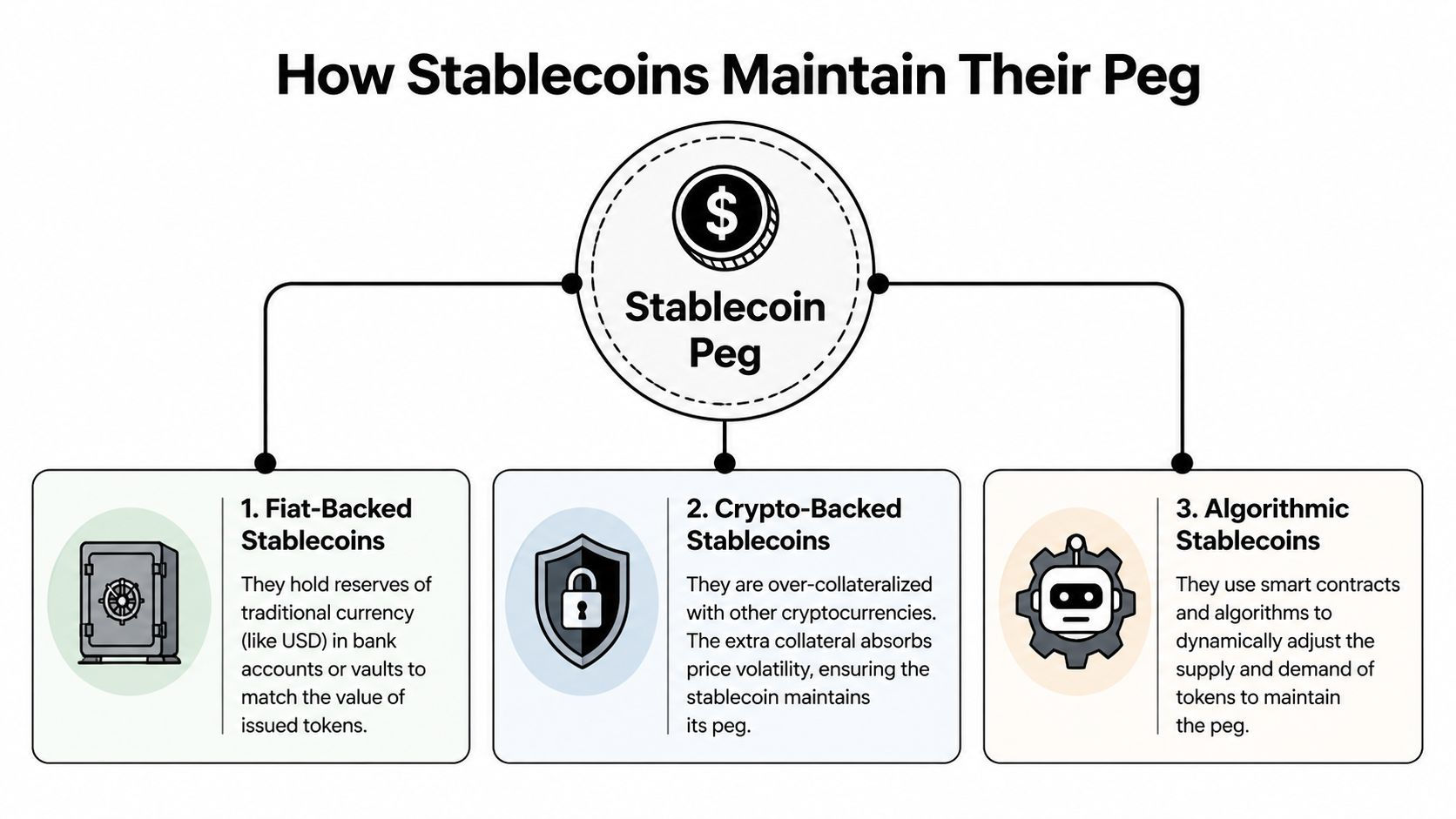

How Stablecoins Maintain Their Peg

The easiest way to understand stablecoins is to stop thinking of them as one category. They share a goal, but they use different machinery to get there. That machinery matters because it shapes both safety and yield.

Fiat-backed stablecoins

This is the model commonly understood. A fiat-backed stablecoin works like a digital claim on traditional reserves. You can think of it as a tokenized IOU. The issuer takes in dollars or dollar-like reserve assets and issues tokens against them.

USDC is the cleanest mental model here. In plain terms, the promise is straightforward. For each token in circulation, there should be reserve assets that support redemption at or near par.

That simplicity is why fiat-backed stablecoins dominate everyday usage. They’re easy for users to understand, easy for treasury teams to account for, and easier for protocols to accept as base collateral. If your goal is stable purchasing power plus low-friction movement across DeFi, this category usually feels the most familiar.

Crypto-backed stablecoins

Crypto-backed stablecoins use a very different setup. Instead of holding bank deposits or Treasury-like reserves, the system locks volatile crypto assets as collateral and issues a stable asset against them.

The best analogy is a pawn shop. You deposit an asset worth more than what you borrow, because the thing you posted can drop in price. That extra collateral acts as a shock absorber.

This design can reduce reliance on a centralized issuer, but the trade-off is complexity. If the collateral falls too quickly, positions may need to be liquidated. That means the peg depends not only on demand for the stablecoin, but also on collateral management, liquidation design, and the behavior of users under stress.

Practical rule: If you can’t explain what collateral sits underneath a stablecoin and how it gets liquidated, you shouldn’t use that coin as the base layer of a yield strategy.

Algorithmic stablecoins

Algorithmic stablecoins try to maintain a peg through supply adjustments, incentive structures, or other programmed market mechanisms rather than direct one-to-one reserve backing. The common analogy is a thermostat. If the room gets too hot, the system cools it. If price moves away from target, the protocol tries to expand or contract supply to pull it back.

That can look elegant on paper. It can also break in ugly ways when confidence disappears, arbitrage slows down, or the surrounding market infrastructure gets stressed.

That’s why infrastructure quality matters so much. J.P. Morgan’s stablecoin analysis notes that 41% of firms prioritize speed and 34% prioritize compliance as essential requirements, which tells you where serious users focus. They want reliable settlement, strong rails, and predictable execution. Not theoretical efficiency that fails when the market gets noisy.

What works and what usually doesn’t

A quick comparison helps:

Type | Simple mental model | Main strength | Main weakness |

|---|---|---|---|

Fiat-backed | Digital dollar claim | Familiar and operationally simple | Depends on issuer, reserves, and redemption process |

Crypto-backed | Overcollateralized on-chain loan | More native to DeFi and less issuer-dependent | More moving parts, liquidation risk, collateral volatility |

Algorithmic | Supply-adjusting system | Can be capital efficient in theory | Confidence-sensitive and more fragile under stress |

For yield strategies, this distinction matters a lot. A stablecoin isn’t “safe” just because the chart looks flat most days. The peg is the output. The mechanism underneath is the product.

Primary Use Cases for Stablecoins Today

The most practical way to understand stablecoins is to watch what people do with them. Their real value shows up in workflows, not definitions.

The DeFi user who wants yield without market timing

A typical DeFi user doesn’t always want to predict where ETH or BTC goes next. Sometimes the job is simpler. Preserve capital, stay liquid, and put idle balances to work.

Stablecoins are the core asset for that approach. Users lend them into money markets, provide them to liquidity pools, or route them into managed strategies that rebalance across protocols. The appeal is obvious. You can stay on-chain, keep optionality, and earn without needing a bullish market to be right.

That doesn’t mean the yield is free money. It usually comes from borrower demand, liquidity incentives, trading activity, or protocol-specific risk. But stablecoins make it possible to separate “earning” from “speculating” in a way that volatile assets often don’t.

The Web3 team that treats stablecoins like operating cash

Now take a different user. A DAO, creator collective, or Web3 startup receives revenue in crypto and needs to pay contributors, keep runway visible, and move funds globally without waiting on traditional banking rails.

Stablecoins fit that workflow well. Teams can invoice in them, settle payments quickly, hold reserves on-chain, and deploy part of treasury balances into conservative strategies while keeping the rest liquid. For many operators, that’s less about ideology and more about execution. They want a digital cash layer that works across wallets, exchanges, and protocols.

A short explainer is helpful here if you want to see those rails in action:

Where stablecoins sit in practice

The role stablecoins play depends on the user:

For traders: They’re dry powder between positions.

For lenders: They’re the asset used to earn yield with lower directional exposure.

For treasury managers: They function like digitally native cash.

For cross-border operators: They’re a transfer rail that doesn’t stop at banking hours.

The same stablecoin can be a settlement asset, a treasury reserve, and a yield-bearing base position. The difference comes from how the holder uses it.

That flexibility is why stablecoins became foundational so quickly. But once you start using them for yield, the easy story ends. The next question is whether the coin, the protocol, and the path to redemption still work when conditions get rough.

Understanding the Real Risks of Stablecoins

Stablecoins look calm right up until they don’t. That’s why the risk conversation matters more than the branding. If you’re using a stablecoin for yield, you’re not only evaluating the token. You’re evaluating every layer underneath it.

Peg risk

Peg risk is the most visible failure mode. A stablecoin is supposed to hold close to its reference value. If confidence in reserves, redemption, liquidity, or market structure weakens, the token can trade below that level.

That matters even if you never redeem directly with the issuer. In DeFi, collateral values, borrowing limits, and liquidation thresholds often assume a stablecoin remains stable enough. Once the market questions that assumption, losses spread quickly through lending and liquidity systems.

A lot of users treat temporary depegs as noise. That’s a mistake. A depeg is a direct test of whether the system can absorb stress.

Counterparty risk

Counterparty risk is less visible because it sits behind the token. With fiat-backed stablecoins, users depend on the issuer to manage reserves, process redemptions, maintain banking relationships, and communicate clearly when pressure rises.

The regulatory backdrop is shifting here. The New York Fed’s historical perspective on stablecoins describes how the GENIUS Act, passed by U.S. Congress in July 2025, created a federal framework for stablecoin issuance and imposed collateralization and anti-money-laundering requirements. That doesn’t remove risk, but it does show that stablecoins are now close enough to mainstream finance that lawmakers are building dedicated rules around them.

Counterparty risk isn’t only about fraud. It’s also about operational failure. If reserves are hard to verify, if redemption channels are uneven, or if banking access tightens, users can learn very quickly that a tokenized dollar isn’t the same thing as dollars in hand.

Smart contract risk

On-chain stablecoins inherit software risk. Once a stablecoin moves through smart contracts, bridges, vaults, lending markets, or automated allocators, code quality becomes part of your credit analysis.

According to the SEC’s stablecoin regulatory framework discussion, all major stablecoins have experienced price fluctuations, and their reliance on smart contracts introduces critical vulnerabilities. Programming errors can lead to blocked redemptions, frozen transfers, and collateral theft, and that risk compounds across every DeFi protocol where funds are deposited.

A stablecoin can look healthy at the issuer level and still become hard to access if the contract layer around it breaks.

If you’re allocating across DeFi, many portfolios become weaker than users realize. The stablecoin may be fine. The vault holding it may not be. The protocol receiving it may have upgrade risk. The strategy manager may rely on assumptions that fail during congestion or market stress.

If you want a deeper framework for reviewing those layers, this guide to protocol safety analysis is the right place to start.

Regulatory and market structure risk

Regulatory risk doesn’t always show up as a ban. More often, it appears as uneven rules, restricted access, fragmented liquidity, or changing redemption terms.

For users, the practical consequence is simple. A stablecoin’s reliability depends on legal structure, custody arrangements, banking rails, and where the token is used. A coin can be compliant in one setting and operationally awkward in another.

The lesson is straightforward:

Don’t isolate the token from the stack: Issuer, reserves, contracts, and protocol design all matter.

Don’t confuse liquidity with safety: A widely traded stablecoin can still behave poorly under stress.

Don’t outsource diligence entirely to the market: Fast adoption doesn’t guarantee resilience.

How to Evaluate and Choose a Stablecoin

Choosing a stablecoin often follows the same hurried pattern as selecting a savings app. Users frequently look for the familiar ticker, glance at the yield, and assume the rest must be fine. That works until it doesn’t.

A better approach is boring on purpose. You want a repeatable filter that helps you reject weak options before you start chasing returns.

Start with the redemption path

The first question isn’t yield. It’s redemption. Who can redeem the token, under what conditions, and how direct is that access?

That distinction matters because retail users often don’t sit in the same position as institutions. The Bank Policy Institute’s warning on stablecoin risks highlights an often-overlooked issue: retail investors on exchanges lack the direct redemption access that institutional investors have with issuers, creating a two-tier system where stablecoins can depeg significantly when institutional support wanes and risk gets pushed onto retail lenders in DeFi.

If you hold through an exchange, a wallet, or a DeFi venue, your ability to exit may depend on market liquidity rather than direct issuer redemption. That changes the risk profile immediately.

Use a practical due diligence checklist

Before depositing into any strategy, check the stablecoin itself with a simple framework:

Reserve clarity: Can you understand what backs the token in plain language, or do you need to decode vague issuer language?

Redemption mechanics: Is redemption direct, limited, permissioned, or only realistic for larger players?

Operational footprint: Is the stablecoin broadly usable across the chains and protocols you rely on?

Stress behavior: When confidence drops, does the token usually recover cleanly, or does liquidity thin out fast?

Dependency stack: Are you just holding the token, or are you adding vault risk, bridge risk, and lending market risk on top?

This kind of review sounds basic, but it filters out a lot of avoidable mistakes.

Don’t rank strategies by APY first

High displayed yield attracts attention because it compresses decision-making into one number. That’s exactly why it’s dangerous.

A stablecoin strategy can show a strong nominal return while subtly embedding weak collateral, thin liquidity, reprice risk, or protocol-level dependencies that only surface during stress. In DeFi, yield is often payment for absorbing a risk someone else doesn’t want to hold.

A cleaner way to consider this:

What you see | What you should ask |

|---|---|

High APY | Why is this yield available at all? |

Familiar stablecoin ticker | Who can redeem it directly? |

Deep protocol integration | What happens if collateral reprices suddenly? |

Easy deposit flow | How many smart contract layers sit between you and withdrawal? |

Chasing the top number usually means you’re underwriting a risk you haven’t named yet.

What disciplined users do differently

Experienced operators don’t assume “stablecoin yield” is one homogeneous category. They separate three decisions:

Which stablecoin to hold

Which protocol to trust with it

Which yield source is worth the complexity

That distinction matters. A decent stablecoin can become a poor choice inside a weak strategy. A well-designed protocol can still expose users to hidden redemption asymmetry. And a convenient interface can hide a messy stack of risks underneath.

The safest habit is to prefer simplicity when the incremental yield doesn’t clearly justify the added layers. In practice, simple, transparent structures often age better than clever ones.

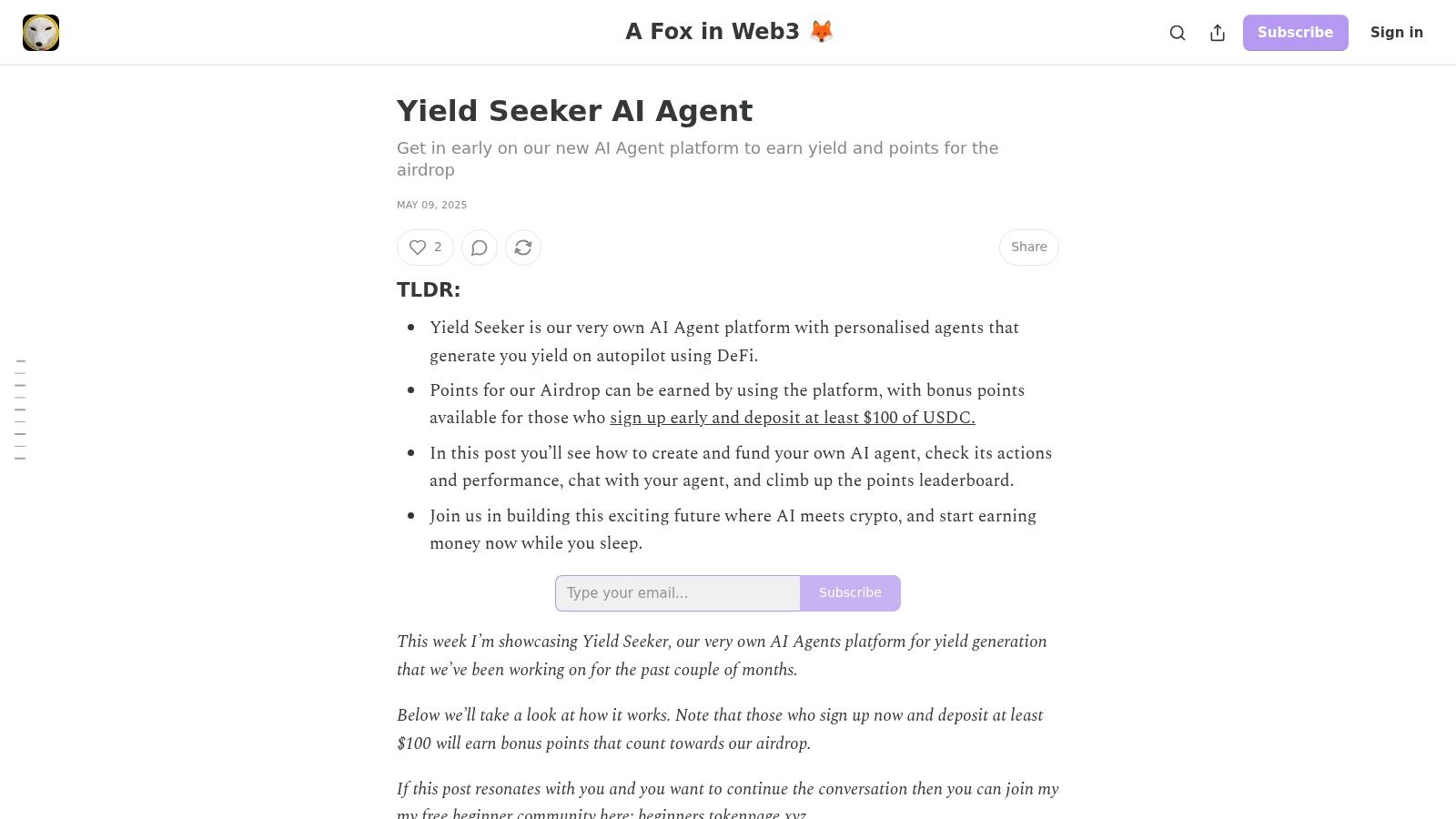

Automating Safe Yield with an AI Agent

Stablecoin investing requires operational work. You’re not just picking an asset. You’re tracking issuer quality, redemption structure, protocol security, liquidity conditions, and changing yields across a fragmented market.

Manual management of that task is not sustainable for many. They have jobs, teams, clients, or other positions to manage. Even experienced DeFi users eventually run into the same constraint. The market moves faster than a spreadsheet.

That’s where automation starts to make sense, but only if it’s risk-aware. A useful system doesn’t just route funds toward the highest displayed yield. It monitors where that yield comes from, how conditions are changing, and whether the extra return still compensates for the added risk.

One practical example is Yield Seeker, which lets users deposit USDC on Base and use an AI agent to monitor and allocate capital across DeFi protocols while keeping funds accessible without lockups or withdrawal fees. The point isn’t automation for its own sake. The point is reducing the manual burden of scanning opportunities, checking changing conditions, and deciding when a yield source no longer looks attractive on a risk-adjusted basis.

What an AI agent should actually do

A credible AI layer in this category should help with tasks that are repetitive, time-sensitive, and easy to get wrong by hand:

Monitor protocol conditions: Watch for changing yields, liquidity shifts, and strategy drift.

Compare opportunities across venues: Surface options across a market that’s too fragmented for most users to track continuously.

Keep decisions legible: Show where capital sits and why it was allocated there.

Preserve user control: Automation should simplify management, not hide what’s happening.

That broader shift toward machine-assisted evaluation is also why frameworks for understanding what language models are good at matter. If you want a grounded explanation of how this thinking applies to modern interfaces and decision support, Algomizer's LLMO insights are worth reading.

For readers who want to go deeper on the crypto side, this overview of AI agents in crypto connects the concept to real on-chain workflows.

The practical takeaway is simple. Stablecoin yield can be useful, but the work sits in the details. The more fragmented DeFi becomes, the more valuable disciplined monitoring becomes. For most users, intelligent automation is no longer a convenience feature. It’s the only realistic way to stay consistent without turning stablecoin management into a second job.

If you want a hands-off way to put idle USDC to work while keeping visibility into where funds are deployed, Yield Seeker offers an AI-driven approach built around automated, risk-aware stablecoin yield management on Base.