You probably already know the feeling. You hold dollars in a bank account or stablecoins in a wallet, and they just sit there. Safe enough, useful enough, but idle.

That’s where USDC gets interesting. It isn’t just a “crypto dollar” for trading memes or parking funds between market moves. It’s a digital dollar with enough trust, liquidity, and technical flexibility to act as working capital on-chain. For a lot of people, that changes the question from “What is USDC?” to “What can I do with it without taking dumb risk?”

Introducing USDC The Digital Dollar

USDC is a stablecoin, which means it’s designed to track the value of the U.S. dollar. If Bitcoin behaves like a volatile commodity and Ethereum behaves like programmable infrastructure, USDC behaves more like cash that can move through blockchain networks.

That simple framing matters. Most beginners either overcomplicate USDC or underestimate it. They hear “digital dollar” and assume it’s boring. In practice, boring is the feature. A stable unit of account is what makes lending, payments, treasury management, and yield strategies usable.

USDC also operates at real scale. According to Circle’s State of the USDC Economy report, USDC, the second-largest stablecoin, saw its circulating supply surge more than 78% year-over-year by late 2025, reaching approximately $76-77.5 billion in market cap and contributing to an all-time transaction volume over $18 trillion.

Why people use USDC instead of just wiring dollars

A bank balance is familiar, but it doesn’t plug directly into on-chain apps. USDC does. You can send it globally, hold it in self-custody, trade with it, post it as collateral, or deploy it into yield strategies without converting into a volatile asset first.

That combination is why USDC sits in the middle of so many workflows:

Payments: People use it to move dollar value without waiting on banking hours.

Trading: Traders use it as a stable quote asset and a place to sit between positions.

Treasury management: Teams hold it because it’s easier to use in crypto-native operations than bank wires.

Yield generation: Savers use it as the base asset for strategies that aim to earn on otherwise idle balances.

USDC makes the on-chain world easier to reason about because it keeps the unit stable while the strategy changes.

The part many guides skip

Most articles stop at “USDC is a digital dollar.” That’s accurate, but incomplete. The useful question is why a digital dollar matters in practice.

If your base asset is stable, you can separate market risk from strategy risk. You’re no longer asking, “Will my token go up?” You’re asking, “Where can I put this dollar-denominated asset to earn something, and what risks am I accepting in return?” That’s a much cleaner mental model.

USDC is the bridge between traditional cash logic and on-chain finance. Once you understand how it keeps its value, the rest starts to click.

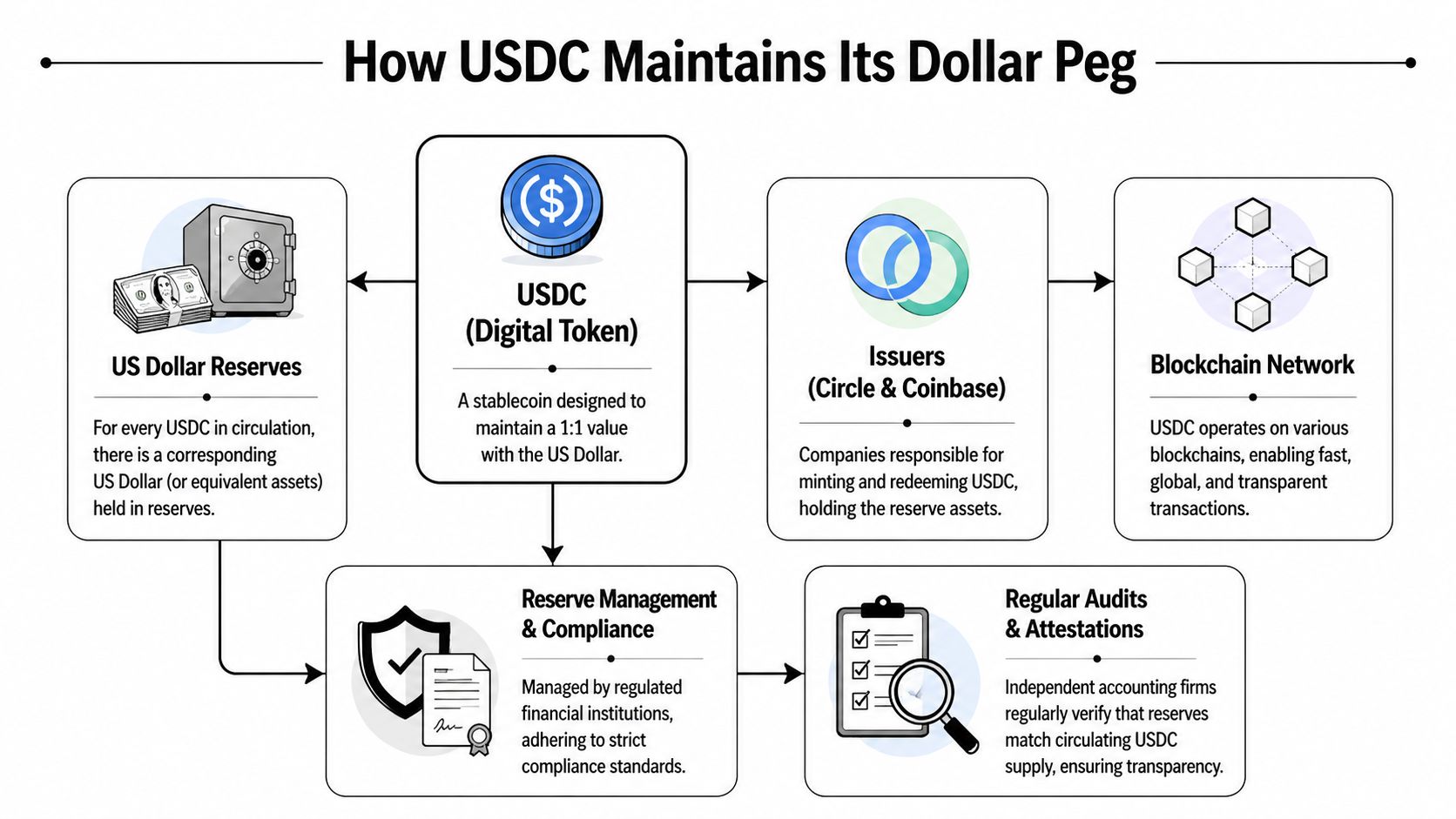

How USDC Maintains Its Dollar Peg

A good way to think about USDC is as a digital claim on dollar reserves. Not in the loose, hand-wavy sense that crypto sometimes uses. More like a coat-check ticket. You hand over one real asset, receive a tokenized receipt, and that receipt is supposed to be redeemable for the thing behind it.

With USDC, the key promise is simple. One USDC should be redeemable for one U.S. dollar.

What sits behind the token

USDC’s peg depends on reserves, not vibes. The reserves are described as cash and short-term U.S. Treasury securities, and the operating model depends on several distinct actors doing different jobs.

Circle issues and redeems USDC. That means it’s the company responsible for creating tokens when dollars come in and removing tokens when dollars are redeemed. Reserve assets are then held and managed through traditional financial institutions rather than left as an abstract promise inside crypto.

According to USDC statistics summarized by SQ Magazine, USDC's peg is supported by monthly independent attestations from firms like Grant Thornton, a practice maintained for over 41 consecutive months, with reserves managed by BlackRock and held by BNY Mellon, generating $658 million in reserve income in a single quarter of 2025.

Why attestations matter

Readers often get confused here. “Backed 1:1” sounds reassuring, but what you really want to know is: who checks?

Independent attestations matter because they create an external verification loop. They don’t remove every possible risk in the system, but they do make “trust us” less central. A stablecoin backed by reserves is only as credible as the process that proves those reserves exist and match the circulating supply.

Here’s the plain-English version:

Users bring in dollars.

Circle can mint new USDC against those assets.Reserves are held in traditional financial instruments.

That keeps the backing tied to relatively conservative dollar assets rather than volatile crypto collateral.Independent firms verify the picture regularly.

That gives users a recurring check on whether the reserve story still holds.

Practical rule: A stablecoin’s real product isn’t the token. It’s the redemption process plus the transparency around reserves.

Why this model feels different from algorithmic stablecoins

USDC belongs to the reserve-backed camp. That’s different from designs that try to maintain a peg through incentives, balancing mechanisms, or crypto collateral structures that can become unstable under stress.

Reserve-backed doesn’t mean risk-free. It means the mechanism is easier to inspect. If one USDC is tied to one dollar’s worth of reserve assets, the peg logic is understandable. If a stablecoin depends on market reflexes and confidence loops, the failure modes are harder for ordinary users to evaluate.

That clarity is a big reason USDC became a core building block for on-chain apps. If you’re trying to earn yield with a stable asset, the foundation matters. You want the base layer to be legible before you start layering protocols on top of it.

Exploring USDC Across the Crypto Ecosystem

A useful way to understand USDC is to follow one coin through a normal crypto workflow.

It might start on an exchange, where someone buys USDC because they want dollar exposure without leaving the blockchain. Then it moves into a wallet, where it becomes portable cash for the on-chain world. From there, it can head in several directions. It can sit in a lending market as collateral, move into a decentralized exchange as one side of a trading pair, or live in a DAO treasury as the stable part of a project’s reserves.

USDC works well in these roles because it’s not trying to do too much. It holds steady while other parts of the system stay dynamic.

One asset, several jobs

In DeFi, the same USDC can serve very different purposes depending on context:

Trading asset: On decentralized exchanges, USDC is often the “calm side” of a trade.

Collateral asset: In lending protocols, borrowers and lenders both prefer something that doesn’t swing wildly.

Treasury asset: Web3 teams often want operational funds in a stable denomination.

Settlement asset: When users move between protocols, USDC acts like a common language.

This is one reason stablecoins became so central to crypto’s day-to-day economy. They reduce friction between decisions.

Why chains matter more than most beginners expect

A lot of confusion comes from seeing “USDC” as one thing that lives in one place. In practice, USDC exists across multiple blockchain networks, and that changes cost, speed, and user experience.

According to The Standard’s discussion of USDC’s multi-chain architecture, USDC's multi-chain architecture on 32+ networks, including high-speed L2s like Base and Polygon, allows it to cut transaction fees to as low as $0.002, a 95%+ reduction compared to Ethereum mainnet, enabling smooth liquidity routing across a $60B+ circulation.

That’s the practical reason so many newer yield strategies happen away from Ethereum mainnet. The economics are friendlier. A small balance can move without getting eaten by fees.

A dollar that costs too much to move stops behaving like cash. Multi-chain USDC fixes that for a lot of everyday use cases.

If you’re trying to understand why activity keeps spreading across ecosystems, it helps to study how different chains attract users and builders. The Mava blog on Ton growth is a useful example of how infrastructure, distribution, and user experience can pull liquidity into new environments.

The bigger takeaway

USDC isn’t valuable just because it’s stable. It’s valuable because it’s stable and usable. Once it can move cheaply across networks, it stops being a parked asset and starts acting like digital working capital.

That’s the fundamental shift. Holding USDC is one thing. Deploying USDC across the ecosystem is where the opportunity starts.

Understanding the Risks and How to Mitigate Them

USDC is easier to reason about than many crypto assets, but “easier” doesn’t mean “risk-free.” Most problems users face don’t come from the token alone. They come from the environment around it.

Three risks matter most in practice.

Smart contract risk

If you put USDC into Aave, a DEX pool, or a vault product, you’re no longer only relying on USDC’s reserve model. You’re also relying on the code of that protocol.

A bug, exploit, bad oracle design, or poor risk management in the app layer can cause losses even if USDC itself remains stable. This is the classic beginner mistake. They think, “I’m using a stablecoin, so the strategy is safe.” The coin may be stable. The protocol may not be.

Ways to reduce that risk:

Start with established protocols: Use products with a longer operating history and clearer documentation.

Read the mechanism first: If you can’t explain how the yield is generated, don’t deposit.

Avoid stacking complexity: Combining bridges, vaults, borrowed capital, and obscure assets multiplies failure points.

Custody risk

A second risk is where you hold your USDC. If it stays on a centralized exchange, you don’t control the private keys. That can be convenient, but it means your access depends on the exchange staying solvent, operational, and willing to process withdrawals.

Self-custody changes that. You hold the wallet keys, so the asset is under your control. But self-custody also shifts responsibility to you. If you lose your seed phrase or sign a malicious transaction, there’s no support desk that can reverse it.

For a practical framework, this guide to understanding stablecoin risks is a helpful reference.

De-peg risk

Stablecoins can trade away from one dollar during stress. USDC’s well-known example came during the banking turmoil tied to Silicon Valley Bank exposure. According to the verified data, USDC fell to $0.8776 in 2023 before recovering.

That event is worth studying because it shows both sides of the story. The risk was real. The market reacted to concern about reserve access. But the recovery also showed why reserve structure and transparency matter.

Don’t treat a stablecoin de-peg as impossible. Treat it as a stress event you should be ready to evaluate.

A sensible mitigation plan looks like this:

Keep some liquidity outside any single app.

Don’t confuse stable price behavior with zero counterparty risk.

Watch where your USDC is deployed, not just what token it is.

If you’re using DeFi for yield, understand the exit path before you enter.

Good risk management in crypto usually feels a bit boring. That’s a positive sign.

A Practical Guide to Earning Yield on USDC

The biggest missed opportunity with USDC is simple. A lot of holders use it as digital cash, but not as a productive asset.

That gap is real. According to Binance Square’s discussion of the stablecoin yield gap, a significant "yield gap" exists, as most USDC activity is focused on payments and access to dollars, while alternatives that pass on yield from U.S. Treasuries directly on-chain remain underexplored by the majority of holders, especially in emerging markets.

Three common ways to earn on USDC

You don’t need one perfect strategy. You need a model for choosing among tradeoffs.

Strategy | Typical APY | Risk Level | Complexity |

|---|---|---|---|

Lending protocols | Variable | Moderate | Low to moderate |

Liquidity provision | Variable | Moderate to high | Moderate |

Yield products and automated vaults | Variable | Moderate | Low to moderate |

The table uses qualitative labels because rates change constantly. That’s the right way to think about yield in DeFi anyway. The headline number matters less than the mechanism producing it.

Lending protocols

This offers the simplest entry point. You deposit USDC into a lending market such as Aave-style platforms, and borrowers pay to access that liquidity. Your yield comes from lending demand.

The mental model is close to an interest-bearing cash account, but with protocol risk added. The main benefits are clarity and simplicity. You usually know where the yield comes from, and your asset remains in USDC terms.

Good fit for people who want:

Clear mechanics: Borrowers create the demand side.

Stable denomination: You’re not taking direct exposure to a second token.

Simple monitoring: It’s easier to check a lending position than an LP position.

Liquidity provision

You can provide USDC alongside another asset to help a DEX facilitate trading. In return, you may earn trading fees and sometimes additional incentives.

This can be attractive, but it’s not “set and forget” in the same way lending can be. If the paired asset moves sharply, your position changes shape. That’s where impermanent loss enters the conversation. It’s not always catastrophic, but it does mean LPing isn’t just passive savings with a fancy wrapper.

Yield products and automated tools

Some users don’t want to compare protocols every day. They want a wrapper that routes funds into opportunities on their behalf. That can include structured savings products, vaults, or automation layers that monitor DeFi venues and adjust allocations.

These tools are helpful when time is the scarce resource. The tradeoff is that you need to understand both the underlying strategy and the automation layer. If you want a broader view of how people compare aggressive opportunities, this piece on highest APY yield farming gives useful context.

The best USDC yield strategy is usually the one you can explain, monitor, and exit without confusion.

How to choose without overthinking it

A practical filter helps:

If you want the cleanest setup, start with lending.

If you understand DEX mechanics and accept position drift, consider LPing.

If you value convenience, automated products can make sense, provided you understand what they do under the hood.

The key isn’t chasing the highest displayed APY. It’s matching the strategy to your tolerance for complexity, smart contract exposure, and active management.

Automate Your Earnings with AI on Base

Manual yield hunting gets old fast. Rates move. Pools change. Incentives appear and disappear. A setup that looked sensible on Monday might be mediocre by Thursday.

That’s why automation is becoming more attractive in stablecoin strategies. People don’t just want access to DeFi. They want a system that can watch multiple venues, compare options, and react without forcing them to live inside dashboards.

Why Base makes this easier

Base is a natural environment for USDC-focused automation because lower fees make frequent reallocation more practical. If a strategy needs to move capital between protocols, high transaction costs can cancel out the benefit. On a lower-cost network, smaller balances and more active management become viable.

There’s also the onboarding issue. A lot of people still hold USDC on one chain and hesitate to move it because bridges feel risky or confusing.

According to Eco’s guide to USDC and Circle’s transfer system, Circle's Cross-Chain Transfer Protocol (CCTP) allows users to securely move native USDC to chains like Base in under 30 seconds by burning on the source and minting on the destination, eliminating risky wrapped tokens and unifying liquidity for AI-driven yield strategies.

That matters more than it might seem. “Burn and mint” sounds technical, but the user benefit is simple. You move native USDC, not a wrapped imitation that introduces extra trust assumptions.

What automation actually does

An automated system for USDC yield doesn’t create magic returns. It handles repetitive work:

Monitoring protocols: Watching rates and availability across venues.

Allocating capital: Moving funds based on a defined risk profile.

Reducing manual overhead: Saving you from checking multiple apps yourself.

Keeping funds flexible: Supporting strategies that don’t rely on long lockups.

The broader pattern is familiar beyond crypto too. If you’re interested in how this logic shows up in other workflows, Unlocking AI business automation is a solid read on why teams increasingly offload repeatable decisions to software.

One practical option on Base

For people who want a guided route, USDC on Base is a good starting point for understanding the setup. One platform in this category is Yield Seeker, which lets users deposit USDC on Base and have an AI agent monitor and allocate capital across DeFi protocols based on risk-aware settings. The product information provided by the publisher says users can start with $10 USDC on Base, keep funds accessible, and avoid lockups.

That setup won’t replace judgment. It does remove a lot of mechanical friction. And for most busy users, friction is the main reason yield opportunities stay untouched.

The hardest part of earning on USDC usually isn’t understanding the idea. It’s maintaining the process.

If you’re holding USDC and want a lower-friction way to put it to work, Yield Seeker offers an AI-powered workflow for automated stablecoin yield on Base. You can create an account, deposit as little as $10 USDC, and let a personalized agent manage allocations while keeping your funds available without lockups.