You're probably looking at two DeFi protocols that seem to offer the same thing. Same stablecoin vault idea, same polished dashboard, same social buzz. Yet one reward token holds up, treasury decisions stay coherent, and yields remain believable. The other token bleeds lower, emissions keep coming, and the “high APY” starts to look like users paying each other with a shrinking coupon.

That gap usually isn't explained by branding or even product quality alone. It's explained by tokenomics.

For stablecoin holders, tokenomics isn't an abstract crypto-native topic. It affects whether a protocol can attract sticky liquidity without bribing it forever, whether governance is likely to act in depositor interests, and whether the yield attached to your USDC is coming from real protocol activity or from token issuance that can unravel fast. If you're choosing where to park capital, tokenomics is part risk analysis, part incentive mapping, and part common sense.

Why Some Crypto Tokens Succeed and Others Fail

A common mistake is evaluating a protocol token the way people evaluate a stock ticker on social media. They compare price charts, notice a recent bounce, then assume “strong token” means “strong protocol.” In DeFi, that shortcut breaks quickly.

Two projects can ship similar products and still produce completely different outcomes for token holders and depositors. One may use its token as a real coordination tool. Users stake it, vote on parameters that matter, and accept lockups because the protocol has a reason to exist beyond speculation. Another may bolt on a token after the fact, promise rewards, and hope emissions create loyalty. That rarely lasts.

The blueprint behind price action

Tokenomics is the economic blueprint of a token. It governs how tokens are created, who gets them, when they hit the market, what they can do, and whether the system gives people a reason to hold rather than dump. In practice, that means tokenomics shapes three things investors care about immediately:

Scarcity

Dilution

Utility

If a protocol keeps issuing more tokens without building durable demand, early yields can look attractive while the token absorbs the damage. If insiders control too much supply or tokens become available into weak demand, price pressure often appears long before the average depositor notices. If the token has no meaningful role in the protocol, holders are left with a governance receipt nobody needs.

Practical rule: A protocol token should solve an incentive problem. If it only solves a fundraising problem, assume friction later.

Yield-focused investors need this lens even more than directional token traders do. When you deposit stablecoins into a protocol, you're trusting an economic machine, not just a smart contract. If the machine depends on issuing more and more reward tokens to maintain activity, the sustainability of your yield is tied to a design choice that may not survive a slower market.

That's why tokenomics matters. It explains why some tokens become part of a functioning economy, while others become exit liquidity wrapped in governance language.

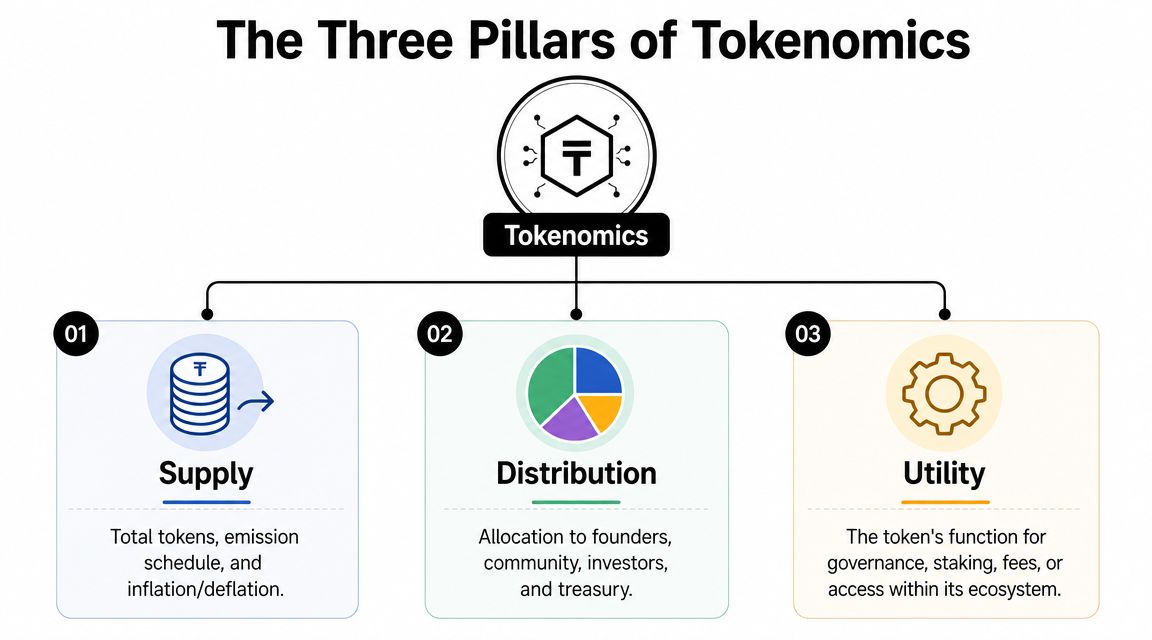

The Three Pillars of Tokenomics

A token can look attractive on a dashboard and still be structurally weak. The fast way to pressure-test it is to examine three moving parts together: supply, distribution, and utility. These are the mechanics that decide whether demand can absorb emissions, whether insiders can create persistent sell pressure, and whether the token has a job beyond subsidizing early users.

For stablecoin depositors, this matters more than it seems. If your yield depends on a reward token, these three pillars shape how long that yield can last and how much hidden risk sits underneath it.

Supply

Supply sets the dilution curve. Start with the basics: circulating supply, total supply, maximum supply if one exists, and who controls minting. Then ask the harder question. How quickly do new tokens reach the market, and who receives them first?

The contrast between major assets makes the point clearly. Bitcoin uses a fixed cap. Ethereum issues new ETH to pay validators. Dogecoin keeps adding new DOGE on a predictable schedule. Different models can work, but they create very different holder experiences, especially around scarcity and long-term dilution, as outlined in Arkm's tokenomics guide.

For protocol evaluation, raw supply numbers are only the start. A capped token can still punish holders if emissions are front-loaded. An inflationary token can still hold value if issuance pays for security, liquidity, or user growth that remains after rewards decline.

Distribution

Distribution determines who has inventory and when that inventory can hit the market. This often proves to be the breaking point for many token models in practice.

A protocol may market itself as community-owned while a small set of wallets controls governance, treasury decisions, or a large future release schedule. Team and investor allocations are not automatically bad. Early capital often funds the build. The trade-off is overhang. If large tranches vest into weak demand, token holders absorb the selling pressure, and stablecoin depositors often feel it later through lower incentives, weaker collateral quality, or stress on the treasury.

Uniswap's UNI is a useful reference point because the initial allocation made the split visible: a large share went to the community, while the remaining supply followed a scheduled release over time. That gap between circulating supply and fully diluted supply is what investors need to monitor. It affects float, governance concentration, and future sell pressure.

Utility

Utility answers the simplest question in tokenomics. Why does this token need to exist?

Good answers are specific. The token governs real protocol parameters. It must be staked to secure a system or to access an economic benefit. It captures a share of fees, improves execution, or gives holders a reason to keep exposure after emissions fall. Weak answers are usually vague promises about ecosystem growth.

Three forms of utility show up repeatedly:

Governance rights, where holders influence emissions, collateral settings, treasury use, or upgrades

Staking or locking, where holders commit capital for rewards, security, or voting weight

Fee or access functions, where the token is needed for payments, discounts, or participation

A token with weak utility can still trade well for a period. It rarely supports durable demand once the incentive budget shrinks.

Why these pillars matter together

The failure mode is usually interaction, not one bad metric. Strong supply design cannot rescue poor distribution. Broad distribution does not create value if nobody needs the token. High utility claims mean little if future emissions swamp demand.

This is the lens yield-focused investors should use. If a protocol pays stablecoin yield with a token that inflates quickly, sits in concentrated hands, and lacks durable utility, the posted APY is often borrowing from the future. If the token has controlled issuance, a credible holder base, and a real role in the protocol, the yield has a better chance of surviving a slower market.

That broader connection between incentive design and platform economics is worth studying. This piece on understanding business model tokenomics gives a useful strategic frame.

Then verify the story onchain. Check wallet concentration, treasury transfers, vesting behavior, staking participation, and governance turnout. A repeatable process for that work is covered in these on-chain analysis workflows.

Pillar | Core question | What to inspect |

|---|---|---|

Supply | How much can exist and how fast does it grow? | Circulating, total, max supply, emissions, mint authority |

Distribution | Who got the tokens and when do they gain access to them? | Team allocation, investor vesting, treasury control, airdrops |

Utility | Why would anyone hold or use it? | Governance power, staking design, fee value, access rights |

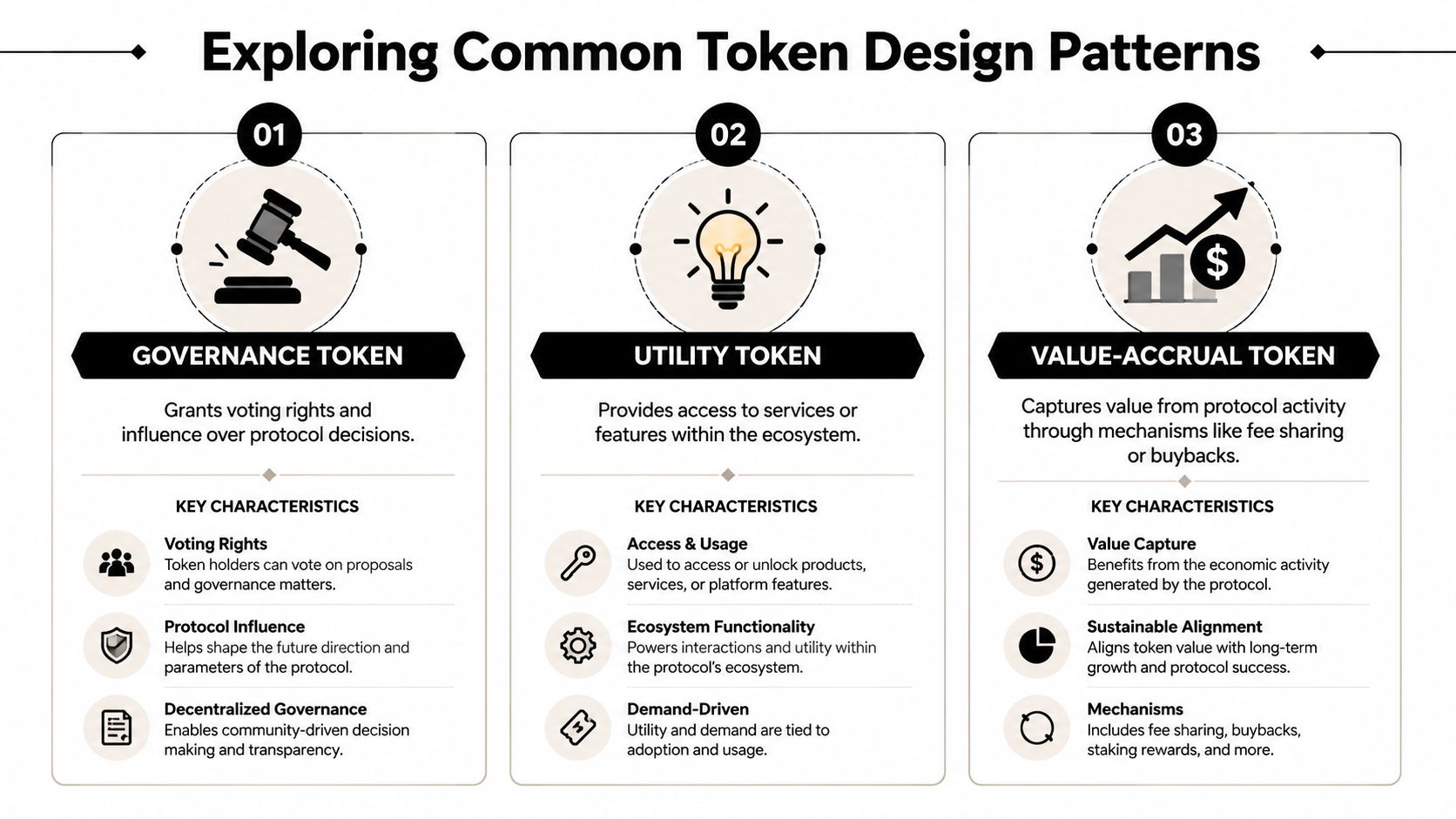

Exploring Common Token Design Patterns

A depositor sees 18% APY on stablecoins and assumes the protocol found a better strategy. Often the difference is token design. The yield is being shaped by who gets paid, in what asset, and whether those payouts come from revenue or fresh issuance.

Patterns matter because they repeat. Teams package them with new branding, but the economic logic is usually familiar. For yield-focused investors, the job is not to memorize labels. It is to ask what each pattern means for dilution, protocol revenue, and the safety of a stablecoin position if incentives cool off.

Governance-first tokens

Governance-first tokens give holders formal voting power over protocol decisions. In strong designs, those decisions affect emissions, collateral settings, fee routing, treasury use, or risk limits. In weak designs, token holders vote on low-impact proposals while a multisig, foundation, or core team still controls the decisions that matter.

That difference has direct consequences for stablecoin depositors. If a protocol can change reserve policy, collateral standards, or reward schedules through a process that holders do not really control, governance adds headline value but little protection. Protocol teams that explain admin powers clearly tend to be easier to underwrite. Good DeFi transparency practices matter more here than governance branding.

Governance can matter a lot without producing cash flow. Treat it as control rights first. Any upside from that control is a separate question.

Utility tokens

Utility tokens are tied to actions inside the product. They can be used for fees, access, boosted rewards, collateral functions, or application-specific tasks. The key question is whether that role is necessary.

A weak utility design usually shows up the same way. Users deposit stablecoins. Fees are earned in stablecoins. The protocol then inserts a volatile token into the workflow even though the product would function without it. That can create short-term buying pressure, but it also adds friction and balance-sheet risk for users who came for stable yield.

Good utility is hard to replace. Bad utility is a toll booth.

Value-accrual designs

This is the pattern many investors want to see because it connects protocol activity to tokenholder outcomes. Fee sharing, buybacks, revenue-directed staking, and similar structures all try to send some portion of economic value back to the token.

The trade-off is straightforward. If rewards are funded by actual usage, the design can hold up in quieter markets. If rewards depend on emissions that are justified by temporary token demand, the model is weaker than it looks. I pay close attention to what asset the protocol earns and what asset it distributes. When those two are disconnected, the gap usually shows up later in price pressure or lower real yield.

Deflationary marketing often muddies this category. Buybacks sound attractive, but buybacks funded by incentive-driven volume are less durable than buybacks funded by repeat, organic usage.

Inflationary workhorse models

Some tokens are meant to be issued continuously because they pay for security, validator participation, liquidity formation, or other ongoing network functions. Inflation is not automatically a flaw. It is a cost center.

The question is who absorbs that cost. If new supply goes to participants who create lasting protocol value, inflation can be rational. If issuance mainly props up headline APY, stablecoin depositors are often the exit liquidity. Brand strength and community attention do not remove this risk. A token can be well known, widely held, and still face meaningful dilution if a large share of supply has yet to enter circulation, as noted earlier.

Dual-token and real-yield structures

Some teams split responsibilities across two tokens. One handles governance, the other handles utility, incentives, or a more stable unit of account. That can make the system cleaner, but it can also split demand so thinly that neither token captures enough value to matter.

The more interesting shift is toward paying users in assets that already have market credibility, such as ETH or stablecoins, instead of relying only on newly issued native tokens. That gives depositors a cleaner way to judge whether the protocol is earning enough to support its payouts.

The more a protocol pays users in its own newly issued token, the more you need to ask whether rewards are revenue or just distribution.

How to Spot Tokenomic Red Flags

Bad tokenomics usually leaves clues in public. Teams publish whitepapers, contracts expose functions, and wallet activity shows who's receiving and moving supply. You don't need perfect forensic skills to catch many failures early. You need a skeptical process.

Start with the code and control surface

The first question is whether the token behaves according to fixed rules or according to a team's discretion. Tokenomics is an onchain incentive system implemented through smart contracts, and those preset rules around minting, distribution, utility, and removal from circulation are part of what makes supply behavior more predictable than discretionary policy, as explained in EXP's overview of tokenomics as code.

That's the theory. In practice, many projects still leave themselves broad administrative powers.

Red flags include:

Open-ended mint authority where a multisig or owner can create new supply without a narrowly defined process

Upgradeable contracts with vague limits that allow the core economics to change after users commit capital

Treasury opacity where key wallets aren't labeled or explained clearly

Governance concentration where a few addresses can dictate outcomes regardless of community participation

Read the reward design like a cash flow statement

A protocol promising high rewards isn't automatically fraudulent. But rewards need a payer.

If a stablecoin vault distributes yield, ask where the yield comes from. Trading fees? Borrowing activity? Validator revenue? External incentives? If the answer is “the protocol token,” then the next question is what supports the token itself. Too many systems stop there.

Watch for these patterns:

Circular utility. Users buy the token to stake it so they can earn more of the same token.

Compressed vesting. Team and investor allocations become liquid before the protocol has durable usage.

Narrative-first token use. The whitepaper says the token is “core to the ecosystem” but product flows barely require it.

Deposit growth bought with emissions. Liquidity arrives fast, then leaves as soon as rewards soften.

For a practical companion to token analysis, this guide to DeFi transparency checks helps frame what protocols should disclose before users trust them with funds.

A short explainer can help if you want a visual walkthrough before reading contracts:

What to inspect before depositing

You can do a fast first-pass review with four checks:

Check | What you're looking for | Why it matters |

|---|---|---|

Allocation map | Team, investor, community, treasury wallets | Concentration often becomes sell pressure or governance control |

Emission logic | How new tokens are minted and why | Unclear issuance usually means future dilution surprises |

Real token role | Whether the app genuinely needs the token | Forced utility rarely supports lasting demand |

Disclosure quality | Vesting, treasury policy, governance process | Weak transparency often precedes economic risk |

If a team explains tokenomics with slogans instead of schedules, assume the hard part isn't solved.

Tokenomics for Yield Farmers and Stablecoin Holders

For yield farmers, tokenomics isn't mainly about whether a governance token might moon. It's about whether your stablecoin yield depends on incentives that can unwind underneath you.

A protocol can pay depositors in three broad ways. It can distribute revenue generated by real usage. It can subsidize activity with treasury assets. Or it can print and distribute its own token. Most protocols use some blend of those approaches, but the balance tells you a lot about risk.

When token rewards support yield

There's nothing wrong with token incentives. They can help a protocol bootstrap liquidity, coordinate users, and direct capital where the system needs it. For a new market, that can be rational. The mistake is assuming incentive-driven demand equals durable demand.

One of the hardest valuation questions in crypto is whether a token's utility creates durable buy-side pressure or only temporary activity from farming. Recent discussion of token valuation also highlights how difficult it is to separate utility from investment behavior. The sharper question is how much observed token demand is organic versus incentive-subsidized, and what onchain metrics distinguish the two, as discussed in CoW Protocol's tokenomics guide.

For stablecoin depositors, that distinction matters because a subsidy can make your dashboard look healthy while the protocol's economic base stays weak.

The difference between yield and emissions

A lot of bad decisions come from treating all APY as if it had the same quality.

Consider the contrast below:

Revenue-linked yield comes from borrowing demand, trading fees, liquidation income, validator payments, or other activity users would perform even without token rewards.

Emission-linked yield comes from distributing a native token whose market price depends on continued demand for that same incentive structure.

The first can still fall, but it's tied to business activity. The second can evaporate quickly if token selling accelerates.

That's why stablecoin users should read tokenomics as protocol risk. If a platform's growth relies on paying depositors and liquidity providers with a highly dilutive token, then the token becomes a shock absorber for the whole model. Once that shock absorber breaks, governance quality often deteriorates too. Treasury decisions get defensive, incentives become more aggressive, and users begin to rotate out.

What sustainable design looks like

Better designs usually share a few traits:

Rewards match a clear purpose. Emissions pay for liquidity, security, or participation the protocol needs.

The token affects behavior after launch. Holders lock, vote, or coordinate in ways that improve the protocol, not just harvest rewards.

Protocol value exists outside the token. Users would still use the product if the token were less exciting.

Disclosure stays current. Supply changes, treasury actions, and governance choices remain visible.

This is one reason many experienced users prefer to evaluate protocols through dashboards, treasury trackers, governance forums, and direct wallet analysis instead of relying on headline APY. Tools that aggregate risk-aware opportunities can help narrow the field. For example, Yield Seeker monitors stablecoin yield opportunities across DeFi and allocates based on user-defined risk and return settings, which is useful if you want a workflow centered on protocols rather than chasing farm campaigns one by one.

The safest-looking stablecoin yield can still be fragile if the protocol needs a falling token price to keep users paid.

A practical mindset for depositors

If you hold stablecoins, your job isn't to become a token maximalist. Your job is to decide whether a protocol's tokenomics strengthens your margin of safety or weakens it.

Ask yourself:

Would this protocol still attract users if token rewards were cut?

Does governance control risk in a disciplined way, or mainly vote on emissions?

Are rewards funded by actual usage, treasury runway, or token issuance?

If insider token vesting completes, does the protocol still have a reason to retain depositors?

Those questions usually matter more than the top-line APY.

Your Framework for Evaluating Any Protocol

A strong tokenomics framework doesn't guarantee you'll avoid every bad protocol. It does make you harder to fool.

The most useful shift is moving from launch analysis to post-launch behavior. A major overlooked question in tokenomics is what happens after the early excitement fades. Many explainers stay focused on supply and vesting, but the deeper issue is retention. What token features keep users engaged after the initial hype cycle, and which ones transfer value from later participants to earlier ones? That under-answered question is highlighted in Duke's discussion of token design and network development.

Here's the framework I'd use before depositing into any DeFi protocol:

Who holds the token today and how concentrated is that ownership?

When does new supply arrive and who receives it?

What does the token do when market interest cools off?

Does the protocol create value without constant token support?

Would I still trust the yield source if rewards were paid in stablecoins instead of the native token?

Can I verify treasury behavior, governance process, and emissions onchain?

That same discipline applies beyond crypto. Investors in other asset classes also learn quickly that returns can look simple while the underlying structure is anything but. If you manage a broader portfolio alongside DeFi positions, practical guides like these tax tips for real estate investors are a good reminder that structure often matters as much as headline return.

For protocol-specific due diligence, I'd pair tokenomics review with a dedicated protocol safety analysis framework. That combination catches far more risk than yield comparisons alone.

Tokenomics won't replace contract audits, governance review, or market judgment. But if you understand who gets paid, why they stay, and what happens when incentives weaken, you'll make better decisions with your stablecoins.

If you want a simpler way to put that framework into practice, Yield Seeker helps stablecoin holders monitor and allocate across DeFi opportunities with a risk-aware, automated workflow. It's built for people who want exposure to onchain yield without manually tracking every protocol, emission schedule, and governance change themselves.