You're probably in one of two camps right now. You hold stablecoins like USDC and you're tired of seeing them sit idle, or you've looked into DeFi yield and backed away because the workflow felt like a part-time job with a decent chance of self-inflicted damage.

That hesitation is rational. Web3 finance can put digital dollars to work around the clock, but it also asks ordinary users to think like traders, security engineers, and operations analysts. The upside is real. The friction is real too.

The useful way to understand Web3 finance isn't as a vague revolution. It's a different financial rail. It lets software move, lend, trade, and settle value without waiting for a bank's operating hours or a broker's approval queue. For stablecoin holders, that matters because yield in this system is often visible, programmable, and accessible in ways traditional cash products are not.

What Is Web3 Finance and Why It Matters for Your Cash

If you hold stablecoins, Web3 finance matters for one simple reason. It gives your cash-like assets access to a global market of automated financial applications that never close.

A bank savings account is a closed system. The bank decides rates, access, and product packaging. In Web3 finance, your wallet can connect directly to lending markets, exchanges, and collateral systems. That doesn't make it safer by default. It does make it more open, more immediate, and more demanding.

Web3 finance represents an upgrade from a local branch network to an always-on financial operating system. Your stablecoins aren't just sitting in an account. They can be routed into lending pools, used to provide trading liquidity, or moved between protocols as conditions change. Software handles the matching and settlement.

McKinsey noted that daily transaction volume on decentralized-finance exchanges exceeded $10 billion at one point, which is a useful marker that this stopped being a toy market and started functioning like real infrastructure (McKinsey on what Web3 is). That doesn't mean every protocol deserves trust. It means the rails themselves can handle serious activity.

Web3 finance is most compelling when you treat it as infrastructure, not entertainment.

For stablecoin holders, the practical question isn't “Is DeFi interesting?” It's “Can these rails help me earn on idle balances without taking risks I don't understand?” That's the right framing. Start there, and a lot of the noise falls away.

If you want a quick grounding in the underlying market category before going deeper, this primer on decentralized finance basics is worth reading.

The Core Building Blocks of Web3 Finance

The easiest way to make sense of Web3 finance is to think in layers. Not every user needs to understand the code, but everyone deploying money should understand the stack.

Blockchain as the base layer

A blockchain is the shared ledger. It records who owns what and which transactions have happened. In practical terms, it's the settlement layer that lets strangers transact without relying on one company to keep the books.

That ledger is why Web3 finance can be more inspectable than traditional finance. If you want a clear explanation of why that matters beyond crypto hype, Wonderment Apps has a useful piece on blockchain accountability and transparency.

Smart contracts as the rules engine

A smart contract is software on the blockchain that executes predefined rules. If collateral falls below a threshold, it can trigger liquidation. If a borrower pays interest, it can route that payment to lenders. If a swap meets pricing conditions, it can settle the trade.

Web3 finance evolves beyond digital money. The contract is the operating logic. It replaces a lot of the manual back-office work that banks, brokers, fund admins, and exchanges usually perform.

Practical rule: If you can't explain what the contract is supposed to do in plain English, don't send it money.

Tokens as the value layer

Tokens represent value inside these systems. Some are native assets of a blockchain. Some are stablecoins meant to track fiat currencies. Others represent claims on collateral, vault deposits, governance rights, or tokenized real-world assets.

This part is no longer theoretical. In November 2022, Securitize launched a tokenized fund on Avalanche in partnership with KKR, showing how on-chain assets can represent real-world value rather than just crypto-native speculation (BCG on Web3 and tokenization).

Applications as financial products

Once you combine blockchains, smart contracts, and tokens, you get the applications most users touch:

AMMs and DEXs: These are automated exchanges. Instead of an order book run by a central venue, liquidity pools and pricing formulas handle swaps.

Lending protocols: These let users deposit assets to earn or borrow against posted collateral.

Liquid staking systems: These issue a tokenized claim on staked assets so users can keep that value productive elsewhere.

DAOs: These are governance systems that let communities or token holders vote on parameters, treasury actions, and upgrades.

The “digital LEGO” analogy fits because teams can combine these pieces in different ways. A yield strategy might deposit stablecoins into a lending market, use the receipt token elsewhere, and rebalance based on changing conditions. The flexibility is powerful. It also means complexity stacks quickly.

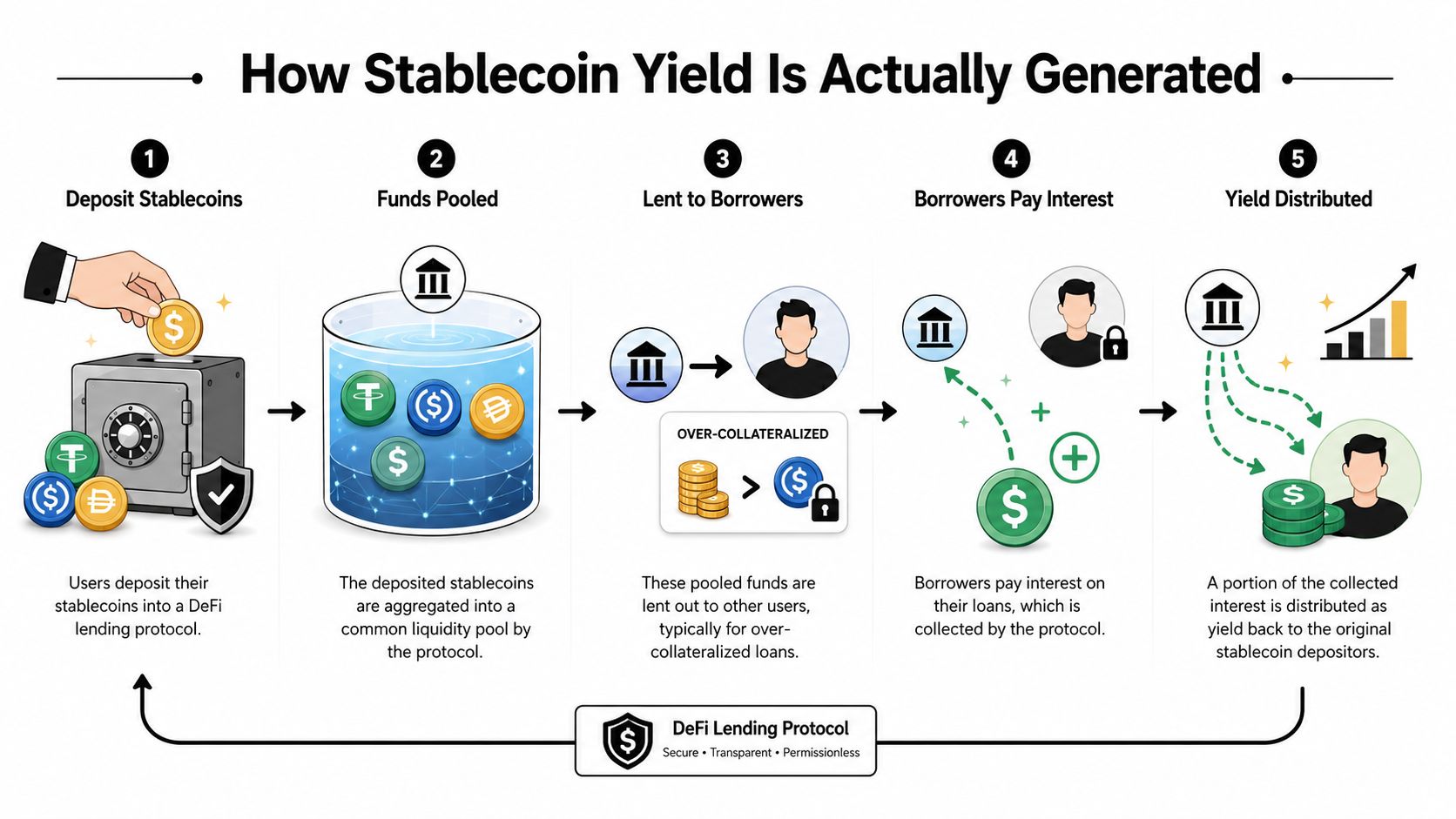

How Stablecoin Yield Is Actually Generated

This is the question that matters most. Where does the yield come from? In serious Web3 finance, the answer should trace back to an identifiable activity, not magic.

Lending fees

The cleanest source of stablecoin yield is borrower demand. You deposit USDC or a similar asset into a lending protocol. The protocol pools deposits and lends them to borrowers who post collateral. Borrowers pay interest. Depositors receive a portion of that interest.

That's the closest on-chain equivalent to a money market mechanism. It's still not the same as a bank deposit, because there's no traditional deposit insurance and the software itself introduces new risk. But the revenue source is understandable.

If you want a more detailed look at this category, this overview of lending protocols in DeFi lays out the mechanics clearly.

Trading fees from liquidity provision

Another yield source comes from providing liquidity to decentralized exchanges. When traders swap one asset for another, the protocol charges fees. Liquidity providers earn a share of those fees.

For stablecoin pairs, this can be more intuitive than volatile token pairs because the assets are designed to stay close in value. Even then, “simple” doesn't mean “risk-free.” Pool design, asset quality, and withdrawal conditions all matter.

Incentives and promotions

Some protocols add token incentives on top of organic revenue. This is the part many users misunderstand.

Incentives can help bootstrap a market, but they're not the same thing as durable yield. If a strategy only looks attractive because emissions are generous, you need to ask what happens when those emissions slow down or buyers stop valuing the reward token.

A good test is simple. If you remove the incentive token, is there still a business model underneath?

Why automation changes the economics

Smart contracts make these flows happen continuously. Interest accrues, fees settle, and capital can move without waiting for a human operations team. That speed matters.

JPMorgan Chase's 2022 transaction using tokenized Singaporean and Japanese yen deposits showed blockchain-based smart contracts processing value transfers in seconds instead of days on traditional rails (CoinDesk on JPMorgan's public-blockchain DeFi trade). For stablecoin yield, that kind of immediacy is useful because capital doesn't have to sit idle between decisions, transfers, and settlements.

In practice, the strongest yield strategies usually combine credible revenue sources with disciplined execution. Chasing the headline number without understanding the engine underneath is how people confuse distribution with income.

Navigating the Major Risks and How to Mitigate Them

The fastest way to lose money in Web3 finance is to focus only on yield. The second fastest is to assume “decentralized” means safe. It doesn't.

One of the sharpest observations about this market is that “Web3 does not have an ideas problem. It has an execution problem,” with front-end tampering and malicious site cloning causing serious user losses (Time on Web3's execution gap). That tracks with what hurts users. Not abstract whitepaper flaws. Basic operational mistakes, weak interfaces, and confusing transaction flows.

The four risks that matter most

Risk Type | Description | Mitigation Strategy |

|---|---|---|

Smart contract risk | The protocol code may contain bugs, flawed assumptions, or upgrade paths that change behavior. | Use established protocols, read documentation, verify audits exist, and avoid products you can't explain. |

Counterparty risk | A product may be “decentralized” in branding but still rely on a small team, concentrated admin control, or opaque treasury decisions. | Check who controls upgrades, pause functions, and treasury keys. Favor systems with transparent governance and narrower trust assumptions. |

Liquidity risk | You may be able to enter a position more easily than you can exit it, especially during stress. | Prefer deep, simple markets for core stablecoin exposure. Test small withdrawals before committing larger balances. |

Regulatory risk | Rules can change around stablecoins, access, reporting, and platform operations. | Keep records, understand the jurisdictions involved, and avoid structures that depend on legal ambiguity. |

What works in practice

Users often overestimate technical risk and underestimate operational risk. They'll read about smart contracts for days, then click a sponsored link, connect the wrong wallet, and sign a bad transaction.

The more useful risk routine is boring:

Use the official interface: Bookmark protocol URLs. Don't trust search ads or random links in group chats.

Start with small transactions: Test deposits, approvals, and withdrawals before increasing exposure.

Separate wallets by purpose: Many experienced users keep one wallet for exploration and another for capital they care about.

Prefer simpler products: A basic lending market is easier to reason about than a stacked strategy built from several protocols.

Watch the exit path: Before depositing, check how withdrawals work, what assets you'll receive back, and whether any redemption friction exists.

What usually doesn't work

A lot of users build risk management around vibes. They trust a protocol because it's popular on social media, because the UI looks polished, or because they've heard a few recognizable names mention it.

That's not a process. It's borrowed confidence.

Security in Web3 finance is usually lost at the interface layer, not in the abstract promise of the protocol.

Another mistake is treating diversification as random spreading. Holding small balances across many weak platforms doesn't reduce risk in a useful way. It often multiplies monitoring burden and creates more ways to make an error. Better diversification is intentional. Different protocols, different mechanisms, and a clear reason for each allocation.

Getting Started in Web3 Finance Safely

The operational burden is what deters many. That's reasonable. Mainstream Web3 finance is moving toward practical use cases, but the key question is whether ordinary users can operate it without becoming their own compliance, security, and treasury desk (Convera on the state of Web3 finance).

The manual path

The traditional DIY route looks like this:

Research protocols yourself: You read docs, compare forums, track sentiment, and check whether yield is organic or incentive-driven.

Manage wallet and chain complexity: You bridge funds, maintain gas on the right network, and keep track of which wallet is connected where.

Monitor positions constantly: You watch rate changes, pool conditions, asset quality, and protocol announcements.

Handle every execution step: Deposits, approvals, rebalances, exits, and recordkeeping all sit with you.

For crypto natives, that process is familiar. For everyone else, it's operational drag. It also creates a lot of room for preventable mistakes.

The automated path

A more practical route is to use software that reduces decision fatigue and execution risk. That can mean dashboards, alerting tools, managed interfaces, or AI-based systems that monitor and allocate based on rules you can inspect.

One example is Yield Seeker, which uses an AI agent to monitor and allocate stablecoin capital across DeFi protocols while keeping funds accessible without lockups. That kind of model won't remove protocol risk, but it can reduce the manual workload of hunting opportunities, tracking fragmented dashboards, and making every move by hand.

A safer starting routine

If you're new but serious, use this order of operations:

Choose one stablecoin and one chain. Complexity compounds fast.

Use a small test amount first. You're testing workflow as much as yield.

Pick one simple strategy. Lending is easier to evaluate than layered farming.

Verify the full exit path. If you can't explain how to get out, don't get in.

Automate only after you understand the baseline. Good automation reduces workload. Blind automation increases hidden risk.

The goal isn't to become an expert in every protocol. It's to create a process you can run reliably.

The Future Is Automated AI-Driven Yield

Manual yield farming won't disappear overnight, but it's already starting to look like manual spreadsheet accounting in a world of modern finance software. It still exists. It's still useful for specialists. It's no longer the optimal operational method for a broad audience.

Why AI fits this market

Web3 finance produces constant information. Rates move. liquidity shifts. New incentives appear. Risk changes at the protocol, interface, and market level. Humans can monitor some of that. Software can monitor more of it, more consistently.

That's why AI-driven orchestration matters. If you want a useful frame for how multiple automated agents can coordinate decisions and workflows, this piece on AI agent orchestration from Tekk.coach is a good reference. The same idea applies to yield systems that analyze opportunities, evaluate constraints, and route capital according to user goals.

The likely end state is simple. Users won't manually chase farms across dashboards. They'll define risk preferences and liquidity needs, then intelligent systems will handle the ongoing work. That's the direction platforms focused on AI yield optimization are pushing toward.

A short visual explainer helps if you want to see that shift in context:

The long-term value of Web3 finance won't come from making everyone a full-time DeFi operator. It will come from making advanced financial infrastructure usable by people who have jobs other than monitoring wallets.

FAQs for Busy Investors and Treasuries

Is stablecoin yield passive income

Not in the purest sense. The yield may accrue without daily manual action, but the risk doesn't disappear just because the interface feels passive. Someone still needs to evaluate the protocol, monitor changes, and understand the exit path.

What's the simplest place to start

Start with one stablecoin, one chain, and one straightforward lending strategy. Avoid layered products until you can explain exactly where the return comes from and what conditions could interrupt it.

Is the highest yield usually the best option

Usually not. Very high posted yields often include short-term incentives, thin liquidity, or risk that isn't obvious from the headline number. Sustainable yield is generally less exciting and more understandable.

For most users, boring is a feature.

Should a treasury use the same approach as an individual

Not exactly. A treasury usually cares more about liquidity management, policy controls, counterparty review, and reporting discipline. Individuals can be more flexible. Treasuries need repeatable process and clear approvals.

What should I check before depositing funds

Use a short checklist:

Protocol clarity: Can you explain the source of yield in one sentence?

Operational safety: Are you on the correct interface and using the intended wallet?

Exit mechanics: Do you know how and when you can withdraw?

Asset quality: Do you understand the stablecoin and any collateral exposure involved?

Monitoring plan: Who is responsible for checking the position after entry?

Is automation worth it

Yes, if it reduces complexity you'd otherwise mishandle. No, if you use it as an excuse not to understand the product at all. Good automation cuts research burden and execution friction. It doesn't remove the need for judgment.

What's the biggest mistake beginners make

They optimize for yield before they optimize for survival. In Web3 finance, a modest return collected consistently is better than a flashy rate attached to a workflow you can't safely operate.

If you want a lower-friction way to put stablecoins to work, Yield Seeker is built for that use case. It helps users deposit USDC, monitor opportunities through an AI agent, and stay exposed to accessible, risk-aware DeFi yield without manually juggling research, dashboards, and constant reallocations.