Ever stared at a screen full of DeFi protocols, all promising juicy yields, and had no idea where to even begin? You’re not alone. Figuring out where to put your stablecoins is more than just chasing the highest APY. It's about learning how to look under the hood to see where that yield really comes from, how sustainable it is, and what risks are hiding in the fine print.

A Look at DeFi Yields in 2026

The world of DeFi has proven to be surprisingly tough. After bottoming out around $50 billion back in late 2022, the total value locked (TVL) has clawed its way back to a healthy $130–$140 billion by early 2026. This isn't just a number—it shows the ecosystem is maturing. You can dig deeper into the market’s comeback with these DeFi market statistics.

With all this new capital flowing in, we're seeing more opportunities than ever. But it also means there's a lot more noise. Those flashy APYs you see are often just temporary bait or attached to incredibly risky strategies. Real yield hunting means you have to get your hands dirty and understand the mechanics.

Where Does Stablecoin Yield Actually Come From?

At its core, DeFi yield is generated from just a handful of activities. Each one has its own unique risk and reward, which is why comparing a lending APY to a liquidity pool APY is like comparing apples to oranges.

Getting a handle on these categories is the first step to making smarter moves.

Lending & Borrowing: This is the bread and butter of DeFi. You supply your stablecoins to a protocol like Aave, and people who want to borrow them pay you interest. The yield here is all about simple supply and demand.

Trading Fees (Liquidity Provision): By adding your stablecoins to a liquidity pool on an AMM like Uniswap, you help other people trade. In return, you get a small cut of the trading fees. The big catch here is the risk of impermanent loss.

Staking & Protocol Rewards: Some protocols will pay you in their own native token just for staking or helping with governance. This type of yield can be all over the place, since its value is tied directly to that token's price on the open market.

A Quick Guide to DeFi Yield Categories

To help you sort through the options, I've put together a simple table. Think of it as a quick reference guide to what you can generally expect from each type of yield source for stablecoins.

Yield Category | Typical Stablecoin APY Range | Primary Risk Factor |

|---|---|---|

Lending Protocols | 3% - 8% | Smart Contract Failure |

Liquidity Provision | 5% - 15%+ | Impermanent Loss |

Yield Aggregators | 6% - 20% | Strategy & Platform Risk |

Liquid Staking | 7% - 18% | LST De-Pegging & Slashing |

This table should give you a good starting point for what's out there.

The most important shift in mindset is this: Your goal isn't just to find the highest number. It’s to find the best risk-adjusted return that fits what you're trying to achieve. A 7% yield from a protocol that's been around for years is a world away from a 15% yield on a brand-new, unaudited platform.

This guide will walk you through how to properly size up these opportunities, moving past the headline numbers to a smarter way of making decisions. If you're just looking for a simple place to start, checking out these stablecoin interest alternatives is a great way to see the range of what's possible.

Understanding Where DeFi Yield Actually Comes From

When you're hunting for yield in DeFi, the first question shouldn't be "How much?" but "Where's the money actually coming from?" A 10% APY from one protocol is not the same as a 10% APY from another. Getting to grips with the mechanics behind the return is the first, and most critical, step in judging its quality and sustainability.

Every yield has an origin story—a specific economic engine that generates the return you pocket. If you can't pinpoint that engine, you might be looking at an unsustainable yield propped up by inflationary token rewards or sketchy, hidden strategies. To truly compare DeFi yields, you have to compare what’s under the hood.

Lending Protocols: The Interest Rate Engine

The most straightforward source of yield in DeFi comes from lending protocols like Aave and Compound. The mechanics here are old as the hills, basically a crypto-native version of traditional banking.

You supply assets: You deposit your stablecoins (like USDC) into a big pool of money.

Others borrow from it: Other users take out loans from that pool, usually to trade or get leverage on other crypto positions.

You earn interest: The borrowers pay interest on their loans, and you, as a supplier, get a cut of that interest.

The yield is driven by pure supply and demand. When lots of people want to borrow but there are few lenders, interest rates—and your yield—shoot up. On the flip side, if the pool is flush with cash but nobody’s borrowing, your yield will be pretty pathetic. The key metric to watch here is the utilization rate—the percentage of supplied assets currently being borrowed.

A higher utilization rate means juicier yields for you, but it's also a red flag for liquidity risk. If almost all the assets are borrowed, you could face delays if you try to pull your funds out.

Automated Market Makers: The Trading Fee Engine

Yield from an Automated Market Maker (AMM) like Uniswap or Curve is a completely different ballgame. Here, the yield comes from facilitating trades. When you become a liquidity provider (LP), you're essentially acting like your own mini-exchange.

You deposit a pair of assets—say, USDC and ETH, or a couple of stablecoins like USDC and DAI—into a liquidity pool. This pool is what lets other people swap between those two assets. For providing this service, you earn a slice of the trading fees from every single swap that happens in that pool.

Your yield is directly tied to trading volume. More trades mean more fees, which means a higher APY for you. Simple enough. But this source of yield comes with its own unique headache called impermanent loss, which is basically the opportunity cost you might face if the prices of the two tokens you deposited drift too far apart.

Liquid Staking: The Dual-Reward Engine

Liquid staking protocols, with Lido being the big kahuna, introduce a more complex but seriously powerful way to earn. The yield here is multi-layered.

Base Staking Rewards: First, you stake a proof-of-stake asset like ETH. In return, you get the base network rewards, which come from securing the network and validating transactions. These are typically in the 3-5% APY range.

DeFi Composability: When you stake, you get a Liquid Staking Token (LST), like stETH, in return. This token represents your staked ETH but, crucially, it remains liquid and usable. You can then take this LST and put it to work again in other DeFi protocols—lend it, use it as collateral, or provide liquidity—to earn a second layer of yield.

This "yield stacking" is what makes LSTs so compelling. Your total APY is a mashup of the base staking reward and whatever extra yield you can squeeze out by deploying the LST elsewhere. It’s a fantastic way to be capital-efficient, but it also means you’re stacking risks from multiple protocols. Comparing these yields means you need to size up both the base staking layer and the secondary DeFi protocol you decide to jump into.

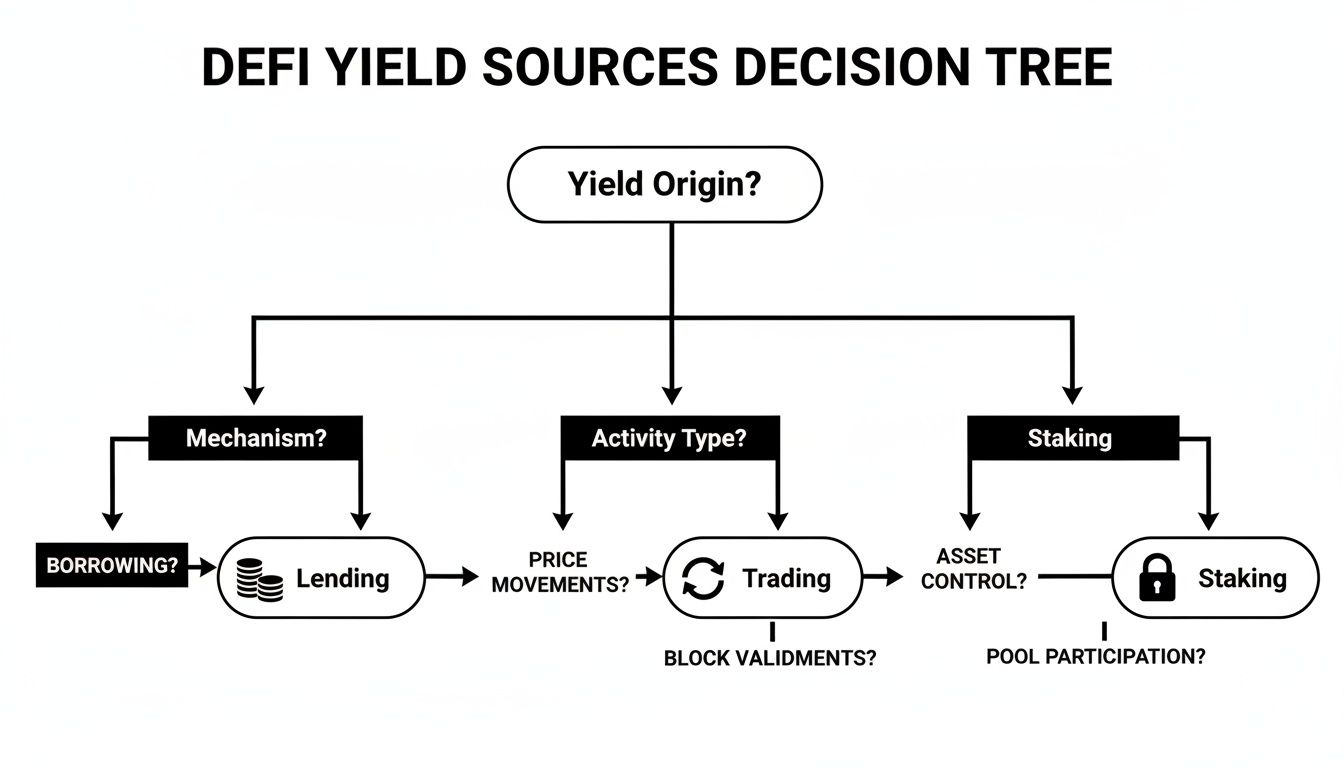

A Practical Framework for Evaluating Stablecoin Yields

Jumping into the world of stablecoin yields without a plan is a quick way to get burned. That juicy headline Annual Percentage Yield (APY) you see plastered on a protocol’s homepage is just the starting point. To make smart calls when comparing DeFi yields, you need a framework that helps you peel back the layers and see what’s really going on.

This means looking past the flashy numbers and asking some tough questions. Where does the yield actually come from? What fees are going to chip away at my returns? What are the real risks involved? A high APY is nice, but a sustainable, risk-adjusted return is how you actually win in the long run.

This decision tree gives you a great mental model for how your capital generates yield, starting right from the source.

As you can see, your yield journey starts by figuring out if the return is from lending, trading, or staking. Each path has its own set of opportunities and, more importantly, its own set of risks. This first choice really dictates what you need to look out for.

Looking Past the Headline APY

The first thing I always do is translate that advertised APY into a more realistic number. There are always a few things that will eat into your returns, and you have to account for them.

Your goal is to figure out the Net APY—the return you’ll actually see after all costs are paid. These are the usual suspects:

Protocol Fees: The cut the DeFi protocol takes for providing the service.

Performance Fees: A percentage of your profits, usually taken by yield aggregators or vaults.

Gas Fees: The cost of transactions on the blockchain to deposit, withdraw, or compound your earnings.

For example, a 12% headline APY can quickly drop to 9-10% after you factor in a 15% performance fee and the gas you’ll spend manually compounding. Making this adjustment right away gives you a much better baseline for comparing different DeFi yields.

Differentiating Yield Strategies and Their Risks

Understanding where your yield comes from is absolutely critical for judging its risk. As we’ve talked about, a return from lending is a completely different beast than one from trading fees. Each strategy has a unique risk-reward tradeoff.

To get a clearer picture, let's break down the main strategies for stablecoin yields and how they stack up.

Stablecoin Yield Strategy Comparison Matrix

This table gives a high-level breakdown of the most common yield strategies. Think of it as a cheat sheet to quickly match an opportunity with your personal risk tolerance and goals.

Strategy Type | Source of Yield | Typical APY (Stablecoins) | Key Risks | Best For |

|---|---|---|---|---|

Lending | Interest paid by borrowers | 3% - 7% | Smart contract failure, protocol insolvency, low utilization | Conservative investors focused on capital preservation and steady, low-effort income. |

Liquidity Provision | Trading fees from swaps | 5% - 15%+ | Impermanent loss, smart contract bugs, stablecoin de-pegging | Active investors with a higher risk tolerance who are comfortable managing positions to offset impermanent loss. |

Yield Aggregators | Automated strategy execution | 6% - 20% | Strategy risk (vault logic), smart contract risk, platform dependency | Users who want higher, compounded returns without the manual work, and who trust the aggregator's security. |

It's pretty clear from this matrix: as the potential APY goes up, so do the complexity and the risks. A simple lending strategy on a blue-chip protocol like Aave is fairly straightforward; your main worry is a major protocol hack. Contrast that with providing liquidity, where you have the very real risk of impermanent loss (IL)—where you could end up with less money than if you had just held the assets in your wallet.

A great way to get comfortable with these concepts is by exploring the different stablecoin interest rates and the platforms that offer them.

Adjusting for Risk and Volatility

The last piece of the puzzle is adjusting for risk. This idea of a Risk-Adjusted Yield helps you compare completely different strategies on a more level playing field. While there isn't one magic formula, you can get a good qualitative sense by looking at a few key things:

Protocol Audits and History: Has the protocol been audited by solid firms? How long has it been running without a major incident? A battle-tested protocol like Compound with multiple audits is way less risky than some new, unaudited platform that just launched.

Stablecoin Peg Stability: Is the yield coming from a rock-solid stablecoin like USDC, or a newer, more experimental algorithmic one? De-peg risk is a massive factor you can't ignore.

Impermanent Loss Potential: If you're looking at providing liquidity, use an IL calculator to see what could happen under different price moves. A 15% APY can easily become a negative return if one of the stablecoins in the pair starts to wobble.

By applying this framework—calculating Net APY, identifying the strategy, and assessing the risks—you can stop chasing big, meaningless numbers. This disciplined approach helps you make strategic decisions that actually fit your goals and risk tolerance, turning the chaos of comparing DeFi yields into a structured process.

Comparing Yields from DeFi Lending Protocols

Lending protocols are the bedrock of DeFi. They’re some of the most straightforward, battle-tested places to earn yield. When you supply stablecoins to a platform like Aave or Compound, you’re essentially participating in an on-chain money market. The yield you get is just the interest paid by borrowers—simple as that.

But don't let the simplicity fool you. Not all lending yields are created equal. The rates you see are always in flux, driven by raw supply and demand. To really know what you’re getting into, you have to look under the hood at how these rates work and how healthy the protocol is before you can properly compare DeFi yields.

The Engine Behind Lending APYs

The interest rates on these platforms are set by algorithms designed to keep both lenders and borrowers happy. The main driver for your APY is the utilization rate—that’s just the percentage of all supplied assets that are currently being borrowed.

Low Utilization: When the pool is full of cash but nobody’s borrowing, the protocol lowers the APY to entice borrowers.

High Utilization: When most of the assets are borrowed out, the algorithm jacks up the interest rate. This encourages new suppliers (like you) to come in and nudges borrowers to repay their loans.

This dynamic is a double-edged sword. A high utilization rate means a higher APY for you, which is great. But it also signals a big liquidity risk. If a pool’s utilization gets close to 90-100%, it means there’s almost no capital left. You might find yourself stuck, unable to withdraw your funds when you want to.

So, when you're comparing lending protocols, the first thing to check is both the supply APY and the utilization rate for the asset you’re lending. A slightly lower, more stable APY on a protocol with a healthy utilization rate (say, 40-70%) is often a much safer play than chasing a monster APY on a platform where liquidity is dangerously low.

Key Metrics for a True Comparison

Beyond the utilization rate, there are a few other things you need to check to get a real sense of a protocol's stability and whether its yields are sustainable. You can't just look at the single pool you’re interested in; you have to zoom out and assess the health of the entire protocol.

1. Collateral Diversity and Quality Borrowers have to post collateral to get a loan, and the quality of that collateral is everything. Protocols that stick to blue-chip assets like ETH, BTC, and top-tier LSTs are generally safer. You should be a bit wary of platforms that let people borrow against a whole bunch of illiquid, volatile altcoins. That’s a recipe for bad debt when the market takes a dive.

2. Loan-to-Value (LTV) Ratios The LTV ratio dictates how much someone can borrow against their collateral. More conservative LTVs (like 50-75%) create a bigger safety cushion before a borrower gets liquidated. Aggressive LTVs just add more risk to the entire system.

3. Protocol TVL and Health A high Total Value Locked (TVL) is a good sign. It shows market trust and deep liquidity. The DeFi lending space has matured quite a bit. In early 2026, the sector's TVL was holding strong at $58 billion, with Aave v3 on Ethereum absolutely dominating with 79% market share. With a healthy sector-wide utilization of 35-36%, there's plenty of room for borrowing to grow without putting a ton of pressure on rates. You can read more about the state of institutional crypto flows to get a feel for these market dynamics.

Real-World Comparison Scenario

Let's say you're looking at two protocols for your USDC:

Protocol A (Established): Offers a 4.5% APY with a 65% utilization rate. It has billions in TVL and mostly accepts ETH and BTC as collateral.

Protocol B (Newer): Dangles a 7.2% APY with a scary 92% utilization rate. Its TVL is tiny, and it accepts a grab-bag of less-liquid altcoins.

That 7.2% from Protocol B might look tempting, but it’s loaded with risk. The high utilization rate means you could have trouble getting your money out, and its weak collateral makes it fragile. For anyone focused on preserving capital and earning a steady income, Protocol A is the obvious choice.

This is what disciplined DeFi investing looks like—prioritizing safety and stability over just chasing the highest number. It's the hallmark of a savvy investor.

While lending protocols are a great way to earn some steady returns, liquid staking has completely changed the game for more advanced yield strategies. It fundamentally reworks how you can use staked assets, transforming them from locked-up, passive capital into active tools for building multi-layered returns. This unlocks a level of capital efficiency that’s just tough to beat with simpler DeFi plays.

The secret sauce here is the Liquid Staking Token (LST). When you stake a proof-of-stake asset like ETH through a protocol like Lido or Rocket Pool, you get an LST (like stETH or rETH) back. This token is your claim on the original staked ETH and all the rewards it's racking up, but the crucial difference is it's not locked—it’s fully liquid and ready to be used all over DeFi.

The Power of Yield Stacking

This liquidity is where the real magic happens. LSTs let you have your cake and eat it too through a strategy called yield stacking. You're earning the base staking reward for helping secure the blockchain, and then you can take your LST and put it to work somewhere else to earn a second, or even a third, layer of yield.

Here’s a quick look at how a basic yield stacking strategy plays out:

Stake ETH: You stake your ETH with a liquid staking provider and get an LST in return. This token automatically earns staking rewards, which are typically in the 3-5% APY range.

Deposit LST into a Lending Protocol: You then take that LST and deposit it as collateral into a lending protocol like Aave. Now you're earning an additional lending yield on top of your staking rewards.

Borrow and Repeat (Optional): If you're feeling more aggressive, you can borrow an asset (like a stablecoin) against your LST collateral and use that to chase another yield, compounding your returns even further.

This composability is what makes LSTs such a breakthrough. It turns a single-yield asset into a "money lego" that can be plugged into different DeFi protocols at the same time. The result is a compounded APY that often leaves isolated strategies in the dust.

Comparing Rewards and Unique Risks

Liquid staking has totally reshaped how experts think about comparing DeFi yields. The market has exploded, creating opportunities for dual rewards from staking and DeFi that just weren't possible before. LSTs are a massive driver of this, allowing for layered strategies that can take a base staking yield of 4-6% and stack on returns from lending protocols, pushing your effective APY into the 8-12% range when market conditions are right. All this, while your capital stays liquid—a huge advantage over the lockup periods of native staking. To get a sense of its scale, you can explore more about the growth and impact of the liquid staking market.

Of course, this extra potential doesn't come for free. It brings its own set of unique risks that you have to weigh carefully.

LST De-Pegging Risk: The LST is designed to trade close to the value of the underlying asset (e.g., stETH to ETH), but it’s not a hard guarantee. Major market stress or a sudden loss of confidence can cause the LST to "de-peg" and trade at a discount, which can lead to losses.

Slashing Penalties: If the validator running the node for your staked assets misbehaves or goes offline, the underlying network can "slash" or destroy a portion of their stake as a penalty. As an LST holder, that loss gets passed on to you.

Smart Contract Risk: Your money is exposed to the smart contract risk of the liquid staking protocol itself, plus the risk of any other DeFi protocol you decide to use your LST in. It's a double-layered risk.

For experienced users who are comfortable navigating these added layers of risk, LSTs are an incredible tool for squeezing every last drop of efficiency out of your capital and hitting higher returns.

Automating Your Yield Strategy with AI

Let's be honest: manually chasing the best DeFi yields, shuffling funds between protocols, and keeping a constant eye on risk is a recipe for burnout. The market runs 24/7, and the juiciest opportunities can pop up and disappear in the blink of an eye. For most of us, it’s just not practical to stay on top of it all.

This is where a new breed of tool comes in: AI-powered yield allocators. Think of them as your personal DeFi portfolio manager, automating the entire grind of finding and managing stablecoin yields. Instead of you hunting for alpha, a smart agent does the heavy lifting for you.

From Manual Hunting to Automated Allocation

AI-driven platforms completely flip the script. They move you away from the high-effort, screen-staring world of "yield farming" and into a much more passive, automated approach. These systems are constantly scanning a curated list of DeFi protocols, crunching real-time data on APYs, fees, liquidity, and all the underlying risk factors.

This automated approach has some pretty clear wins:

You get your time back: No more endlessly refreshing dashboards or scrolling through Twitter to find the next hot rate.

Decisions are data-driven: An AI can process way more data points than any human ever could, leading to more objective and timely moves.

Built-in risk management: The best platforms bake in real-time risk checks, automatically steering clear of protocols that start showing red flags.

It all boils down to this: you're swapping emotional, reactive decisions for a systematic, data-informed strategy. It lets you tap into DeFi's potential without the operational headache and constant stress of doing it all yourself.

How AI Yield Allocators Work

The whole point is simplicity. With a platform like Yield Seeker, you’re usually just a few steps away from being set up. You deposit your stablecoins, and the AI takes the wheel from there.

If you're curious about the nuts and bolts, the technical documentation for these systems can be quite revealing. For example, checking out BuddyPro's documentation for automated strategies gives you a deeper look into how these agents actually execute trades and handle risk on the back end.

Once you’re set up, the platform's AI agent gets to work:

Monitoring: It keeps a constant watch over a universe of pre-vetted protocols.

Allocation: Based on its analysis, it places your capital in the best mix of opportunities to maximize your risk-adjusted yield.

Rebalancing: As market conditions shift, the AI automatically shuffles your funds, moving out of lower-performing or riskier spots and into better ones.

All of this happens behind the scenes, with your earnings neatly tracked on a simple dashboard. We actually wrote a guide on automated APY discovery that breaks down how this works in practice. This hands-off model opens up passive income on stablecoins to everyone, whether you're new to DeFi or an expert looking to put your more complex strategies on autopilot.

A Few Common Questions About DeFi Yields

As you start exploring the world of DeFi yields, a few questions always seem to pop up. Let's tackle some of the most common ones to give you a clearer picture and help you invest with more confidence.

What’s a Good APY for Stablecoins, Really?

Everyone wants to know what a "good" APY for stablecoins looks like in 2026. The honest answer is, it all comes down to your personal appetite for risk. There’s no magic number that works for everyone, because higher returns almost always mean you're taking on more risk.

A practical way I like to think about it is by breaking it down into tiers:

Conservative (3-7% APY): You'll typically find this range on the big, "blue-chip" lending protocols like Aave or Compound. The risk here is relatively low, making it a solid choice if your main goal is capital preservation.

Moderate (5-12% APY): These returns often come from providing liquidity to stablecoin pools where the assets are tightly correlated (think USDC-DAI pairs) on platforms like Curve.

Aggressive (20%+ APY): Chasing yields this high usually means venturing into newer protocols, dealing with more volatile assets, or using leverage. This territory comes with significant risks, from impermanent loss to smart contract failures.

The goal isn’t just about chasing the highest number you see. It’s about finding the best risk-adjusted return that actually fits what you’re trying to achieve.

How Do I Actually Account for Risk When I Compare Yields?

It's absolutely critical to look past the advertised APY. A real comparison digs into the qualitative risks that come with the territory. Start by checking out the protocol itself. Look at its security audit history, see how long it's been running without any major hacks, and check its Total Value Locked (TVL), which is a decent proxy for how much the market trusts it.

If you're looking at lending, a sky-high utilization rate can be a serious red flag for liquidity risk. For liquidity providing, you should always run the numbers through an impermanent loss calculator to see what the potential downsides could be. And don't forget the stablecoin itself—a de-peg event can easily wipe out all the yield you've worked so hard to earn.

Can I Actually Lose Money with DeFi Yield Farming?

Yes, you can absolutely lose your initial capital. It's not just about missing out on potential gains; yield farming in DeFi has real risks that can lead to losses.

The main culprits are usually:

Smart Contract Risk: A bug or an exploit in a protocol’s code is a prime target for hackers. If they succeed, it could mean a total loss of all the funds you have deposited.

Impermanent Loss (IL): When you're providing liquidity, the value of your position can drop below what it would have been if you'd just held the original tokens. This happens when the prices of the tokens in the pool move in different directions.

Stablecoin De-pegging: If the stablecoin you're farming with loses its 1:1 peg to the US dollar, the value of your capital drops right along with it.

Manually tracking rates, assessing all these risks, and constantly moving your funds is more than a full-time job. With Yield Seeker, you can just deposit your stablecoins and let a personalized AI Agent handle the entire process for you. It automates finding and managing competitive, risk-aware yields so you don’t have to. Start earning smarter at https://yieldseeker.xyz.